Gold’s Pricing Power Moving East (Part 1)

How is the gold price made?

When we hear commentary on why the gold price has moved, we usually hear of U.S. economic or political factors and a move in the U.S. Dollar. Most times these do not precipitate the buying of physical gold.

What they do do, is to spur the buying or selling of futures or Options on the COMEX gold market. Many commentators attribute moves in the physical gold price to moves on COMEX.

But this link is tenuous, as COMEX does not [except for a maximum of 5% and minimum of 1% of contracts that disclose they will deal in physical gold, upfront] deal in physical gold.

The dollar gold price is the one that most investors look at, even though they may deal in a different currency to the dollar. This is because the dollar is the key global currency against which all others are measured.

Price differential between Shanghai and London/New York

U.S. gold prices today are primarily driven by demand for physical gold in gold ETFs, such as the Gold Trust and the SPDR gold ETF [GLD].

But the bulk of physical gold traded in the world now happens on the Shanghai gold exchange. There are 10 million investors, including 10,000 institutions that are able to deal over their cell phones at any time on the Shanghai Gold Exchange. Such a market dwarfs both London and New York on the physical front, as all transactions have to be backed by physical gold.

With gold exports not permitted from China, there are obstacles to the free flow of gold globally. The International Gold Exchange in Shanghai has not yet attracted sufficient numbers to allow this. But the major banks can and do hold stock both in Shanghai and London and by running a dollar/Yuan currency book can arbitrage gold between the markets to smooth out the bulk of price differences between markets.

While there are frequent fingers pointing to the ‘premium’ of Shanghai prices over those of London and New York of $5 all the time, it is because Shanghai prices 0.9999 quality gold whereas London prices 0.995 quality gold. One has to deduct this before comparing the prices in the two markets.

On top of this we see between $5 - $15 an ounce difference on a daily basis, which can include the cost of moving the gold from London to Shanghai.

On top of this cost lies the difference in liquidity between the markets and the differences in local demand and supply. In the very liquid Shanghai market, bullion banks do not exert the same influence as in London and New York, so speculation is restricted. It is further restricted by the much higher costs of taking large speculative positions in Shanghai. These costs were increased at the beginning of the year to discourage speculation.

Shanghai, as a result, gives less volatile prices, more indicative of [Chinese] physical demand. While no gold flows out of China [removing its downside pressure on the gold price] Chinese demand draws from the rest of the world.

Gold enters China from the rest of the world’s gold markets primarily via Switzerland where it is refined into metric bars. We see metric measures of gold dominating the global gold market in the future. Imports comes from all over the world in all forms, with a reducing amount coming in via Hong Kong.

Consequently, the Shanghai Gold Exchange gold price, although higher [for reasons given above] is exerting a growing influence on the global gold price in all currencies and better reflects the physical gold price of gold.

London, New York And The Gold Price

With London having been the global center of the physical gold world until recently, one would have thought that the influence over the gold price would have resided in London. But this is no longer so, as history over the last few years, has shown that London has usually followed COMEX prices.

Of course, this would give rise to charges of ‘manipulation’ from U.S. and other sources. The not uncommon bear-raids by the big U.S. banks and high frequency traders ensured that the gold price bore little resemblance to the real global physical gold demand and supply factors.

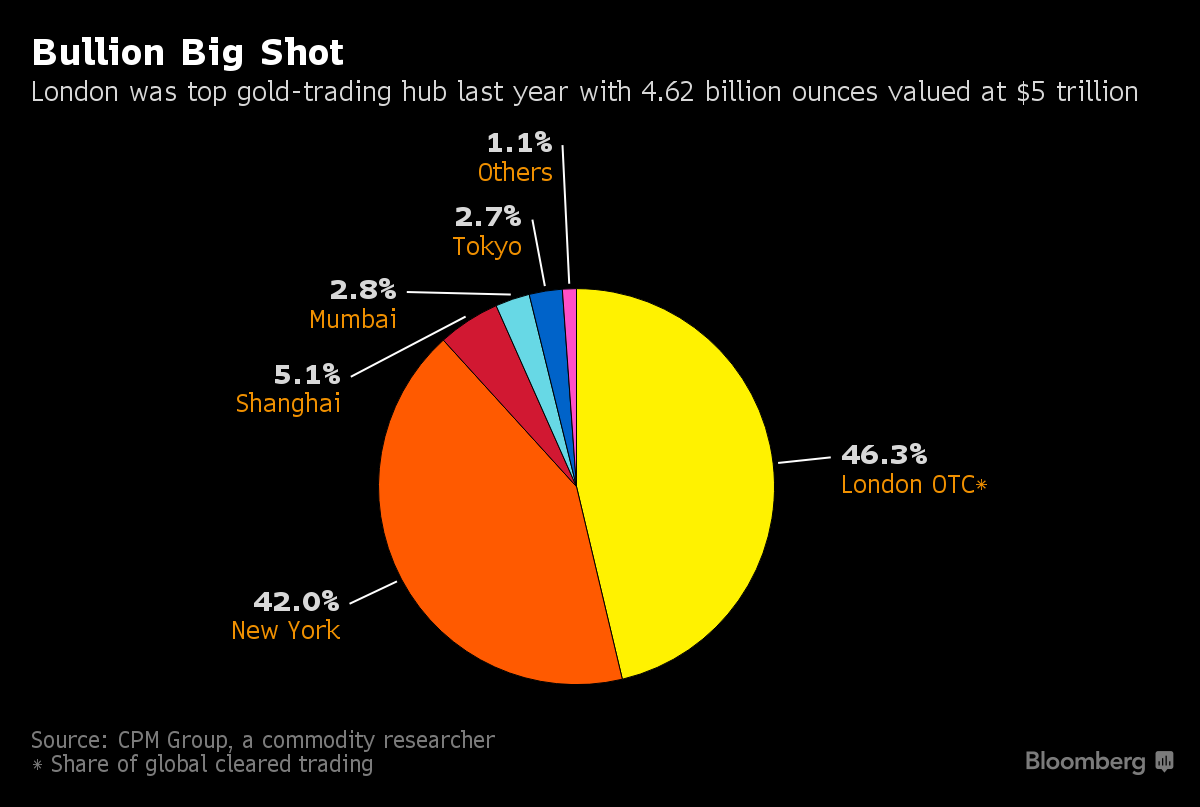

But on closer examination of the chart above, one sees that all but a small percentage of “gold” is traded not in gold but in some form of derivatives, such as shares in GLD, futures, options, or even gold shares, where the buyer does not own physical gold but a piece of paper to the gold price.

Take out this ‘paper’ gold and London and New York’s 88% of gold traded, falls to around less than 1% compared to Shanghai’s 5% of physically traded gold. i.e. five times as big.

When there is a real premium in Chinese gold prices over London and New York’s Chinese gold importers [Like the ICBC/Standard bank and HSBC bank] then export gold bullion to China to meet that higher demand and smooth out price differentials. Consequently, we have witnessed a steady very, very large flow of gold pass through the refineries of Switzerland [to be upgraded to 0.999 fineness] and onto the Far East.

This has allowed both Russia and China in particular, to acquire huge tonnages of gold [on top of their own production] at what really are, discount prices over the last decade!

With gold now an integral part of the Chinese financial and banking systems, China cannot afford to be at the mercy of the capricious, non-representative, U.S., physically-small gold market, even though the volumes of paper gold traded are huge as you can see in the pie chart above.

Day to day news items are not the real reasons gold is bought and sold in the west. It is the profit motive inherent in western financial markets, driving traders and funds to buy and sell gold frequently. Gold holdings are changed even by large funds from day-today positions to monthly or three monthly. There are few that hold a long-term holding. The demand for short-term performance prevents that.

The Chinese View Of Gold

The motive east of Greece is to acquire gold holdings as a prime financial asset that, over time, provides secure wealth for the long term. Trading of gold is an ancillary function only. East of Greece it is the sheer volume of gold kilos held that’s important.

China’s gold holdings are far greater than the available statistics tell us. Gold is held as jewelry at retails levels, on the balance sheet of banks, in the Shanghai Gold Exchange, for clients, as well as for the Exchange itself, in government agencies, for the government and by the People’s Bank of China, for the nation.

In summary, as the People’s Bank of China put it, “We own gold through the people of China!”

This is resulting in China moving to take over gold’s global pricing power.

In Part 2:

- China excluded from the global gold price or arbitrage includes it?

- Shanghai twice daily Gold Fixes

- De-Globalization, Protectionism and Capital Controls

- Is the Yuan a problem in pricing gold?

This will ensure a 24-hour global gold market where prices relate to the gold market and not to the U.S. economic situation.

A word to gold investors - Simply holding gold overseas will not be enough. We are happy to send you a guide on just how to hold your gold effectively out of the reach of the authorities in your Jurisdiction.

It will be the gold investor that ensures he is outside the reach of confiscating authorities that will retain his gold and ensure he profits from those rocketing prices.

********

There are no gold custodians or dealers that are geared to protect their clients with the exception of one we know of – www.Stockbridgemgmt.com.Contact them at [email protected]

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Julian D. W. Phillips makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Julian D. W. Phillips only and are subject to change without notice. Julian D. W. Phillips assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, we assume no liability for any direct or indirect loss or damage which you may incur as a result of the use and existence of the information, provided within this Report.

Julian Phillips is the Founding Partner of Gold Forecaster - Global Watch and Silver Forecaster [incorporating Platinum]. Mr. Phillips analyzes the gold, silver, and platinum market alongside the macro economic currency aspects of these precious metals. He covers the shares involved in these sectors and publishes numerous articles on specialist websites concerning precious metals. Mr. Phillips is also a specialist in Exchange Controls and international currencies. He has qualified to be a member of the London Stock Exchange. His working life has focused on Gold/Currencies/Fund Management and now Silver and Platinum. Additionally, Mr. Phillips has spent some years in capital creation in currency distressed countries through exchange control incentives. Mr Phillips is also the Chairman of Stockbridge Management Alliance Ltd. a company that offers gold storage in a way designed to prevent its confiscation should such an order be issued in any country. His websites are at http://www.goldforecaster.com and http://www.silverforecaster.com/.

Julian Phillips is the Founding Partner of Gold Forecaster - Global Watch and Silver Forecaster [incorporating Platinum]. Mr. Phillips analyzes the gold, silver, and platinum market alongside the macro economic currency aspects of these precious metals. He covers the shares involved in these sectors and publishes numerous articles on specialist websites concerning precious metals. Mr. Phillips is also a specialist in Exchange Controls and international currencies. He has qualified to be a member of the London Stock Exchange. His working life has focused on Gold/Currencies/Fund Management and now Silver and Platinum. Additionally, Mr. Phillips has spent some years in capital creation in currency distressed countries through exchange control incentives. Mr Phillips is also the Chairman of Stockbridge Management Alliance Ltd. a company that offers gold storage in a way designed to prevent its confiscation should such an order be issued in any country. His websites are at http://www.goldforecaster.com and http://www.silverforecaster.com/.