Gold Clings to Its War Premiums

share

share

share

share

share

share

share

share

share

share

Despite material struggles across other areas of the commodities market, the yellow metal remains relatively elevated.

Growth vs. Inflation

With our GDXJ ETF short position continuing to produce profits, miners’ weakness alongside gold’s strength highlights how bears and bulls can make money in this market.

However, with the yellow metal poised to follow the junior miners lower over the medium term, the poor domestic fundamental outlook should outweigh gold’s geopolitical optimism.

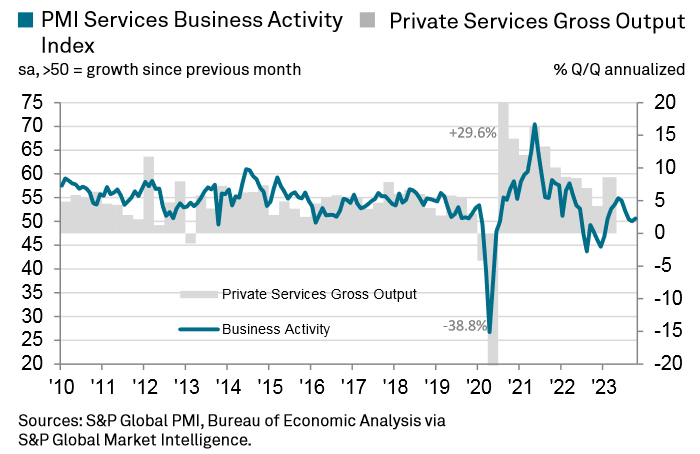

For example, S&P Global released its U.S. Services PMI on Nov. 3. And since output prices “cooled to the softest since October 2020,” growth has overtaken inflation as the main problem confronting the U.S. economy. Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, said:

“The PMI survey paints a far more subdued picture of U.S. economic health than the latest bumper GDP numbers, with October seeing very muted growth of business activity for a third successive month.

“A summer-surge in service sector activity, fueled by rising consumer spending, has stalled. Manufacturing is meanwhile also struggling to regain momentum amid weak global demand. As such, the survey data are broadly consistent with GDP rising at an annual rate of around 1.5%.”

Please see below:

To explain, the blue line above tracks S&P Global’s U.S. Services PMI, while the gray bars above track private services gross output. If you analyze the former’s decline on the right side of the chart, you can see why the firm expects GDP growth to come in below potential (2%). Consequently, silver is firmly in the crosshairs, as economic-induced volatility should hit the white metal and the miners the hardest.

As further evidence, the ISM also released its Services PMI on Nov. 3. Anthony Nieves, Chair of the ISM Services Business Survey Committee, said:

“The services sector continues to slow, with decreases in the Business Activity and Employment indexes. Sentiment among Business Survey Committee respondents' comments is mixed, with some optimistic about the current steady and stable business conditions and others concerned about such economic factors as inflation, interest rates, and geopolitical events.”

So, while the crowd remains fixated on inflation, their growth over-optimism should lead to a Minsky Moment over the medium term.

Powell’s Mistake

While we warned throughout 2021 that inflation would not be transitory, Powell and the crowd were happy to follow that narrative. Now, they remain inflation hawks, which should only worsen the outlook for assets like oil and the PMs.

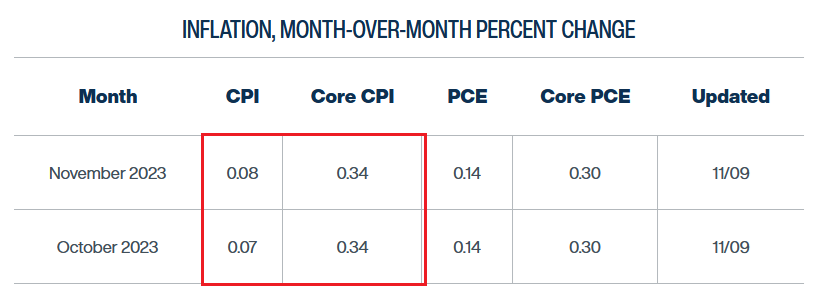

The Cleveland Fed has the headline Consumer Price Index (CPI) coming in roughly flat month-over-month (MoM) in October and November, which means little to no inflation. And while the core CPI is expected to hit 0.34% MoM, which is still too high, it should weaken alongside the U.S. labor market.

Please see below:

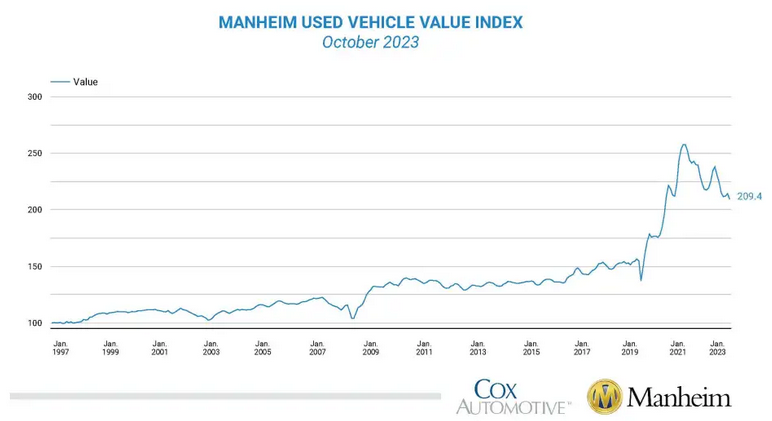

Similarly, while surging used car prices were all the rage in 2021, the tide has turned.

Please see below:

To explain, the Manheim Used Vehicle Value Index (MUVVI) decreased by 2.3% MoM, “a reversal of the gains that were seen during the prior two months.” As a result, a downtrend is firmly in place, and higher long-term interest rates should only intensify the slide in the months ahead.

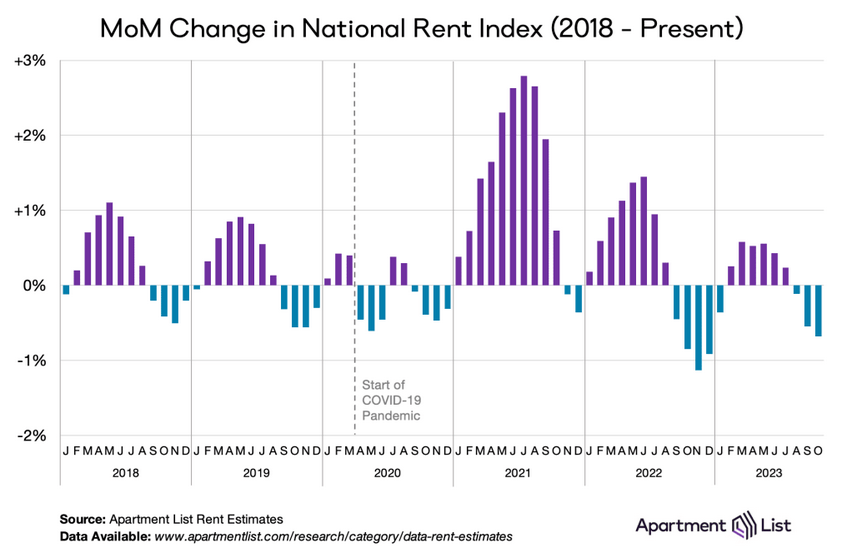

Likewise, it’s important to note that the Shelter CPI accounts for more than 30% of the headline CPI’s movement. And with Apartment List noting that the median rent dropped by 0.7% MoM in October, it’s “the third consecutive month of negative rent growth, and declines are likely to persist in the coming months as we head into the winter.”

The report added:

“This is the second steepest October rent decline that we’ve seen in the history of our index (going back to 2017). The only time that October brought a sharper decline was last year, when rents fell by 0.8 percent as the market shifted into the period of sluggishness that still persists. For comparison, from 2017 to 2020, October declines ranged from -0.4 to -0.6 percent.”

Please see below:

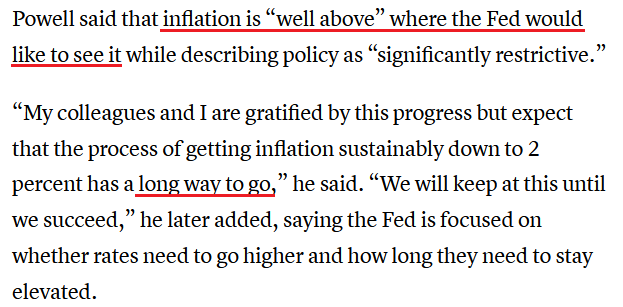

To explain, the weakness on the right side of the chart highlights how rent inflation is nothing like 2021. Yet, with Powell remaining hawkish on Nov. 9, his disposition should lead to more economic carnage, which is bullish for the USD Index. He said:

“The Federal Open Market Committee is committed to achieving a stance of monetary policy that is sufficiently restrictive to bring inflation down to 2% over time; we are not confident that we have achieved such a stance.”

Thus, when Powell realizes the severity of the economic weakness, it will likely be too late to stop financial assets’ sell-offs.

Overall, we believe Powell is making another policy mistake. He misread inflation in 2021, and now he’s misreading growth. And with assets like mining stocks, oil, and the S&P 500 poised to suffer the consequences, Treasury bonds and the U.S. dollar should be the best-performing assets if (when) volatility erupts.

To learn how to succeed in the interim, subscribe to our premium Gold Trading Alert. We closed out our 11th- straight profitable trade recently, and our 12th is currently in the green. Moreover, the technicals allow us to trade around our fundamental thesis, as plenty of opportunities have arisen from analyzing price levels and taking positions with great risk-reward propositions. Therefore, as we await a recession in 2024, we see plenty of long and short trades coming our way.

*********

share

share

share

share

share

Alex Demolitor hails from Canada, and is a cross-asset strategist who has extensive macroeconomic experience. He has completed the Chartered Financial Analyst (CFA) program and specializes in predicting the fundamental events that will impact assets in the stock, commodity, bond, and FX markets. His analyses are published at GoldPriceForecast.com.

Alex Demolitor hails from Canada, and is a cross-asset strategist who has extensive macroeconomic experience. He has completed the Chartered Financial Analyst (CFA) program and specializes in predicting the fundamental events that will impact assets in the stock, commodity, bond, and FX markets. His analyses are published at GoldPriceForecast.com.