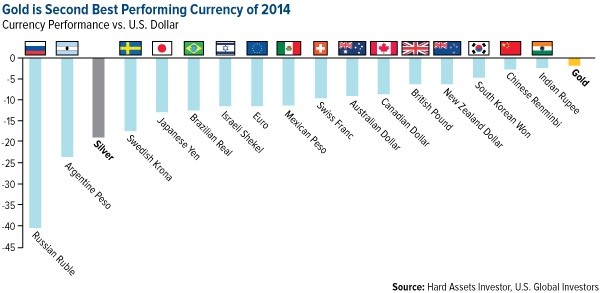

Gold Beats All Other World Currencies In 2014

“Gold is money. Everything else is credit.” ~J.P. Morgan in 1912

Loyal readers of our Investor Alert and my blog Frank Talk are no doubt aware that the U.S. dollar’s rising strength has put pressure on commodities such as oil and gold. I wrote about this as recently as my roundup of the top commodities stories of 2014, which you can read here.

Gold took a blow in the second half of 2014 as a result of the dollar’s ascent, and sentiment toward the yellow metal right now is less than ideal. But to keep things in perspective, its performance this year has far outpaced that of 2013, when it fell 28 percent—its worst showing since early into President Reagan’s first term.

Even though gold has lost 0.8 percent year-to-date as of this writing, it still leads all major world currencies except for the U.S. dollar.

The Case for Gold as Currency

In his most recent book, former Federal Reserve Chairman Alan Greenspan convincingly makes the case that gold is indeed money:

Yet gold has special properties that no other currency, with the possible exception of silver, can claim. For more than two millennia, gold has had virtually unquestioned acceptance as payment. It has never required the credit guarantee of a third party. No questions are raised when gold or direct claims to gold are offered in payment of an obligation; it was the only form of payment, for example, that exporters to Germany would accept as World War II was drawing to a close.

Yet gold has special properties that no other currency, with the possible exception of silver, can claim. For more than two millennia, gold has had virtually unquestioned acceptance as payment. It has never required the credit guarantee of a third party. No questions are raised when gold or direct claims to gold are offered in payment of an obligation; it was the only form of payment, for example, that exporters to Germany would accept as World War II was drawing to a close.

Greenspan goes on to make another astute point. If gold is nothing more than a commodity, then why do most developed countries’ central banks see the need to hold the stuff? Wouldn’t some other commodity suffice? Diamonds perhaps, or soybeans?

During a Congressional monetary policy meeting in 2011, Texas Representative Ron Paul squared off against former Fed Chairman Ben Bernanke over this very topic. When asked why central banks still insist on holding the precious metal in their reserves, Bernanke responded that it was simply tradition.

Tradition, yes, but the reason goes so much deeper than that. Gold has an intrinsic value that transcends its commodity-ness, something that’s recognized by nations all over the globe.

For example, we’re seeing a trend among European central banks seeking to bring their gold reserves back under their jurisdiction. Although Switzerland recently voted down a referendum that would have done just that, there’s talk now that Austria, Belgium and France are interested in shoring up their own gold reserves. The Netherlands and Germany have already brought some of their gold home.

China and India’s central banks are in the buying mood. Russia is currently snapping up gold at an astounding rate: 130 tons this year alone, up 73 percent from 2013.

China and India’s central banks are in the buying mood. Russia is currently snapping up gold at an astounding rate: 130 tons this year alone, up 73 percent from 2013.

Of course, if you’re Russia, buying that much bullion makes perfect sense. When your currency is the worst-performing in the world, you sorely need something in your coffers with greater value, ample liquidity and no credit risk.

Diversify and Rebalance

For the rest of us, gold remains an exceptional instrument to diversify your portfolio with. Despite its decline midway through the year, its price has remained relatively stable, much more so than oil’s. What investors—especially the gold bears—need to remember is that bullion has a 12-month standard deviation of ±18 percent, meaning that its price action this year is well within normal behavior.

As always, I advocate a 10-percent weighting in gold: 5 percent in physical metal, 5 percent in equities, then rebalance every year.

Speaking of which, look out for my special New Year’s edition of the Investor Alert this Friday. I’ll be discussing what steps you can take to maximize your portfolio going into 2015!

********

Past performance does not guarantee future results.

Standard deviation is a measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is also known as historical volatility. Diversification does not protect an investor from market risks and does not assure a profit. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

********

Courtesy of http://www.usfunds.com

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com. You can contact Frank at: [email protected].

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com. You can contact Frank at: [email protected].