The Commodity Supercycle Revisited

A “commodity supercycle” is a period of consistent price increases lasting more than five years, and in some cases, decades. The Bank of Canada defines it as an “extended period during which commodity prices are well above or below their long-run trend.”

Supercycles occur because of the long lag between commodity price signals and changes in supply. While each commodity is different, the following is a rundown of a typical boom-bust cycle:

As economies grow, so does the demand for commodities, and eventually the demand outstrips supply. That leads to rising commodity prices, but the commodity producers don’t initially respond to the higher prices because they’re unsure whether they will last. As a result, the gap between demand and supply continues to widen, keeping upward pressure on prices.

Eventually, prices get so attractive that producers respond by making additional investments to boost supply, narrowing the supply and demand gap. High prices continue to encourage investment until finally, supply overtakes demand, pushing prices down. But even as prices fall, supply continues to rise as investments made during the boom years bear fruit. Shortages turn to gluts and commodities enter the bearish part of the cycle.

There have been multiple commodity supercycles throughout the course of history. The most recent one started in 1996 and peaked in 2011, driven by raw material demand from rapid industrialization taking place in markets like Brazil, India, Russia and especially, China.

We can talk about the cyclical nature of commodities in general, but we can also pick certain commodities to see whether they are on the upswing or downswing.

Sprott earlier this year pointed out that A new copper supercycle is emerging, built on several rising geopolitical and market trends, including electrification, national security concerns, environmental policy, supply constraints and deglobalization.

Dawn of a new supercycle

While no two supercycles look the same, they all have three indicators in common: a surge in supply, demand and price. The new commodity supercycle, however, could look a bit different from the previous ones for one reason — the focus on attempts to limit global warming.

According to S&P Global, a more aggressive commitment to the energy transition across G-20 nations could also create the conditions for a sustained surge in demand, supply and prices.

Like in the past, commodity supercycles are usually driven by strong demand for raw materials, manufactured materials and sources of energy. The energy transition serves as a major catalyst for all the key inputs to our renewable energy infrastructure, taking demand to levels never seen before.

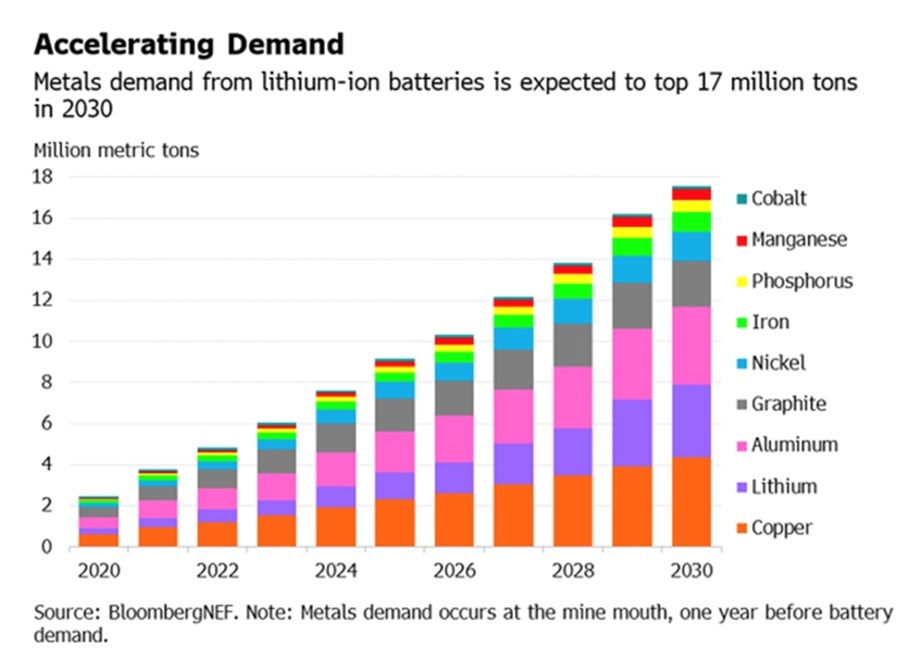

Demand for copper — the cornerstone for all electricity-related technologies — is set to grow by 53% to 39 million metric tons by 2040, according to BloombergNEF. Battery metals like lithium, cobalt and nickel will see even faster growth, reaching more than three times the current demand levels by 2030, says BNEF, with lithium rising the fastest with a seven-fold increase.

Source: BloombergNEF

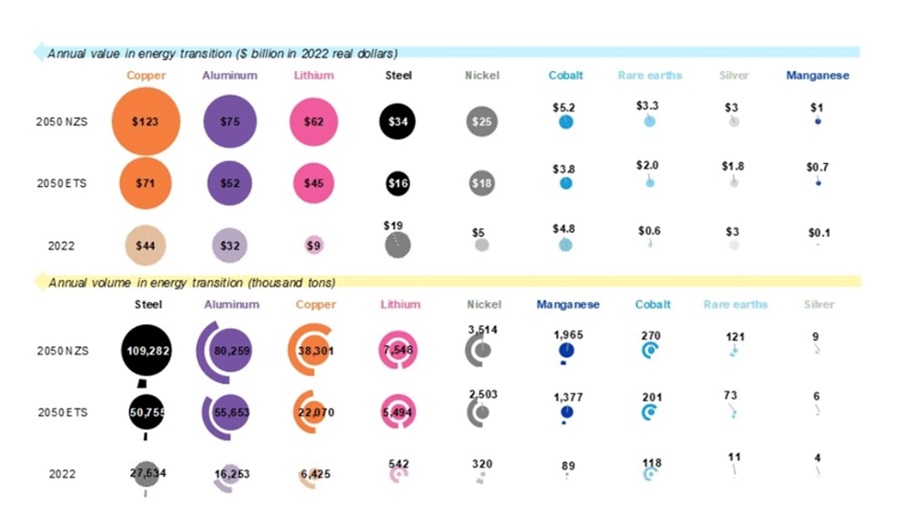

To reach net-zero, demand for these key metals needed for the deployment of energy transition technologies such as solar, wind, batteries and electric vehicles will grow fivefold by 2050, BNEF adds.

Source: BloombergNEF

Another proponent of the “green” commodities supercycle is Dr. Linda Yueh, adjunct professor of economics at the London Business School.

In a 2023 podcast, Yueh said the next commodities cycle has begun in earnest and that this time it’s being led by battery metals. She pointed out that last year, the Guangzhou Futures Exchange became the fourth commodities exchange to launch contracts tracking the price of lithium carbonate, used in electric car batteries.

Last July the COMEX division of the New York Mercantile Exchange launched a lithium carbonate futures contract, while the London Metals Exchange introduced new futures contracts to provide further hedging and trading opportunities for battery materials.

“The sun does not always shine and the wind does not always blow so batteries are crucial for the green transition,” Yueh observes. “Thus, the mining and processing of metals, such lithium and nickel, are driving a potential supercycle and raises attendant resilience concerns about supply chains as well as environmental concerns.”

While China, which controls about 80% of the world’s battery production capacity, is currently the top “commodity superpower,” the term also applies to leading lithium producers Australia and Chile.

For nickel, a mainstay of nickel-manganese-cobalt batteries, the top three producers are Indonesia, the Philippines and Russia.

According to a news article titled ‘Green Tech is Driving the Next Commodities Supercycle’, Yueh believes that the focus of this present supercycle increasingly falls on supply chain resilience, noting that China has had a head start and that it will continue to be a major player for years to come.

(Western countries are aiming to limit China’s clean-technology dominance through tariffs and legislation like the US Inflation Reduction Act — Rick)

A key area of focus will need to be in the processing of battery metals, thereby helping to diversify and add resilience to supply chains while contributing to the important value-added benefits to those countries that make such investments in processing and finishing plants.

In March of this year, The Economic Times of India cited three reasons for the beginning of a new supercycle, not all of them green:

- The global population is thought to have increased beyond 8 billion people— a striking milestone for commodity analysts.

- Per-capita consumption of commodities remains low in emerging market economies, particularly India, which is only at a relatively early stage of the emergence of a sizable middle class, like China.

- A higher commitment to the energy transition across G-20 nations could create the conditions for a sustained surge in demand, supply, and prices. Battery metals such as lithium carbonate are showing the sort of sustained price increases that suggest a bigger cycle is on its way, and hydrogen and carbon markets are in early days of showing strong growth in both supply and demand.

Jeff Curry spent 27 years at Goldman Sachs, where he was head of global commodities research. The man knows a thing or two about commodity supercycles.

He now works for Carlyle, a private equity firm, where he is chief strategy officer for energy pathways.

In speaking recently with Barron’s, Curry said he’s more convinced than ever that commodities have entered a new supercycle that in particular will lift copper, gold and oil prices.

Curry says when (not if) the Federal Reserve cuts interest rates in September, as expected, the most interest-rate sensitive sectors will benefit including green energy and copper.

But unlike previous supercycles, investors need to focus on a larger ecosystem, not just the materials themselves but things like batteries and so-called green steel. Biden’s Inflation Reduction Act for example provides provides $500 million to repower a steel plant with cleaner energy in Ohio, Trump’s running mate JD Vance’s home state.

“Copper and green energy are connected because so much copper is used in batteries and electric vehicles,” says Curry. “Copper is involved in all the key investment themes facing the world today. It embodies the demand around green spending, data centers, and deglobalization.”

But what about new sectors like AI, technology, healthcare and agriculture? Curry calls it “the revenge of the old economy” and we see it happening during past cycles.

The most recent period saw the shale oil boom put downward pressure on prices. Inflation and interest rates were low so investors moved into long-term assets like artificial intelligence stocks.

To replace capital that investors moved out of the physical goods market, governments around the world have created a demand shock through spending such as the Inflation Reduction Act and REPowerEU in Europe. Curry notes there will be $750 million spent on subsidies for green capex in 2024 alone.

Today’s demand drivers for commodities Curry groups under the acronym RED: redistribution, environmental policies and deglobalization.

An example of redistribution is covid-19 stimulus checks mailed out to lower-income Americans. The extra money went directly into consumption, not saving or investing. The lower-income group spends a higher percentage of their income on commodities.

E stands for environmentalism. It has to do with the amount of stimulus going to fight climate change. Greater than $16 trillion has been spent in this decade alone — equal to all of China’s spend during the 2000s.

Finally, deglobalization is the process of disconnection from other nations. China is a good example of this. China produces more electric vehicles than any other country, yet it also approved 106 gjgawatts of coal-fired power generation capacity last year.

“So, between coal and all the renewables, it is disconnecting itself from the rest of the world. That’s deglobalization,” Curry writes. “It goes to show you that these three themes that drive everything are all connected. You can connect deglobalization back to redistributionist policies. Think about tariffs. Why do you put tariffs on? To protect your manufacturing. All these countries are building out their own manufacturing. If you build out your own manufacturing, there’s more commodity demand, more capex, more physical everything.”

The role of inflation

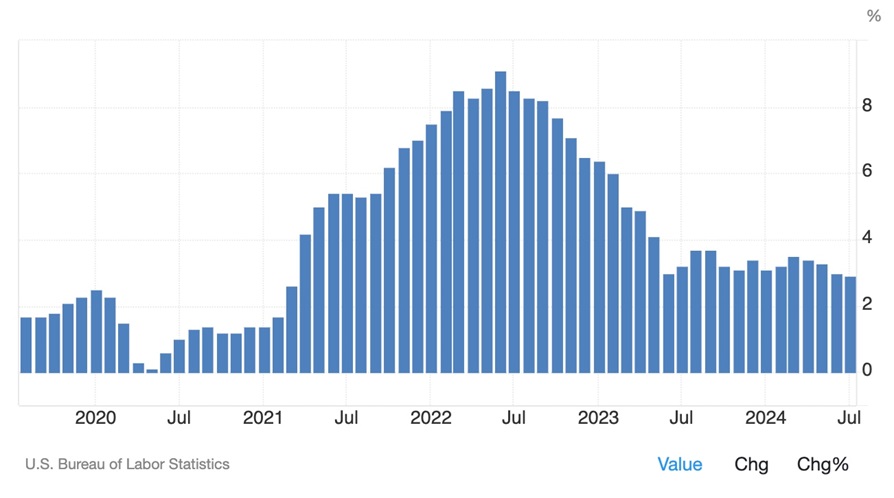

The final, most definitive indicator of a commodity supercycle is rising prices, and historically, supercycles tend to create inflation.

Over the past two years the Federal Reserve and other central banks have been fighting inflation that at one point reached the highest in 40 years; not since the early 1980s had price increases been so high.

The Fed raised interest rates to quell demand and bring prices down to its target inflation level of 2%. It worked. A series of rate hikes since the spring of 2022 lowered inflation from the 95 peak in June 2022 to the current 2.9%.

US inflation. Source: Trading Economics

A remarkable feat and achieved with a “soft landing”, i.e. no recession.

While some have argued that inflation would have come down anyway once covid-related supply chain wrinkles were ironed out, we are not among them. The Fed had to do something to slow runaway prices and monetary tightening/ rate hikes were the answer.

As The Economist writes in a recent article, “high interest rates not the passage of time have restored price stability”.

Another important point from The Economist article is that inflation may have stopped rising, but inflation isn’t gone; it has compounded over the years and the prices of many goods, including commodities, remain high.

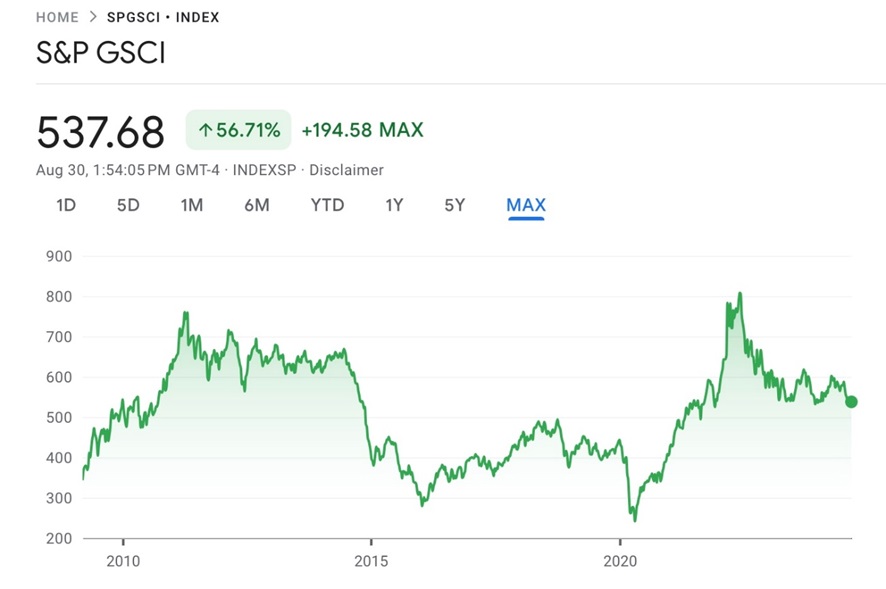

For proof of this, consult the chart below of the S&P GSCI commodities index. The index peaked in June 2022, lining up with the inflation peak, and has since declined. But commodity prices today, tracked by the index, are still the highest they’ve been since October 2014.

Source: Google Finance

Commodity prices have stayed buoyant despite relatively high interest rates, around 5%, high bond yields and a high dollar — all headwinds for commodities.

While the Fed’s attack on inflation hasn’t done much to reduce demand — consumer spending increased by 0.5% in July, and second-quarter GDP growth rose by 3% — a slowing labor market has the Fed looking at a rate cut in September.

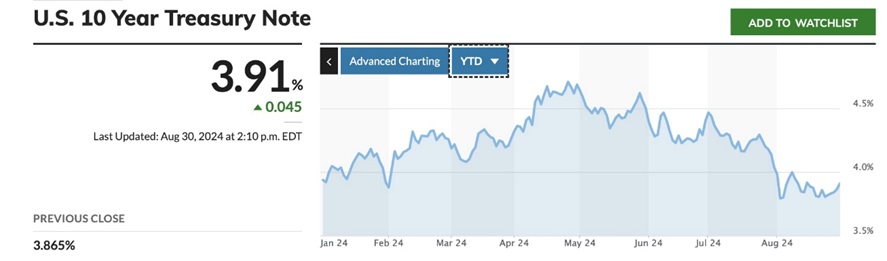

If interest rates are reduced, there will be an immediate effect on bond yields, which have already fallen this summer. The US 10-year Treasury note, for example, has gone from a year-to-date high of 4.7% in April to the current 3.9%.

Source: MarketWatch

Bond yields and bond prices have an inverse relationship. Could this be the start of a bull market for bonds, and a bull market for commodities once the triad of lower rates, lower bond yields and a lower dollar takes effect?

Look what happened to gold when the Fed last week telegraphed an interest rate cut. Spot gold set a record $2,531.60 on Powell’s dovish comments. Silver followed gold higher, breaking through $30/oz. Market participants should see this as a dry run for what actually happens when rates are reduced. Commodities and precious metals, imo, look like the place to be.

The new commodity supercycle is unique in the sense that supplies for several commodities are set to peak or have already peaked, causing market deficits and higher prices.

Previously, surging demand and falling supply are the hallmarks of a market in decline (i.e. coal). But now, it’s not so much about producers being reluctant to invest, but more of demand rising too fast for supply to catch up.

Copper

Take copper, for example.

On the demand side, electrical grids need to be updated, and governments are embarking on large-scale infrastructure investments that are copper-intensive.

Along with the usual applications in construction wiring and plumbing, transportation, power transmission and communications, there is now added demand for copper in electric vehicles, solar panels, wind turbines, and energy storage.

Additional copper is being demanded by the electrification of public transportation systems, 5G and AI.

Copper prices may have come off the boil recently (from a high of $5.11/lb in May) due to problems in China but the structural supply deficit is real and keeping prices elevated.

Benchmark Mineral Intelligence (BMI) forecasts global copper consumption to grow 3.5% to 28 million tonnes in 2024, and for demand to increase from 27 million tonnes in 2023 to 38 million tonnes in 2032, averaging 3.9% yearly growth.

Yet the US Geological Survey reports supply from copper mines in 2023 amounted to only 22 million tonnes. If the copper supply doesn’t grow this year, we are looking at a 6Mt deficit.

5 reasons why we are entering the next copper supercycle — Richard Mills

Copper: Humanity’s first and most important future metal — Richard Mills

Silver

One metal that has already plunged into deficit territory is silver. While often bought for investment purposes, silver is primarily used for industrial applications such as electronics and automotive. It’s also a key ingredient in solar panels, and as the world moves towards renewables, demand from that sector has grown exponentially.

The Silver Institute reported a 184.3 million-ounce deficit in 2023 on the back of robust industrial demand.

SI expects demand to grow by 2% this year, led by an anticipated 20% gain in the PV market. Industrial fabrication should post another all-time high, rising by 9%. Demand for jewelry and silverware fabrication are predicted to rise by 4% and 7%, respectively.

Total silver supply should decrease by 1%, meaning 2024 should see another deficit, amounting to 215.3Moz, the second-largest in more than 20 years.

Silver is in the fourth year of a shortage, with mined supply seemingly unable to keep up with demand, which is strongly influenced by the solar and electronics markets.

Silver looks ready to rip — Richard Mills

Iron ore

Admittedly the iron ore price has taken a beating of late, mostly due to the negative outlook for Chinese demand, which has been hit by a protracted property crisis.

Despite the government’s support for housing and other industries, on June 3 the iron ore price tumbled to its lowest in six weeks.

Earlier this week, however, the steelmaking ingredient was back above $100 a ton. Traders are seeing China’s drop in inventories as a tentative sign that the period of oversupply is starting to ease.

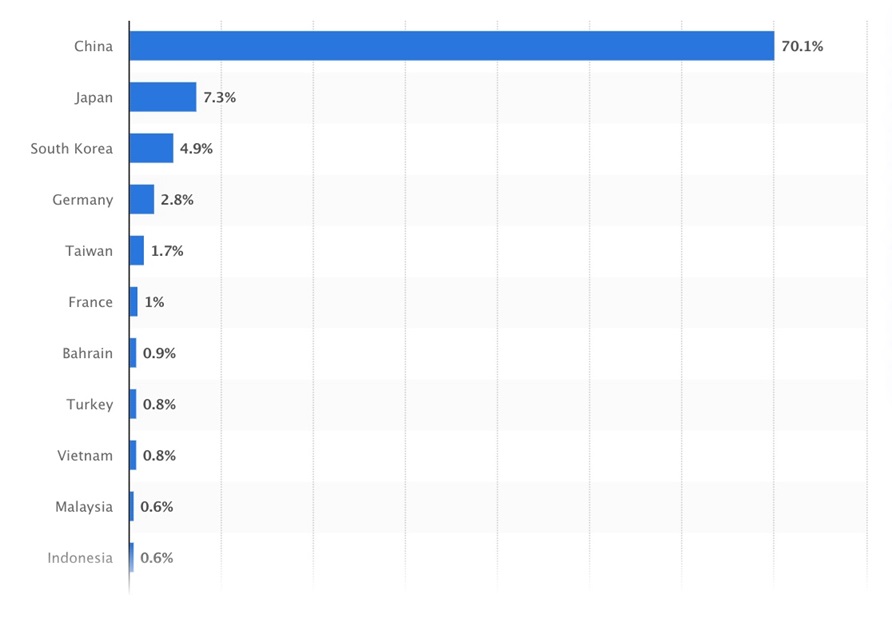

China imports the most iron ore of all countries, followed by Japan and South Korea.

Distribution of global iron ore imports based on value in 2021, by major country. Source: Statista

Conclusion

There have been multiple commodity super cycles throughout the course of history. The most recent one started in 1996 and peaked in 2011, driven by raw material demand from rapid industrialization taking place in markets like Brazil, India, Russia and especially, China.

The first green shoots of a new commodity supercycle, one based on raw materials for supplying the new electrified economy, are growing.

Silver and gold are up over 20% so far this year despite the headwinds of high bond yields and a strong US dollar.

Copper has come down from its $5 a pound pinnacle, but at $4.22 miners can still make money, although it’s not high enough to incentivize new mines.

Iron ore has had a tough go of it but it appears that the glut in supply is lessening and the price is basing around $100 a ton.

We know one thing for sure. The case for all commodities rests upon the US dollar. Once the Fed starts cutting interest rates, the dollar will weaken and the entire commodities complex will strengthen.

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter