Gold Price – Crossing The Rubicon

Gold is challenging the $1300 level for the third time this year. If it breaks upwards out of this consolidation phase convincingly, it could be an important event, signalling a dollar that will continue to weaken.

The factors driving the dollar lower are several and disparate. The US economy is sluggish relative to the rest of the world, the rise of Asia from which America is excluded is unstoppable, geopolitics are shifting away from US global dominance, and the end is in sight for monopolistic payment for oil in US dollars.

These subjects have been covered in some detail in my recent articles, which will be referred to for further clarification where appropriate. This article summarises these trends, and explains why the consequence appear certain to drive gold, priced in dollars, much higher.

The importance of gold and reasons for its suppression

The post-war Bretton Woods Agreement confirmed the US dollar to be fixed to gold at $35 per ounce. All other national currencies were linked to gold through the dollar at the central bank level. Ordinary civilians, businesses and commercial banks were not permitted to exchange their currencies for gold through central banks, so this was simply a high-level arrangement designed to maintain control of gold priced in dollars.

A few years after Bretton Woods, in 1949 and when the newly-fledged IMF began to collate statistics on national gold reserves, the US Treasury was recorded owning 21,828.25 tonnes of gold, 74.5% of all central bank reserves, and 43.6% of estimated above-ground gold stocks. However, over the years the proportions changed, and by 1960, US gold reserves had declined to 15,821.9 tonnes, 47% of central bank reserves, and 24.9% of above ground stocks.

Clearly, American control of gold had weakened considerably in the two decades following Bretton Woods. This weakening continued until the failure of the London gold pool, the arrangement dating from 1961 whereby the major American and European central banks collaborated to defend the $35 peg. The Americans had abused the gold discipline by financing foreign ventures, notably the Korean and Vietnam wars, not out of taxation, but by printing dollars for export, and it began to put pressure on the dollar. The London gold pool effectively spread the cost of maintaining the dollar peg among the Europeans. Unsurprisingly, France withdrew from the gold pool in June 1967, and the pool collapsed. By the end of that year, the US Treasury was down to 10,721.6 tonnes, 30% of total central bank gold reserves, and 15% of above-ground stocks.

Inevitably the decline continued, and by the time of the Nixon shock (August 1971 – the abandonment of the gold exchange commitment) it was clear the US Government had lost control of the market. She had only 9,069.7 tonnes left, representing 28.3% of central bank gold, and 11.9% of above ground stocks. Monetary policy switched from the fixed parity arrangements centred on gold through the medium of the dollar, to a propaganda effort aimed at removing gold from the monetary system altogether, replacing it with an unbacked dollar as the international reserve standard.

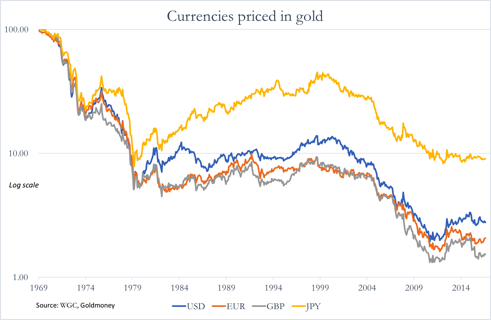

The result was the purchasing power of the dollar and the other major currencies measured in gold has all but collapsed, as shown in the chart below.

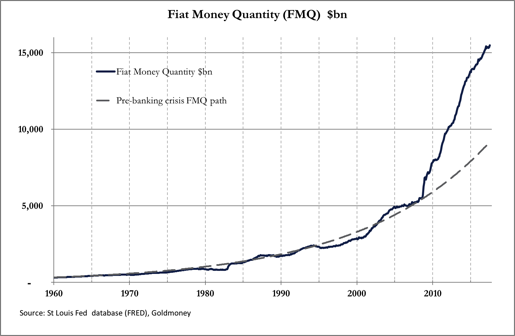

Between 1969 and today, the dollar’s purchasing power relative to gold declined by 97.3% (the blue line). By banning gold from having any monetary role, the US removed price stability from the dollar. More recently, since the great financial crisis the quantity of fiat money in the global currency system has expanded dramatically relative to the long-term average growth rate of money and bank credit. This is illustrated in our second chart, which records the growth in the total amount of fiat dollars in the US banking system.

The fiat money quantity is the sum of true money supply and commercial bank reserves held at the central bank (the Fed). It is the measure of all deposits, including those of the commercial banks. Monetary inflation has expanded dramatically since the great financial crisis, illustrated by its acceleration above the long-term trend. The consequences for the dollar’s purchasing power in time will be to accelerate the dollar’s decline even more.

The monetary expansion of the dollar has been echoed in the other major currencies, with negative consequences for global price inflation in the coming years. Meanwhile, gold’s inflation, at roughly 3,200 tonnes annually, is about 1.9% of above-ground stocks. The different rates of increase between above-ground gold stocks and the fiat money quantities of unbacked state-issued currencies is what ultimately drives the price of gold measured in those unbacked currencies. It is easy to see why a higher gold price, reaffirming gold’s role as sound money at a time of excessive fiat currency inflation, is viewed by the major monetary authorities as a potential threat to their currencies’ credibility.

There can be little doubt that without the propaganda war against gold led by the US monetary authorities, without the expansion of unbacked paper gold constituting artificial gold supply in the futures and forwards markets, and without the secret interventions of the US’s Exchange Stabilisation Fund, the gold price would be considerably higher, expressed in dollars.

However, gold remains centre-stage as a global hedge against the decline in purchasing power of fiat currencies. Besides rescuing the financial system from collapse nine years ago, the expansion of bank credit is inherently cyclical. The credit-cycle for China’s yuan appears to be moving into a new expansionary phase, reflected in a rising trend for nominal GDP. This will be put into context later in this article, but it is noticeable that on the back of China’s GDP growth, Japan, the EU and the UK are also enjoying export-led revivals.

The US does not share these benefits, partly because China and Russia, the founders of the Shanghai Cooperation Organisation (SCO), are deliberately freezing America and her money out, and partly because of America’s own tendency towards trade isolationism. It is therefore less certain that America is close to moving from the recovery stage of the dollar’s credit cycle into expansion. In the absence of other factors, the difference in interest rate outlooks this implies should be reflected in a declining dollar exchange rate against the other major currencies, a trend that has been under way since last January.

Despite the massive expansion of fiat money over the last nine years, it is possible for governments to stabilise the future purchasing power for their currencies. It will require their fiat currencies to be tied convincingly to the characteristics of gold. It depends on the government concerned accepting that gold is superior money to its own currency, owning sufficient physical gold reserves to convince the markets, and the gold price being at a level where the arrangement sticks. There is no doubt that China, Russia, as well as the other SCO member states and their populations regard gold as a superior money to fiat currencies, partly because their fiat currencies do not have well-established records of objective exchange value.

In the US, Japan, the UK and through much of Europe, the populations have experienced a longer, generally more stable objective exchange value for their currencies. Under pressure from their governments to use only state-issued currency, they have lost the habit of regarding gold as money. The monetary authorities of these countries, with a few exceptions, also do not regard gold as having any monetary role at all, beyond paying lip-service to a vague concept it has value as an asset which is no one else’s liability.

Therefore, understanding the role of gold and the protection it can offer fiat currencies is split into two geographic camps: the governments of Asia which are actively accumulating, or would like to accumulate additional reserves of monetary gold, and the governments of North America and Western Europe which see the gold price as irrelevant from the monetary point of view.

Gold reserves and gold secrets

We shall now briefly comment on the positions of the main monetary authorities on the global gold stage, their current gold policies, and how they are likely to change. These are the US, China, and the member nations of the SCO.

United States

The US monetary authorities were behind the push to remove gold from the monetary system, when they terminated the Bretton Woods Agreement in 1971. They are somewhat schizophrenic on the issue, the US Treasury claiming it still owns 8,133 tonnes of gold, reflected in the Fed’s balance sheet at the last official price of $42.22 per ounce. Interestingly, when the previous Fed Chairman, Ben Bernanke, was questioned on the subject by Senator Ron Paul in 2011, it was clear he did not regard it as money, only a legacy asset. If this is true, the Fed should substitute the reference to gold in its balance sheet with an unsecured loan to the US Treasury, which if Ben Bernanke is right, has a greater monetary credential than gold. It would also end the embarrassing calls to audit the Fed.

The resistance to leaving go of gold rather proves that gold is still money. However, the monetary policies of the Fed since the great financial crisis are predicated in the belief that gold is not money. This dichotomy is also shared with the Bank of England, the Bank of Japan, and the European Central Bank.

They all say that the world has moved on from the days when gold was part of the monetary system, so they are ill-prepared to discard the Keynesian beliefs upon which their current monetary policy is based. Their advanced, welfare-state economies are simply too far down the road of the state theory of money to turn back. However, this exposes their currencies, and particularly the US dollar as the world’s reserve currency, to a substantial loss of purchasing power as the rapid monetary expansion of the last nine years works its way through to consumer prices.

The election of President Trump promising to make America great again is turning out to be a failure. The removal only last week of Steve Bannon, his chief strategist, clears the way for the pre-Trump establishment to reassert itself. Gone is Bannon’s talk of a financial war against China and Russia, and doubtless, with a trio of the Generals Kelly, Mattis and McMaster now in control of the White House, it will be back to military options.

General Kelly, who was appointed to bring some order into the White House is doing this by removing dissenters from the mainstream. This was why Bannon had to go, and why President Trump himself will have to knuckle under and become as anodyne as President Obama. The mainstream is back and little has changed.

Meanwhile, the US economy muddles along without clear signs of improving consumer demand. It seems increased trade tariffs against China remain on the agenda, in which case they will amount to a self-harming tax on American consumers. Furthermore, global economic growth and progress is being driven primarily by China, from which America is excluded. And as the interest rate differentials start to widen between a stagnating US economy and an expanding Asia that also benefits Japan, the EU and the UK, the dollar is likely to weaken considerably in the foreign exchanges, as well as in terms of the commodities a dollar will buy.

Some forecasters believe that the US economy is stalling and deflation beckons. This is a mistake. The conditions replicate an inflationary outlook, whereby prices start rising at an accelerating rate, driven by a falling purchasing power for the dollar. The dollar is likely to lose more purchasing power through the effects of the last nine years’ monetary expansion working through to consumer prices. Additionally, foreign nations and commodity suppliers doing business in Asia are likely to be sellers of dollars for other currencies as the world moves towards an Asia-centric global economy. For deflation to take hold, there must be a shortage of dollars, not the substantial excesses in existence today.

China

In partnership with Russia, China is ringmaster for all Asia. The Chinese economy is run with a beneficial mercantilist approach. The primary political objective is to plan an economic future for the benefit of its people. Instead of democratic responsibility, the leadership commands the economy strategically in the universal interest of its citizens, crushing all individual dissent.

The Chinese state, having embraced important concepts of free markets, operates rather like the East India Company of old. Through a series of five-year plans, hundreds of millions of workers are being moved from less productive employment, redirected and retrained to more productive, higher technology and service occupations. The whole economy is in a planned transition. Low-skill jobs are being mechanised. Already, China is expanding into the rest of Asia, promising to move whole communities and countries out of relative poverty. The trans-shipment of goods across the Eurasian continent is expanding rapidly. The Chinese have also taken economic control over much of sub-Saharan Africa to secure the natural resources for the Grand Plan.

Most of this expansion is financed through bank credit, issued through the large state-owned banks. Unlike economic policy in the West’s welfare states, which is aimed at preserving legacy businesses, the positive redeployment of capital resources limits the build-up of malinvestments in China. Furthermore, the expansion of nominal GDP, which is the direct consequence of the expansion of bank credit, is accompanied by genuine economic progress, which is decreasingly the case in the West.

Consequently, China’s credit bubble is arguably less dangerous than those in the US, EU, UK, and even in Japan. However, credit bubble there is, and it is part of a global credit cycle that afflicts all fiat currencies. Undoubtedly, the Chinese authorities are aware of this danger, evidenced by their repeated actions to contain credit-fuelled speculation before it gets out of hand. [Crypto-currency enthusiasts, beware!]

So far, China has pursued a policy of managing the yuan’s exchange rate against the US dollar, and consequently records $3.08tr in foreign reserves, the vast bulk of it in dollars. At some point, China will need to abandon foreign exchange support of the dollar, because the dollar’s purchasing power measured in commodities is likely to continue its decline. This policy is making the raw materials China needs more expensive priced in yuan.

It is therefore becoming more sensible for China to dispose of her dollars and encourage the yuan to rise against it on the foreign exchanges. Admittedly, this will damage the profits of exporters to dollar-denominated markets, but should have the beneficial effect of redirecting capital and labour resources from these legacy businesses towards the new activities favoured by the five-year plan. Now that the process of refocusing the economy from manufacturing and exporting cheap goods towards a technology and service driven economy is well underway, China must be getting closer to ditching the dollar as the yuan’s reference currency. It is near the time for China to stop supporting the one currency she wants to do away with.

All the indications from China’s gold policy are that the end-plan is to tie the yuan to gold. In 1983, China introduced regulations appointing the Peoples Bank with the role of acquiring gold on behalf of the state. Analysis of contemporary prices, Western central bank sales and leasing into a prolonged bear market, shows China could accumulate significant quantities of gold bullion. In the 1980s, China had capital inflows she wished to neutralise, followed by the trade surpluses that began to accumulate in the 1990s. Adding to her programme of acquisition of gold from abroad, China beefed up her gold mining capacity and her gold refining state monopoly. Today, she is the largest mine producer by far, and takes in gold doré from other countries to refine and keep.

By 2002, she had accumulated enough bullion by then permit her own citizens to buy gold, and even advertised on television and other media to encourage them to do so. Deliveries into private ownership through the Shanghai Gold Exchange (controlled by the Peoples Bank) has totalled over 15,000 tonnes after 2002, though some of that will have been recycled as scrap. I have speculated that by 2002, the Chinese state could easily have accumulated over 20,000 tonnes before the Shanghai Gold Exchange was established, rather than the paltry figure of 1,843 tonnes in declared reserves today. Whatever the true figure, the Peoples Bank has purposefully been acquiring gold for thirty-four years, and by 2002 had built a strong and satisfactory position, clearing the way over the last fifteen years for her people to do the same.

China now has an iron grip on the physical gold market. The launch of the Hong Kong owned LME’s new gold contract is the latest move, building on China’s policy of using the Hong Kong and London connection for the development of her interests in international capital markets. The contract has been a success from day one. While the American banks push the price round on the Comex futures market, the real control over the market is now in Chinese hands.

China and her citizens are still accumulating gold. Basically, gold that goes into China does not come out. This contrasts with the US and the EU, where people are strongly discouraged from regarding gold as money or a store of value. For geopolitical purposes, it matters not who is right, but who has the power to be right. By ending the yuan’s exchange relationship with the dollar and transferring it to gold, global monetary hegemony would be transferred from America to China and her sphere of influence in one big step.

The Shanghai Cooperation Organisation

The SCO is driven by China in partnership with Russia. As well as a population of 3.3bn, it is the principal trade partner of Japan, the Koreas, and all the South-east Asian nations, adding a further 830 million people into the SCO’s sphere of influence. Dependents on the SCO for their exports of raw materials takes in nearly all sub-Saharan Africa, adding another billion. Europe, Australia and New Zealand are also drawn into the SCO’s circle of trade influence, a further 700 million. That totals over 5.8bn, leaving nations with a population total of about a billion either neutral or siding with America. Yet, it is the US dollar that settles the bulk of world trade.

There are strong indications that gold will be part of the settlement medium for the SCO’s future trade. Not only is China driving the SCO in partnership with Russia, which appears to be gold-friendly as well, but central bank demand for physical gold has mostly been from SCO member states and affiliates.

India, which lacks enough gold at the state level to support her membership, is using increasingly desperate measures to acquire gold from her own citizens. India’s economic renaissance, since the socialist Ghandi dynasty was ousted, has been on the back of Keynesian policies, so there is likely to be a strong intellectual resistance to gold in the monetary elite. Furthermore, senior appointees to the Reserve Bank have traditionally been on the advice of the Bank of England, which is anti-gold, and at the same time conscious that Indian gold demand on top of that of China is undermining control over the London bullion market. India’s gold policy as a member of the SCO is somewhat confused,

The imbalances between gold ownership of the various SCO member states rule out a new super-currency, so it is likely to be the yuan that is predominantly used for Eurasian trade settlement, with other members pursuing a currency board approach for their own currencies.

Control Over The Oil Market

The most significant post-war financial agreement achieved by America was with Saudi Arabia, whereby the Saudis agreed to only accept dollars in payment for oil in return for American protection. The agreement was adopted by all OPEC members, in return for the ability to fix oil prices as they pleased. This put the American banks firmly in control of the expansion of global credit, as well as the recycling of the currency surpluses arising from sales of oil to oil consuming nations, particularly benefiting the friends of America. That one decision, negotiated by Nixon and Kissinger, set up the dollar as the world’s reserve and trade currency after the end of the Bretton Woods’ agreement, and remains so to this day.

Today, Saudi Arabia is no longer the stable theocracy it was, and at current oil prices is running into financial difficulties. It plans to sell a five per cent stake in the national oil monopoly, Aramco, to raise $200bn to plug the gap in state finances. It can only do this by way of a public listing and offering if it can verify its stated oil reserves, which may prove difficult. If one was to guess an outcome for this dilemma, it would be that Saudi’s largest customer, China, could come to the rescue. And it would be expected that China would gain some influence over the disposition of Saudi’s oil sales.

It would be a typical Chinese strategy, repeating in the case of energy what China has already achieved in gaining control over the global economy. Other than America, whose consumption exceeds its supply by a significant margin, Russia is the largest global supplier (just), followed by Saudi Arabia. Between them they account for 22.4% of global supply. Other Asian suppliers in the SCO or allied to it gives a further 12%, making 34.4%. Coordinating these supplies gives China and her partners more production leverage on the global oil market than Saudi Arabia had in the 1970s.

Already, China is showing a preference to settling trade and energy deals in yuan, but to take this much further, it will need to offer gold convertibility to compete with the dollar. This appears to be being pursued in two steps, the first being oil suppliers given the opportunity to sell their oil for yuan, and to sell their yuan on the Shanghai futures exchange for gold, before the second step, a formal yuan convertibility, is eventually offered.

The yuan-gold contract already exists, the oil-yuan contract will shortly be introduced. The Shanghai International Energy Exchange is currently training potential users and carrying out systems tests prior to launch later this year. Obviously, these futures contracts in gold and oil may need to be initially supported by the state banks to enable them to build liquidity. But importantly, it will allow Iran, Russia and other Asian producers to avoid Western banking sanctions by selling oil for gold.

Geopolitics Could Set The Timing

The course of economic and monetary events in Asia was predetermined by the Chinese some time ago. We saw evidence of this in the UK, when China decided its international financial markets would be operated between Hong Kong and London, cutting out New York entirely and the dollar as much as possible. The Hong Kong Exchange bought the London Metal Exchange in 2012, and a year later London’s role was cemented when the then Chancellor of the Exchequer, George Osborne, visited China. This was followed by Britain becoming the first developed nation to join the Chinese-led Asia Infrastructure Investment Bank, much to the annoyance of the US.

The Obama administration had no effective response to China’s strategy, and continued to attack China’s partner, Russia, through proxy wars in Ukraine and Syria. The bid to take control of resource-rich Afghanistan failed. The election of President Trump brought with it uncertainly in US foreign policy, prompting a visit by President Xi to President Trump last April. There was no doubt that Xi decided he needed to assess Trump personally. He is likely to have come away with the view that Trump was unpredictable, and so it has proved.

We can only guess as to whether Xi’s visit has caused the Chinese to accelerate their planned move away from the dollar to their ultimate trade settlement and monetary plans. The threat of an American invasion of North Korea will be watched closely by Beijing in this context. The prospect of American troops on the Chinese border only 500 miles from Beijing will be prevented at all costs, so retaliation by an attack on the dollar would be the most effective response.

The removal of Steve Bannon last week and the control of the White House passing to three generals are important developments. In his last interview while still officially appointed, Bannon correctly analysed the geopolitics between China and the US. His analysis was very much on the lines presented in this article. However, his assessment was that the US needed to fight a trade and financial war against China, and forget anything military. In his words, “unless someone solves the part of the equation that shows me that 10 million people in Seoul don’t die in the first 30 minutes from conventional weapons, I don’t know what you are talking about, there’s no military solution here, they got us.”

Bannon’s mistake is to assume America still wields its traditional financial power, when it is clear to informed outsiders that this is no longer true. However, the generals now in charge of the White House are more likely to stoke up proxy wars, either because that is where their skills lie, or more cynically perhaps they are influenced by the arms manufacturers who are looking for defence contracts. They have taken no time in ratcheting up the American presence in Afghanistan and clearly have a desire to gain influence in Pakistan, both of which are on China’s eastern flank, where she is building commercial and infrastructural ties.

So, geopolitics are back on familiar ground. Trump is now neutralised and will increasingly look like a cowed Obama. Perhaps more troops will be sent to Syria. Perhaps more advisors will be sent to Ukraine. Perhaps more missiles will be installed in Poland, or the Baltic states. North Korea will rumble on, in a stalemate protected by its nuclear weapons. But increasingly, China’s interests are now served by taking the next step to disentangling herself from the dollar, and that will mean selling down her dollar reserves to stockpile the copper and the other industrial materials she needs. It will also mean lending dollars to trade counterparties, such as Saudi Arabia, to be repaid in yuan.

Conclusion

China and Russia’s geopolitical strategy has been evolving long enough for observers to understand it and the implications for the West. We can assume the strategic thinkers and intelligence agencies of all the major players have a reasonable grasp of the implications, including America, which is determined not to lose in this Great Game. That was the point behind Steve Bannon’s candid interview with Politico.

Bannon was deluded about the extent of America’s economic and financial power. He is now out. We are back to geopolitics being decided by the military. Meanwhile, China’s interests have almost certainly moved firmly towards dumping the dollar. This can only be done successfully by linking the yuan to the characteristics of physical gold, the market which China has effectively cornered.

If gold crosses the $1300 Rubicon, it may be taken as an early sign that China’s long-term plan of monetising her gold is progressing towards the next stage. The oil-for-yuan futures contract is due to be launched very shortly, allowing countries like Iran to buy gold freely, paid for by oil sales.

Alternatively, if China defers securing the yuan to gold, the dollar still looks like weakening against other currencies, reflecting a US economy isolated from the positive Asian story. The pace of the rise in the gold price might be slower, but the direction seems equally certain.

Eventually, gold will need to rise to a level where the Chinese are prepared to set a conversion rate. Expect China to use its control over physical gold markets to achieve it at a time of its own choosing. Leaving the $1300 price behind could well be the start of the move towards this objective.

Alasdair Macleod

HEAD OF RESEARCH• GOLDMONEY

MOBILE: +44 7790 419403

9. Bond Street, ST HELIER, JERSEY, JE2 3NP, CHANNEL ISLANDS