Consumer Confidence Plunges

Apparently, the consumer does not feel he or she is part of the Fed’s economy, which we all know has inordinately benefited the rich at the expense of the rest—particularly at the rising expense of the rest who have faced years of soaring prices because of the Fed policies that juiced financial markets for the 1%. Consumers, at least, do not describe the same thing the Fed does when it describes the economy. It is like the two are looking alternate realities.

Consumer confidence in the Fed’s “strong” economy took its biggest one-month plunge in three years, and the reasons given were both declining jobs and rising inflation. These are exactly the metrics I’ve focused on as being the most critical to the Fed’s plans for a soft landing and the economic realities we’ll actually be facing.

The board’s consumer confidence index slid to 98.7, down from 105.6 in August…. By contrast, the index had a reading of 132.6 in February 2020, a month before the Covid pandemic hit….

“Consumers’ assessments of current business conditions turned negative while views of the current labor market situation softened further. Consumers were also more pessimistic about future labor market conditions and less positive about future business conditions and future income,” said Dana Peterson, chief economist at The Conference Board.

The last time the confidence index dropped more came as inflation was just beginning a climb to what ultimately was the highest level in more than 40 years.

Consumers, apparently, are seeing things as I’ve been seeing them, even in terms of the second rise in inflation this year that I’ve expected to begin again about now. So, I may be off-track with what the Fed and Biden administration are presenting but not with what consumers are sensing:

On inflation, the 12-month outlook rose to 5.2%, with concerns over price increases topping the list of economic concerns.

That is even more likely now that the Fed has lowered interest rates by a large chunk.

For the first time since 2005, however, the Fed experienced a voice of dissent over the scale of the move when it voted recently to lower its base interest target by half a percent. Fed Gov. Michelle Bowman thought the large-scale interest cut would communicate the things I said it did communicate:

Bowman cited several specific concerns: that the big move would indicate that Fed officials see “some fragility or greater downside risks to the economy”; that markets might expect a series of large cuts; that large amounts of sideline cash could be put to work as rates fall, stoking inflation; and her general feeling that rates won’t need to come down as much as her fellow policymakers have indicated.

She worries that this large cut could reignite inflation.

Consumers increasingly believe recession is already here

There was even an uptick in the number of consumers believing we’re already in a recession. These people aren’t buying what the Fed is selling any more than I have been.

Danielle DiMartino Booth, a former Fed advisor, says the market is in for a ‘rude awakening’ about the upcoming U.S. GDP report. She believes the GDP error on recession I’ve been talking about is about to be proven, just like the errors in government jobs reports were recently proven.

According to her, the Fed cut interest rates more than expected because it expects negative revisions to past GDP prints just like we saw to job reports. And that is essentially the explanation I also put forward for the Fed’s emergency-scale rate cut—the Fed fears something about the economy and recession that it is not letting on.

She also notes that unemployment does not look as bad as it actually is because we’ve seen seventeen straight months where Americans have exhausted their unemployment benefits, and that means all those people have rolled off the unemployment roll even though they didn’t find work.

She says, that all twelve Fed regions in the Fed’s “Beige Book” have flagged falling consumption. In such a consumer-based economy, Fed Chair Jerome Powell has to be concerned about that, and falling consumption does not square well with the rising GDP that has been reported by the Biden government.

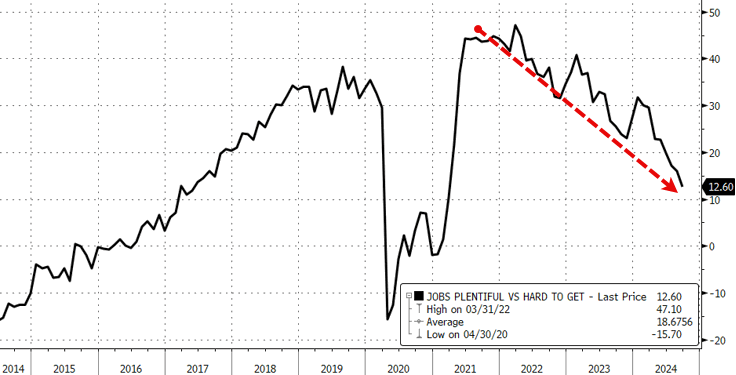

You can see here how much the labor market has softened compared to the tightness the Fed sees in its broken labor metrics and the phony Bidenomics Lying Statistics (the BLS labor reports):

The real-world experience out there is that we’ve fallen back about seven years and are now halfway back to the absolutely abysmal Covid lows.

********

David Haggith publishes The Daily Doom and writes satire. The Daily Doom contains economic, social, and political news about our troubled times--a non partisan weekday collection of the most consequential stories about our complex times with insightful editorials and weekly economic analysis. As an equal-opportunity critic of America's sharply divided, two-ring political circus, David divides his satire into sister publications so you can pick the one you find agreeable and ignore her sassy sister.

Support David Haggith by subscribing on Substack.