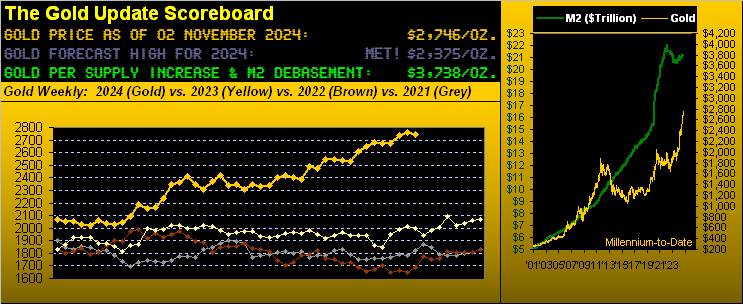

Gold’s Highs; Inflation’s Rise

Gold’s Highs … Gold just recorded its 16th All-Time Weekly High within the 44 trading weeks that have completed the first 10 months of this year. Price by Gold’s “continuous front-month contract” (at present that for December) tapped 2800 for the first time ever in reaching up to 2802 this past Wednesday.

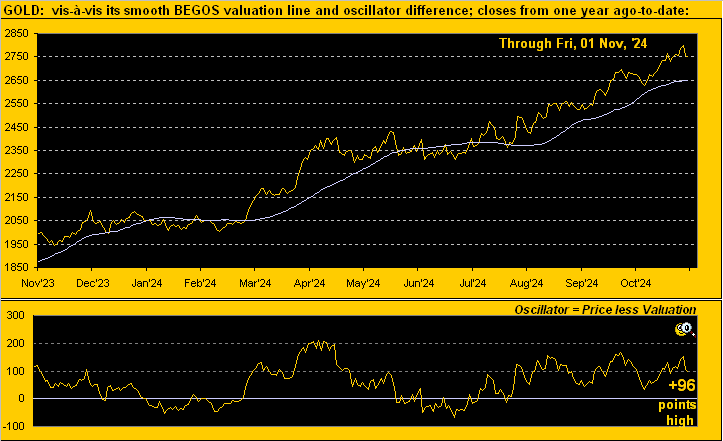

‘Course — as has been our ongoing take of late — Gold whilst still long-term vastly undervalued per the above Scoreboard’s 3738 Dollar debasement level vs. yesterday’s (Friday’s) actual settle at 2746, price near-term remains overvalued per our following Market Value gauge. Such measure assesses Gold’s typical movement relative to that of the primary BEGOS Markets (Bond / Euro / Gold / Oil / S&P 500) which at present shows the yellow metal as +96 points “high” above its smooth valuation line to which inevitably price reverses:

Still, we maintain that Gold’s deviation from its BEGOS valuation merely underscores the run of justly due buying. In fact, across these 16 years of producing The Gold Update, never do we recall so many folks whom we encounter on a day-to-day basis questioning us about Gold. And given its significant undervaluation relative to currency debasement, we regularly point out that — despite Gold’s run of record highs — most broadly ’tis still cheap … as is Silver relative to Gold … the white metal indeed super cheap. Updating the math there: valuing Gold at 3738 and applying the century-to-date Gold/Silver evolving average ratio of 68.5x puts Silver at  54.57! That is +67% above her present price of 32.58. Why, even applying said average ratio vis-à-vis today’s Gold level of 2746 places Silver some +23% higher at 40.09, the actual ratio at present being 84.3x. Thus we repeatedly reprise: Do not forget Sweet Sister Silver!

54.57! That is +67% above her present price of 32.58. Why, even applying said average ratio vis-à-vis today’s Gold level of 2746 places Silver some +23% higher at 40.09, the actual ratio at present being 84.3x. Thus we repeatedly reprise: Do not forget Sweet Sister Silver!

As for Gold itself, by the weekly bars from one year ago-to-date, we can only cue Nat King Cole from back in ’51 with“Unforgettable…”:

And yet whilst Silver by valuation significantly trails Gold, year-to-date the white metal +35.6% again tops the table of our BEGOS Markets, the yellow metal a close second +32.5%, with the inanely overvalued “Casino 500” rounding out the podium placers +20.1%. Note therein that the Dollar Index is actually positive (given yields backing up and the Bond being in the cellar): just a friendly reminder that Gold plays no currency favourites:

To the precious metals’ equities we go, the graphic ever so exemplary of the adage “Live by the leverage, die by the leverage” notably with respect to Newmont (NEM). The company’s Q3 earnings of 81¢/share more than doubled those of a year ago (36¢/share): but the stock was taken out behind the woodshed for having missed the consensus estimate of 86¢/share. Bummer.

Still from the top down by their percentage tracks from a year ago-to-date we’ve Agnico Eagle Mines +83%, the Global X Silver Miners exchange-traded fund (SIL) +59%, Pan American Silver (PAAS) +57%, the VanEck Vectors Gold Miners exchange-traded fund (GDX) +42%, Gold itself +38%, Newmont (NEM) +21%, and Franco-Nevada (FNV) back in the black +10%. The equities perhaps are not for those faint of heart, but well-suited for the long-term smart:

Gold’s highs, indeed. ‘Tis been thus far an amazing year. But is inflation, dare we say stagflation, perhaps to appear?

Inflation’s Rise … All the broad measures of inflation data are in for the month of September. And with respect to the so-called “Fed-favoured” inflation gauge of Personal Consumption Expenditures, ’twas hailed by Dow Jones Newswires this past Thursday as follows: “PCE inflation edges closer to Fed’s 2% target, keeping FOMC on track for next interest-rate cut.” A bit of a stretch that, especially as we do the math. To be sure, the headline PCE 12-month summation dropped from August’s 2.2% to 2.0%. But then we’ve the big BUT: that for the core PCE was maintained at +2.6%, — and moreover — the month’s annualized pace increased for the headline number from +1.2% in August to +2.4% for September. Even worse, the core number rose from 1.2% as well to 3.6%. Whoops! Here’s our updated table:

So following September’s leap in core PCE inflation came October’s job creation of a scant 12,000 non-farm payrolls (vs. the consensus expectation for 123,000 after 223,000 in September), and thus our justification for having mentioned the word stagflation. Still, mitigative to that may be the recent rising of the Economic Barometer as shown here from a year ago-to-date, the red-line S&P 500 indicative of investors keeping stocks on their plate despite some mild selling of late:

“The S&P has been coming back down, mmb, but to call it ‘mild’?”

Nobody tees it up better than Squire. His observance notwithstanding, the wee rightmost drop indeed is comparatively “mild” relative to the increase in the S&P year-over-year. And of even further import, here (employing “trailing 12-months earnings”) is the truthfully “live” price/earnings ratio of the S&P 500, duly including these two most recent consecutive down weeks:

At least we can offer a hat-tip to the mighty Swiss-based UBS, whose Nicolas le Roux-led strategy team just penned the bank’s expectations “…for equities to cheapen relative to bonds…” Perhaps Nico and company have been reading The Gold Update and the website’s daily Prescient Commentary both of which have gone on ad nauseum for months about same. Just in case you’re scoring at home, the all-risk S&P yield is presently 1.293% whilst no-risk U.S. debt across the maturity spectrum yields better than 4%. (Which means for you WestPalmBeachers down there … no, forget it … you’re too pre-occupied in trying to figure out how to do a ballot).

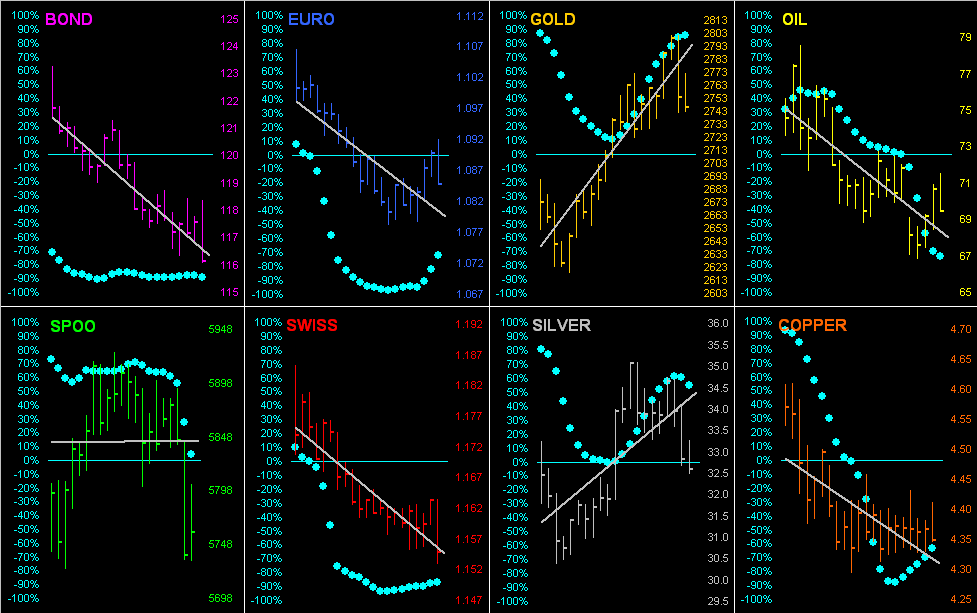

Meanwhile, it being month-end (plus one trading day), ’tis time to go ’round the horn for all eight of our BEGOS Markets from a month ago (last 21 trading days)-to-date, featuring their respective grey linear regression trendlines and “Baby Blues”, the dots denoting the consistency of said trends. Focus here ought be on both the Euro and Copper, their “Baby Blues” having curled up from beneath the -80% level, the rule-of-thumb being to then anticipate higher price levels near-term:

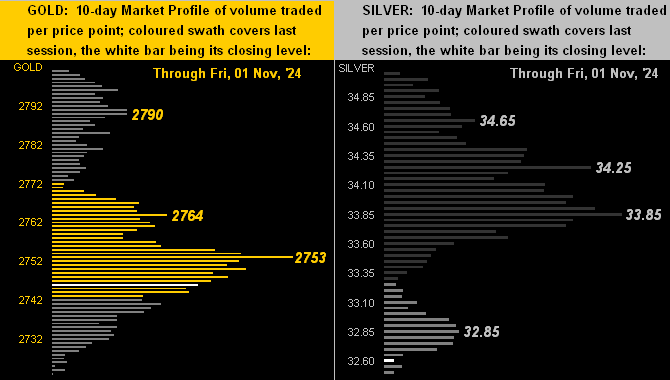

Too, we’ve the 10-day Market Profiles for the precious metals, featuring Gold on the left and Silver on the right. In both cases, their dominant volume price resistors are as labeled:

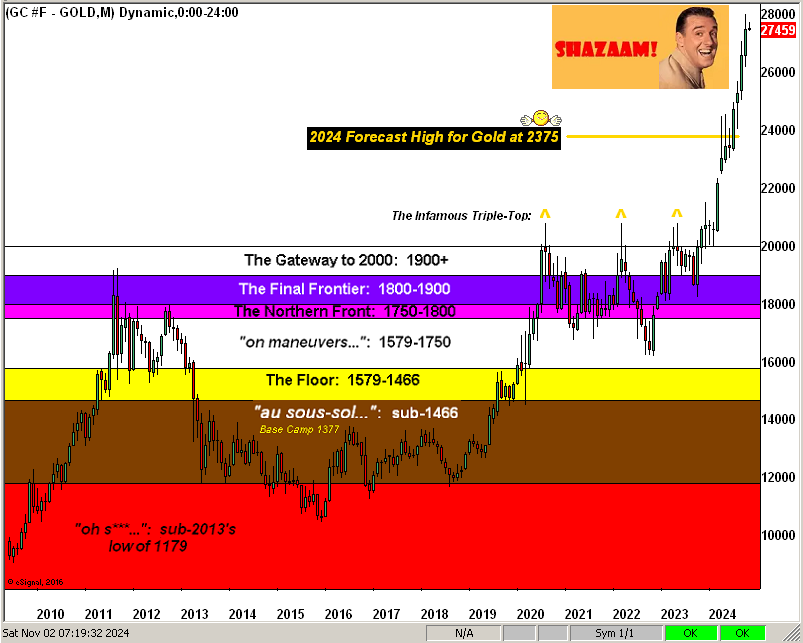

And as is our wont to write, ‘twouldn’t be month end (and a day) without the stratified Gold Structure by the month from 16 years ago-to-date. Yes, Gomer, you tell ’em: for our Gold of late ’tis been nothing but “SHAZAAM!” mate:

StateSide there’s an election next week. Just as the frequency with which we’re asked about Gold these days has been inexorably on the increase, so too are we questioned: “Who’s gonna win?”

‘Course, nobody knows, and sentiment varies based on one’s favoured sources of information, given that 99.999% of us have never actually met (let alone personally know) either the “current democrat” nor the “former democrat”.

But the one point upon which all seem to agree is — regardless of who “wins” or is “declared” the next President — there shall be an ensuance of StateSide chaos both in the markets and (hopefully still) civil society. Gold, too, could certainly get banged about a bit: again, ’tis near-term overvalued. But because ’tis long-term undervalued — be it on the left or on the right — Gold is far and away the best candidate to keep your future bright!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

********

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.