Dennis Gartman's Vision On The Road To Damascus Global Central Banks' US Treasury Reserves

Dennis Gartman exemplifies the gold punditry all too frequently seen on television financial programming. I'm sure Mr. Gartman is a decent guy. I'm not questioning his integrity. It's obvious he takes pleasure in sharing his knowledge with the general public in his television appearances. So, understand that my intent is not to call him out, or belittle him, but to make a point that Mr. Gartman seems to have had an epiphany of sorts in the past few days when it comes to "monetary policy."

Just last September, with gold just below $1300, I saw the following Gartman quote on the internet.

"It [gold] is not just over-extended to the upside; it is hyper-extended. It is not just overbought; it is hyper-overbought. We cannot strongly enough urge everyone to avoid buying gold here and we shall go so far as to suggest that those who are long begin the process of quietly heading for the exits and to reduce their positions to the most minimal "insurance" positions possible." -- The Gartman Letter, late September 2010

So just eight months ago, Mr. Gartman was more concerned about how many dollars it took to purchase gold, rather than the viability of the dollars used in the purchase. Then just this week, I saw something attributed to him that that smacks of latent goldbuggery!

"Last night the Fed. St. Louis reported yet again that the adjusted monetary base rose sharply once again, to a new record high …in only five months the base has risen 30%. We do not even wish to annualize that preposterous increase. All we can do is shake our head as this number runs skyward each week, asking how it was that we applauded the Fed so openly in the past for its administration of the nation's monetary affairs during the problems of '08 and the recession that followed only to have these same authorities act in this reckless manner now? Where are the adults, we ask? It is a reasonable question, and we ask again, where are the adults?" -- The Gartman Letter, late May 2011

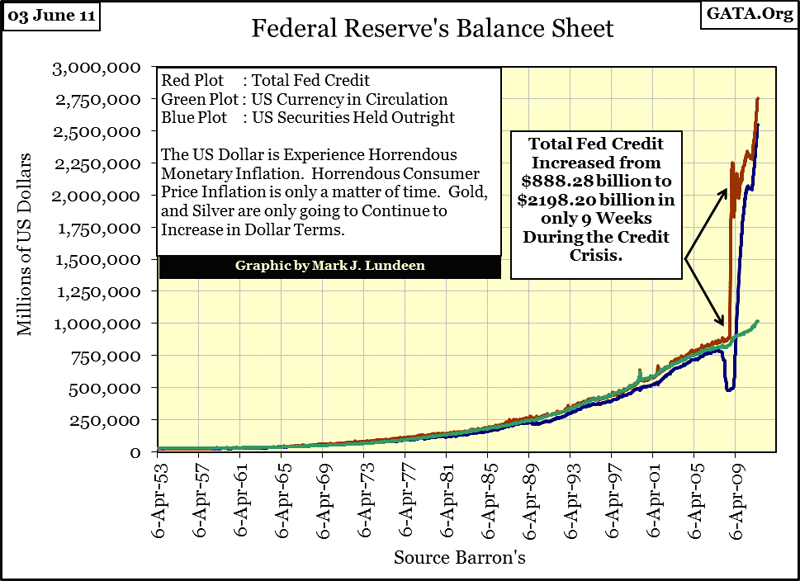

Mr. Gartman: long before Alan Greenspan became Chairman of the Federal Reserve in August 1987, highly trained "adults" managed the monetary affairs of the world's reserve currency. The only thing that has changed since 2008 is that you have begun to understand, if yet to fully accept, that the adults managing the Federal Reserve are a cabal of incompetent monetary quacks, and always have been. Maybe the guys over at Le Metropole Café (myself included) are not so wrong after all! You complain about a five month, 30% increase in the monetary base. How did you (and everyone else at CNBC), manage to miss Doctor Bernanke increasing Total Fed Credit by 147% in only 9 weeks during the credit crisis? Barron's has been publishing the Fed's balance sheet data weekly since the late 1930s!

Could it be that for decades, you (and CNBC's entire viewing audience) have remained ignorant of the Fed's malfeasance because people like Steven Liesman (CNBC's economic guru) have made careers of slavishly parroting the party-line from the Federal Reserve's press office? This chart showing Doctor Bernanke doubling then tripling the Fed's balance sheet should have been breaking news in December 2008, two and a half years ago, with frequent updates since then. As atrocious as this chart looks, and it looks plenty bad, there are worse looking charts that could be plotted from Barron's historical data set.

It's not just the Federal Reserve monetizing US Treasury Debt! For a very long time, "Monetary authorities" in all 24 time zones have been trashing their money supplies with inflationary purchases of US Treasury debt, and "injecting" the residue into their banking systems. The chart below shows the total dollar value of central bank purchases of Treasury debt over the last decade and a half. These purchases were all financed with monetary inflation created by the world's central banks' open market operations. Mr. Gartman, here is the fountainhead of "liquidity" that has fueled devastating bubbles in financial assets and real estate for the past two decades, and why the economies of the world now sit on the edge of a deflationary abyss.

Any competent historian of classical empires could have predicted our current situation, such as the following quote on China's Sung Dynasty's (960-1127 AD) experience with paper money.

"Such were the sources of that flood of paper money which, ever since, has alternatively accelerated and threatened the economic life of the world." -- William Durant: Our Oriental Heritage, (1935) pg. 779-80

Well, this may be all news to you, and everyone else at CNBC, however the world's central banks are looking at the data the Fed publishes weekly, and there have been signs of buyer's regret from America's largest creditor. Note the date of the quote, over two years ago.

"We hate you guys. Once you start issuing $1 trillion-$2 trillion [$1,000bn-$2,000bn] . . . we know the dollar is going to depreciate, so we hate you guys but there is nothing much we can do." -- Luo Ping, a director-general at the China Banking Regulatory Commission, 11 February 2009

But we all know it's not what people say that matters, but what they do. And as shown in the chart above, global central banks (blue plot) continue to purchase US Treasury debt in ever greater quantities. However, when we compare these purchases as percentages of the total US national debt (next chart), a different picture of foreign central bank behavior emerges: since July 2008, central banks (blue plot) have refused to monetize more than 25% of the total float of the Treasury market.

The Fed's reaction to this development has been completely predictable. Since early 2009 (five months after the Fed's foreign colleagues slowed their purchases) the Fed began their panic purchases of US Treasury debt, increasing their presence in the Treasury market to 17.5% of the total float. So, for over two years the Fed has monetized the national debt faster than Washington's politicians have increased it. That makes concerns of hyper-inflation in the dollar economy completely rational.

Those forward thinking people who have wisely swapped their central bank's funny-money for gold and silver anytime in the past ten years, need not apologize to anyone in the financial media for their prudence. And not only that, but with the whiz-kids currently staffing the "policy" desk at the Federal Reserve, now is * not * the time to sell gold and silver!

So far, we have looked at monetized Treasury debt in two line items:

- Treasuries purchased by Foreign Central Banks

- Treasuries purchased by the Federal Reserve

However, combining these two series into one called "global monetary reserves", we can see what central banking, as a government created institution, has done to the world's money supply. The chart below has three line items:

- Red Plot ---: US National Debt, (read off left scale)

- Blue Plot --: Global Monetary Reserves, (read off left scale)

- Green Plot: Percent of US National Debt Monetized by Global Central Banks, (read off right scale)

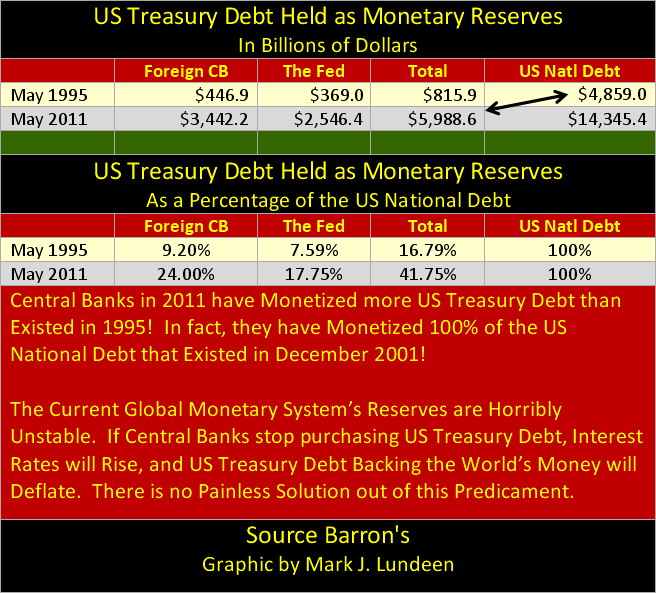

As the US national debt grew to $14.34 trillion dollars, from $4.85 trillion in May 1995, global central banks have increased their holdings of US Treasury debt to 42% of the entire US Treasury market, from only 17% in May 1995. And what has the Federal Reserve been doing with all the inflation they've been creating? The following quotes by respected figures in the media make it clear that Doctor Bernanke, as Doctor Greenspan before him, have been rigging the valuations of financial assets upwards, and the suppression of the price of gold, silver and precious metal miners, the traditional hedges against rising consumer prices, is a logical inference.

"Well, what I just want to talk about for a few minutes is the various efforts that are going on in public and behind the scenes by the Fed and other government officials to guard against a free-fall in the markets -- the Fed in 1989 created what is called a PLUNGE PROTECTION TEAM (emphasis by Lundeen, conspiracy theory by ABC News' George Stephanopoulos), which is the Federal Reserve, big major banks, representatives of the New York Stock Exchange and the other exchanges, ---they have been meeting informally so far, and they have kind of an informal agreement among major banks to come in and start to buy stock if there appears to be a problem. They have, in the past, acted more formally" - George Stephanopoulos, former Clinton adviser, Monday September 17, 2001 ABC's Good Morning America

* * *

"One reason that monster declines are less likely now is that investors recognized something that they didn't in 1987: The Federal Reserve is on their side." -- Andrew Bary, Barron's 15 October 2007 issue

* * *

"Policies have contributed to a stronger stock market just as they did in March 2009, when we did the last iteration of this. The S&P 500 is up 20% plus and the Russell 2000, which is about small cap stocks, is up 30% plus." -- Doctor Benjamin Bernanke, CNBC Interview with Steve Liesman 13 Jan 2011 (1:40 PM).

* * *

In light of these facts, published weekly in the statistics pages of Barron's, and admitted "policy" activities, reported in the public domain, it would be naïve to attribute our current low bond yields in US Treasury debt, and 30 year mortgage rates to market forces. This is also true for the world's corporate bond and stock markets. We should all beoutraged that the world's "policy makers" have engaged in a multi-decade long, price fixing scheme that has consumed 42% of the US Treasury market for its fuel, while highly regarded market commentators, and academics sit in front of a TV camera like monkeys; seeing, hearing, and speaking no evil.

This price fixing scheme's end game will prove no different than any other ill-advised market rig. That the market manipulators are supported by the highest authorities in Washington and elsewhere will make no difference. Those assets that benefitted from the rig, will deflate, those assets that were suppressed will inflate from the inflationary blow-back. As the current market rig is of historic proportions, so will be its inevitable consequences.

The table below lists the start of my data and latest data points of the world's journey into a hyper-inflationary hell.

As we can see in the table above, in 2011 global central banks have monetized more US Treasury debt than evenexisted in 1995. In fact, they have monetized 42% of the $14.34 trillion dollar total of today's US national debt. The chart below is a way to visualize the trap the world's central banks now find themselves in. All the US Treasury debt that existed at the time of the 9/11 terror attack on the World Trade Center, has been monetized by global central banks.

In laymen's language, what that means is that the Fed and the world's central banks have purchased, and now own an amount of US Treasury bonds equal to the total US National Debt as of December 2001, and are currently holding them on their books, and are currently collecting interest on them from the US Treasury. So, central banks purchased the sum all the US Treasuries in existence in December 2001 using freshly printed money that cost them ABSOLUTELY NOTHING TO CREATE! Without this massive intervention in the bond market, and massive artificial expansion of the existing supply of money, the 10 Year US Treasury Bond Yield would likely be above 8% today rather that 3%, and there never would have been a US housing bubble or stock market bubble.

Central bankers have shaped our world to their specifications. But other than marginalized groups like GATA, who is there to educate the public of the raw deal Washington, Wall Street, economists at Harvard and Yale, and their colleagues in countries around the world are dealing out to the average citizen?

So Mr Gartman, when the markets see a soft patch, and the Dow Jones declines 2% in a trading session, the yields on the 10 T-notes typically decline. Is this from investors seeking the safety of the US Treasury market, or are the world's central banks fighting for survival in the only way they know how: monetizing an ever increasing percentage of the US Treasury market? I think it's the latter, meaning 42% down, 58% of the US Treasury Market to go!

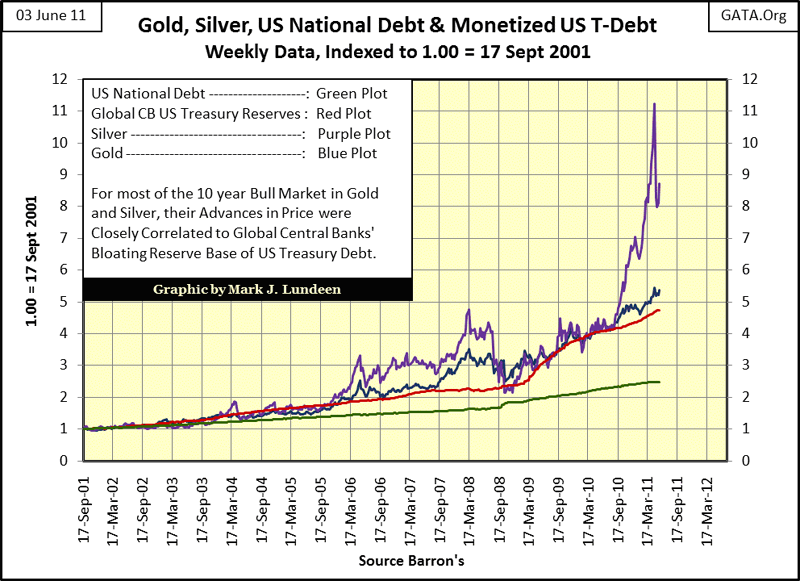

Not surprisingly, there is a relationship between the expansion in the global central bank's balance sheets to the price of gold and silver, as is evident in the chart below. For most of the past ten years, the indexed value of global monetized Treasury debt (Red Plot) has formed a hard bottom in the price corrections for gold and silver (Blue and Purple Plots).

Is this a coincidence? It just might be, but I find this a fascinating relationship nonetheless. Since last August, we see how the price of silver has broken free from its ties to the growth in global central banking reserves. The question is, will silver once again decline towards the red plot above, or will gold also break free from its ten year relationship to the growth in banking reserves? I expect it to break free sometime in the next year or two, and like silver, the price of gold will soar far above the rate-of-increase seen in the world's central banks balance sheets.

The table below is from a recent article of mine, showing the notional values of various futures markets. Previous to August 1971, when President Nixon severed the dollar's last link to gold, financial futures did not exist. Forty years later, the notional value of financial futures contracts are several orders-of-magnitude greater than that of those contracts trading real things, like grain, energy and metal.

There is something seriously wrong with an economy whose greatest source of risk is the money used in it, rather than the production and supply of goods and services created in it!

It would be a mistake to assume that just because financial assets begin to deflate, so too must traditional commodity prices. Rising interest rates are prime indication of deflating financial assets. The last time the economy suffered from rising interest rates was during the 1960s & 70s, a period also know for rising consumer prices and bull markets in grain, energy and the metals.

Mr. Gartman, some risks can't be hedged, such as having a Princeton man at the helm of the Federal Reserve. Somewhere, someday soon, something is going to happen that will start a selling panic in financial assets that will not be quelled by central banks monetizing America's un-backed IOUs. History's largest monetary experiment in credit creation and debt management, via derivatives, will go down in flames, if not next week or next year. Safety will only be found in capital flight from debt, to something real like gold and silver.

More from Gold-Eagle