Bullish On Precious Metal Focused Juniors

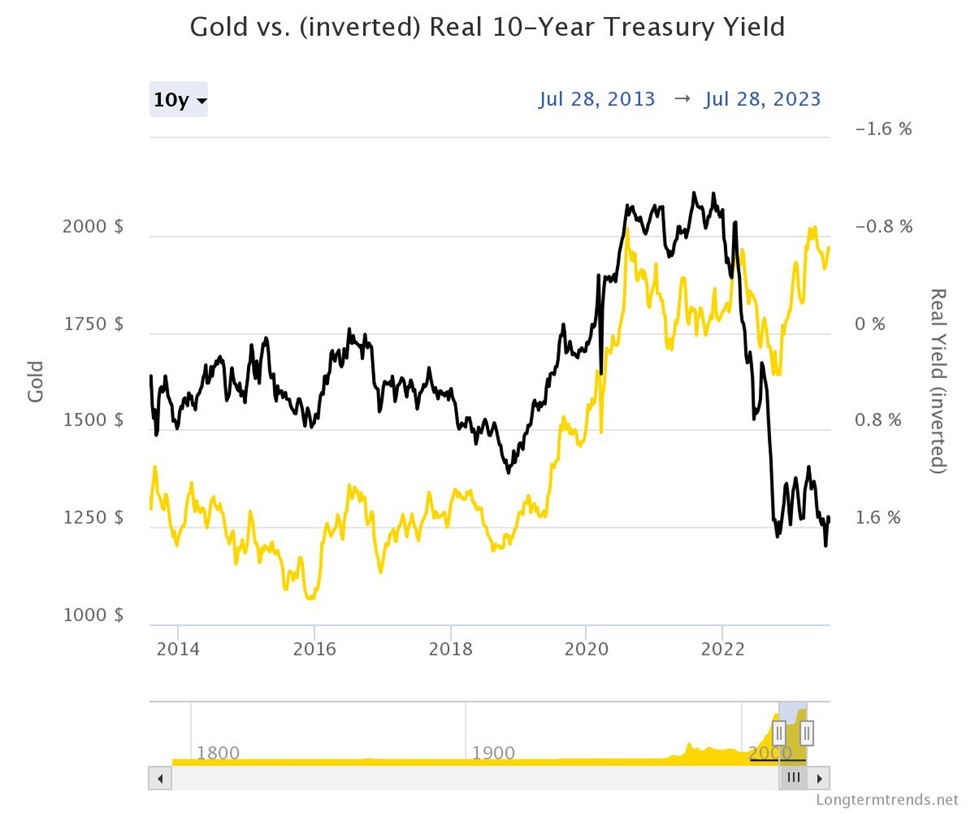

The gold market has gotten a nice little jolt since the US Federal Reserve’s recent decision to lift interest rates once again, now at their highest in 22 years.

While such a move didn’t come as a shock to most people, it did bring us closer to peak interest rates — and eventually, a Fed pivot — which is positive news for gold. This is because when the US central bank reverses its policy, it tends to weaken both the dollar and yields, both of which are rival assets to gold.

“Yields are starting to look toward the Fed to pivot, and it looks like gold’s just ready to break out. I think these boomer rocks, they’re set up for a boom,” said Mike McGlone, Bloomberg Intelligence senior macro strategist, in a Yahoo Finance report.

“The key thing that has pressured gold the past 10 years or so has been the US stock market outperforming the world,” McGlone explained. “The key trigger will be when the US stock market continues to underperform the rest of the world, and gold will be the shining star.

“A sooner Fed pivot on rate hikes will likely cause another gold price surge due to a potential further decline in the US dollar and bond yields,” an analyst from CMC Markets told CNBC earlier this year. Should that happen, it expects bullion to trade between $2,500 to $2,600 an ounce.

Fed Pivot Approaching?

Although it’s anyone’s guess when that will happen, there are a couple of indications that the current monetary policy tightening cycle — the most aggressive since the 1980s — should be drawing to a close.

First and foremost, the US inflation data is looking better. The PCE Price Index, the Fed’s preferred inflation gauge, rose 3% from a year earlier in June, the smallest increase in more than two years. Core prices — which exclude food and energy and are regarded as a more reliable signal of underlying inflation — advanced 4.1%, also the lowest since 2021 and slower than estimated.

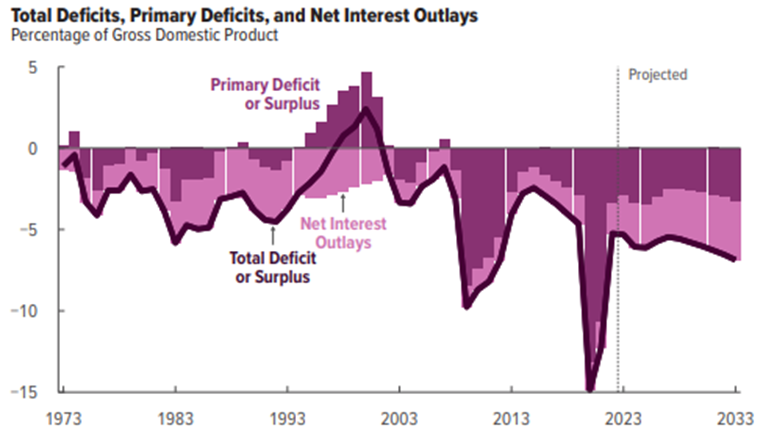

Then there’s the swelling federal debt accumulated during the current monetary cycle. For the first nine months of the fiscal year, the US government deficit totalled $1.4 trillion — a 170% increase from the same period a year earlier. At the current rate of spending, it could easily reach $3 trillion.

“We are projected to spend more on interest payments in the next decade than we will on the entire defense budget,” Maya Macguineas, president of the Committee for a Responsible Federal Budget, told NPR. “How can anyone possibly think this trend is sustainable?”

At some point, the Fed’s rate hike campaign would be deemed too costly for the benefit it provides, and at least some Fed officials are acknowledging that the current cycle is nearing its end.

“We’re likely to need a couple more rate hikes over the course of this year to really bring inflation” sustainably back to the US central bank’s 2% goal, San Francisco Fed President Mary Daly said during an event at the Brookings Institution in July.

However, Daly added that while the risks of doing too little are still greater than those of overdoing it on rate hikes, the two sides are getting into better balance as the Fed nears “the last part” of its hiking cycle.

According to the CME’s FedWatch Tool, the probability that the Fed will leave rates unchanged this year is at 60%.

“I don’t think the Fed’s going to make a move in September, but later in the year, if we continue to get strong economic data, the Fed probably will make one more rate-hike,” Jim Wyckoff, senior market analyst at Kitco, said via Reuters this week.

“Right now, the gold and silver markets are waiting for the next catalyst… if demand from China starts to recover, we see more upside in gold and silver,” he added.

Gold Demand Still Robust

One aspect of the gold market investors shouldn’t worry about is demand.

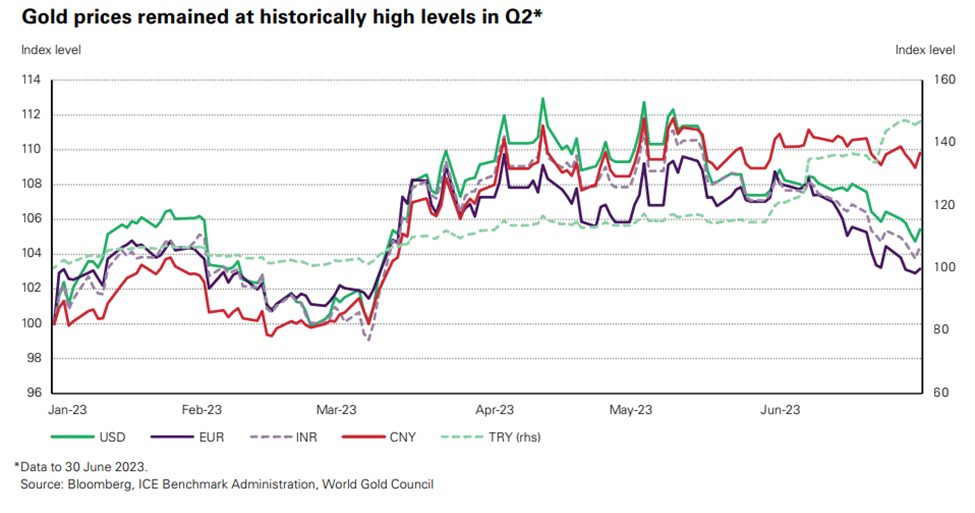

This week, the World Gold Council (WGC) put out a fresh quarterly report confirming the metal’s demand trajectory. In Q2 2023, gold investment in Q2 was healthy compared with the same quarter of last year, up 20% to 256t. Jewelry consumption also strengthened modestly y/y, up 3% to 476t despite historically high (if not record) prices in most markets.

But the most talked-about source of demand has to be central banks, which bought a record 1,136 tonnes of gold last year and followed that up with another 228t in Q1, the most ever in a first quarter.

While central bank net buying slowed to 103t in Q2 2023, down 35% y/y from an extremely high base, the selling activity has done little to dent the underlying positive trend in central bank gold demand, which saw its highest first half on record dating back to 2000, the WGC said.

“Record central bank demand has dominated the gold market over the last year and, despite a slower pace in Q2, this trend underscores gold’s importance as a safe haven asset amid ongoing geopolitical tensions and challenging economic conditions around the world,” Louise Street, senior markets analyst at the WGC, commented.

Looking ahead, the Council expects the positive central bank trend to continue, and an economic contraction could bring additional upside for gold, further reinforcing its safe-haven asset status.

“In this scenario, gold would be supported by demand from investors and central banks, helping to offset any weakness in jewelry and technology demand triggered by a squeeze on consumer spending,” Street said.

Leveraging Gold’s Bull Market

This WGC report, plus gold’s performance during the first half (up 8.2% year to date as we speak), should assuage any concerns that the bull market is fading away. In fact, signs are mostly pointing to the contrary.

Randy Smallwood of Wheaton Precious Metals, chairman of the WGC, told CNBC reporters that “continued central bank buying of gold bodes well for long-term prices.” He forecasts that prices could eventually hit $2,500 an ounce.

An even wilder prediction recently surfaced from Wall Street research firm Goehring & Rozencwajg (G&R), which believes it’s only a matter of time before gold surpasses double digits on its way to $12,000-15,000 an ounce. In a recent interview, managing partner Adam Rozencwajg said he believes “gold has entered into a new phase of this bull market,” and it’s now the perfect time to step back in.

Instinctively, as we head into the second half of the year, investing in gold seems to be the logical choice; yet, buying physical gold like bullion, coins or jewelry may not be logistically feasible for all.

There is, however, an alternative or perhaps more profitable route to realizing the growth potential of physical gold: investing in gold-related stocks. Like with every sector, gold companies can come in different sizes, depending on how much they produce (if at all).

The biggest producers (a.k.a seniors) are likely the most reflective of the market and represent the safest bet, but in terms of reward, it’s the exploration-stage companies (“juniors”) that are more attractive.

In fact, junior gold stocks offer incredible upside potential during gold bull markets. Anecdotally, during a bull market, senior gold miners typically outperform the metal by a multiple of 2 to 3 times. Junior gold stocks – though riskier – can outperform the precious metal’s return by 5 or even 10 times during a bull market.

*********

More from Gold-Eagle