Gold Should Heed Miners’ Warning

While geopolitical conflict has kept gold afloat, mining stocks’ weakness signals trouble ahead.

Economic Recession Looms

While risk assets attempt to break free of their bearish corrections, gold’s relative outperformance has the yellow metal shining bright. Despite that, we’ve booked 11-straight profitable trades, and our 12th (currently open) remains in the green. As a result, our success highlights why mining stocks are often better trading instruments than the yellow metal.

Furthermore, while gold has largely sidestepped the recent risk rout, a recession is bearish for nearly all assets, and gold should suffer mightily if (when) the economic pain unfolds.

For example, S&P Global released its U.S. Composite PMI on Oct. 25. And while the headline results were decent and it outperformed expectations, weakness was present beneath the surface. An excerpt read:

“Although some service providers highlighted a pick-up in customer numbers, many continued to note that high interest rates and challenging economic conditions weighed on client demand. Some mentioned smaller and less frequent orders being placed by customers. As such, service sector new business fell for a third month running.”

In addition:

“The rate of charge inflation eased to the weakest since June 2020 and was slower than the long-run series average. Firms were reportedly keen to pass through any cost savings made to customers in a bid to drive sales.”

Thus, while 2021 and 2022 (to a lesser extent) were filled with demand-driven inflation, those days are long gone. With firms increasing discounts to move inventory, consumer demand has suffered, and the weakness should continue in the months ahead.

More importantly, the “rate of employment growth was only marginal overall,” as firms remain concerned about costs and future demand conditions. Therefore, the economic backdrop is heading in the wrong direction, and silver could be a major casualty if the trend continues.

Please see below:

Car Trouble

With the crowd ignoring the ominous implications of rising long-term interest rates, the consensus assumes a recession is highly unlikely. For context, we wrote on Sep. 29:

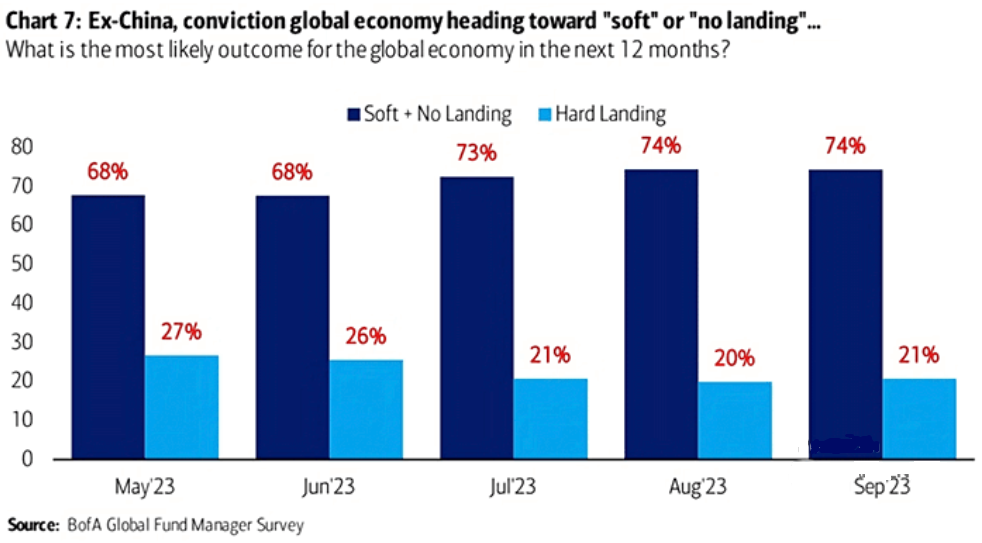

To explain, Bank of America’s latest Global Fund Manager Survey shows that only 21% of respondents expect a “hard landing” (the light blue bar) for developed markets over the next 12 months. Conversely, the majority expect a “soft” or “no landing” scenario to occur, which is a fairytale, in our opinion.

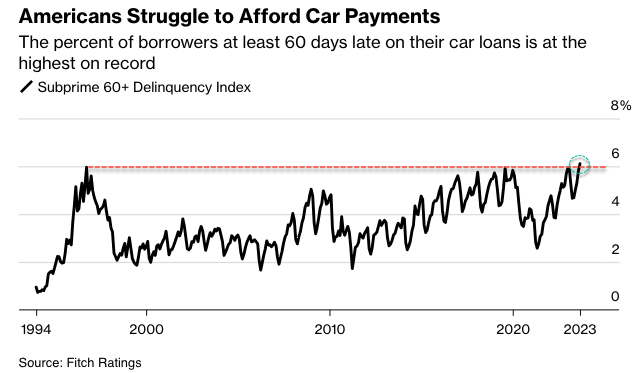

To that point, with auto-loan delinquencies hitting an all-time high, the problems should only intensify the longer rates remain elevated, and this is bad news for oil and the PMs. Bloomberg noted:

“The percent of subprime auto borrowers at least 60 days past due on their loans rose to 6.11% in September, the highest in data going back to 1994, according to Fitch Ratings.”

Please see below:

To explain, the black line above tracks the delinquency rate for subprime auto loans. If you analyze the right side of the chart, you can see that higher long-term interest rates are impacting the real economy.

Remember, the average auto loan length is 72 months, which means that financing rates are highly sensitive to the movements of the U.S. 5-year and 7-year Treasury yields. And with both rising substantially over the last few months, the scars should continue to show.

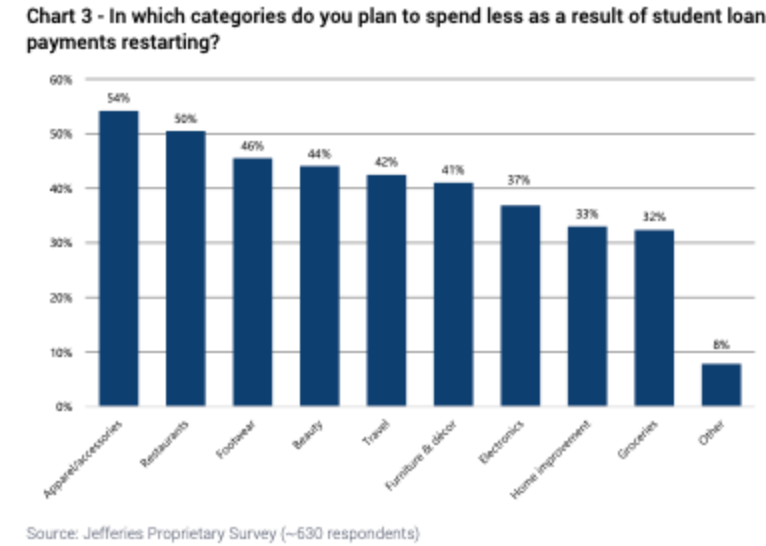

As another ominous sign, we warned the resumption of student loan repayments would further suppress consumers’ wallets. And with this occurring alongside higher borrowing costs and lower wage inflation, Americans have less disposable income.

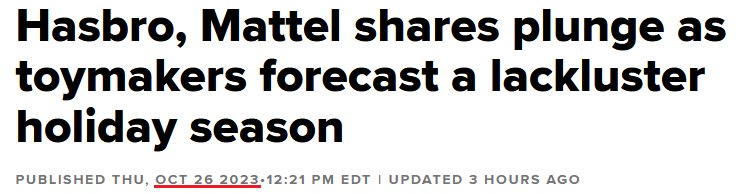

So, with U.S. toymakers sounding the alarm on Oct. 26, shares of Hasbro and Mattel sunk as consumers shunned holiday spending.

Please see below:

Moreover, we warned that darker days were on the horizon, and heightened volatility is bullish for the USD Index. We added on Sep. 29:

With less money to allocate to discretionary items, the current backdrop is much different than 2021/2022, in our opinion.

Please see below:

To explain, Jefferies surveyed student loan borrowers and found that roughly 40% to 50% plan to cut their spending on things like electronics, travel and apparel. As such, a confluence of factors has collided, making the economic outlook extremely unfriendly, and a Minsky Moment should help push the USD Index to new highs.

Overall, the S&P 500 has suffered, and the rout has not helped the GDXJ ETF. And with both assets declining alongside lower interest rates on Oct. 26, the results highlight how economic uncertainty often leads to liquidations across several risk assets. In contrast, Treasury bonds and the USD Index are the primary safe havens. Consequently, more of the same should occur before the miners’ bear market ends.

For a deeper understanding of our investment thesis, subscribe to our premium Gold Trading Alert. We closed out our 11th- straight profitable trade recently, and our 12th made money again on Oct. 26. Furthermore, the technicals are essential for managing risk, as the fundamentals are not the best timing tools. As a result, becoming a premium member equips you with everything you need to succeed.

********

Alex Demolitor hails from Canada, and is a cross-asset strategist who has extensive macroeconomic experience. He has completed the Chartered Financial Analyst (CFA) program and specializes in predicting the fundamental events that will impact assets in the stock, commodity, bond, and FX markets. His analyses are published at GoldPriceForecast.com.

Alex Demolitor hails from Canada, and is a cross-asset strategist who has extensive macroeconomic experience. He has completed the Chartered Financial Analyst (CFA) program and specializes in predicting the fundamental events that will impact assets in the stock, commodity, bond, and FX markets. His analyses are published at GoldPriceForecast.com.

More from Gold-Eagle