H1, 2025: Stock Market Top Projected

share

share

share

share

share

share

share

share

share

share

2025 begins with our plans well in motion for a stock market top and important changes to the macro.

This article attempts to put clearer words and images to the many words I expended in my interview with Jordan on Monday discussing the macro (and the precious metals).

For virtually all of 2024 NFTRH has been on a plan that saw two things in the stock market…

- Bullish and

- High risk due multiple indications of a coming top

Risk indicators have generally been of two kinds; signs of extreme complacency and confidence, and analogs of past conditions that extrapolate to a bearish outcome. Frankly, it has been a bit of a trick remaining bullish with the market’s trends and ongoing momentum, while being aware of the risk profile. But that is our job at NFTRH; to be on the right side of the markets, bias be damned. The right side in 2024 was the bullish side.

Let’s take a look at some indications in support of the bearish thesis for 2025, possibly in the coming weeks.

Confidence Game

Contrarian alarm bells are ringing in the form of intact mass-speculation and structurally over-bullish sentiment, which was supported by the Biden administration’s strong efforts to keep the economy goosed through debt spending on favored economic areas. Also, you’d have to believe that Treasury Secretary and former Fed chief Yellen at least has the ear of the Fed, which went dovish at a key pre-election moment. The fact that government itself was primary in 2024 hiring is unprecedented in my experience. Here is the proof from November Payrolls report. The confidence game currently in play was largely supported and sustained by the admin’s stimulative policies.

Now, speaking of confidence, comes the “America great again” portion of our show. The businessman president knows economics (thinks the public). He is going to cut taxes. He is going to lay out tariffs and make ’em pay in order to have access to US citizens as customers. Well, the seeds of a down economic cycle have already been planted and when Trump starts funding tax cuts from increasing the $35T debt pile it will be too late. Damage done.

Let’s look at a few pictures associated with the thoughts above, starting with Michael Pollaro’s picture of what had been rising liquidity into 2024, emanating out of the Fed’s various orifices, but which has turned back down…

Michael Pollaro

…back in line with the Fed’s balance sheet, which has been shrinking since 2022:

St. Louis Fed

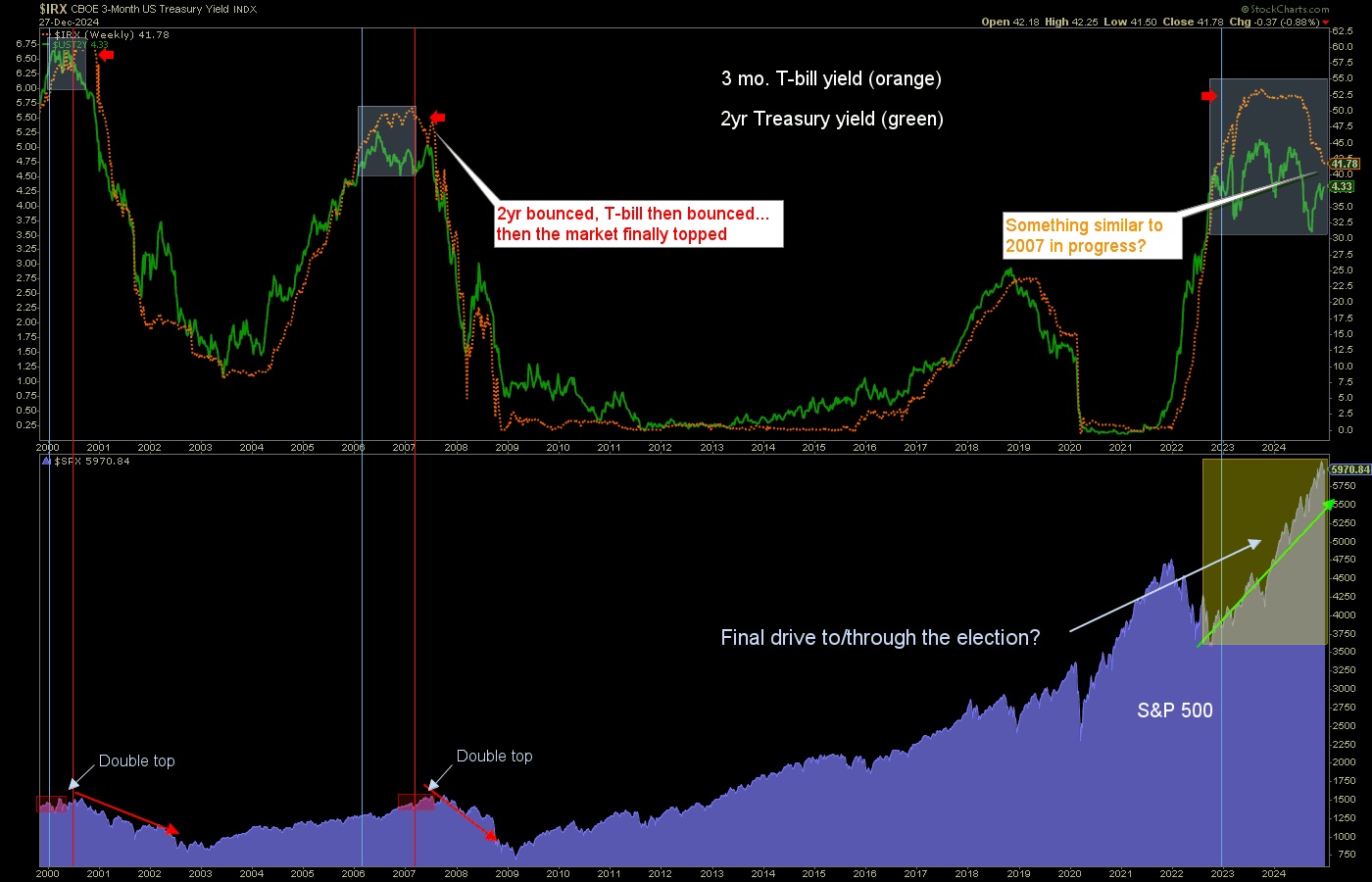

The Fed is a clear and present indicator of waning market liquidity, and recently the bond market has pressured it to start to ease away from dovish Fed Funds rate policy as well. This is likely due to the market’s reaction to the Tariff-minded and debt-spending Trump. Regardless of the rationale, it is a clear and present risk signal for markets, much like we noted in NFTRH 842:

With respect to inflation, I think the bond market is reacting to what it thinks it sees ahead in the new administration. But when the economy starts to show more signs of weakness (not yet pervasively evident, thanks IMO to the efforts to hold onto the White House by the Biden administration through economic stimulus and some fudged payrolls reporting), the bond market may well change its mind.

Right now the bond market is doing to the Fed what it did in 2007; forcing it to stop and reevaluate its dovish stance. Of course, that was the precursor to a “hard down” in yields, inflation, economy and stock market back in ’07.

Another danger is the duo of the US dollar and the Gold/Silver ratio (GSR); the 2 Horsemen of the Liquidity Apocalypse.

Liquidity Destroyers, USD & GSR

When gold out-performs silver, especially if both metals are declining in price and the US dollar is rising, the indication is anti-liquidity for the markets. Gold is a refuge (likely after USD and short-term Treasuries) during market liquidity crises and silver is not. USD, to the denial of “de-dollarization” dreamers, is still the world’s reserve currency and thus, logical anti-market to asset markets.

This can, for a while, support a Goldilocks theme as inflation signals get pushed down, but if the two riders become impulsive to the upside, you should have an abundance of caution. As yet they are bull-biased and bullish respectively. But with GSR in a pattern and USD just breaking out of a base, there is little that is impulsive about this to this point. But the charts are bull-biased and as such, caution should be taken against the possibility that the bias could play out in an impulse.

Bottom Line

Fed-manufactured liquidity is waning and the 2 Horsemen, GSR & USD are picking up on that. With the recent bump back up in market-based inflation signaling, the Fed is under pressure to back away from its purely dovish stance (as we heard from its own orifice on the most recent FOMC day). That potentially sets a trap for the Fed and the markets if the result of 2007 analog in the 2yr/T-bill (ref. the black & blue chart above) is extrapolated to today.

Contrarian Signals

“I think it’s pretty clear we’ve avoided a recession”

In the link we show why this assertion from Jerome Powell is another cherry on top of the 2025 contrarian bear thesis. In the article, we illustrate why not only the 10yr-2yr Yield Curve but also now the 10yr-3mo Yield Curve are flashing danger. Optimists had been saying that the economic cycle was not in danger because the 10yr-3mo was not confirming the 10yr-2yr’s steepener. Well, now it is. An economic bust comes with a curve steepener.

Not only is the very fact that America just elected the pro-business, tax cutting, tariff imposing Trump to the White House a contrarian’s dream, now we also have the head of the Federal Reserve uttering the words quoted above. Well, let’s include another contrarian gem; the assertion by media that now that the Yield Curve is un-inverted economic recession has been averted! Happy New Year! Happy days are here again!

Ah, no. In response to a mainstream media that was incorrectly scaring the public about a recession back in 2022-2023 because the curve was inverted, we noted that was so very wrong, and we also noted that the new calls of “ALL CLEAR!” were wrong… and dangerous to a gullible public back in September:

“Bond Market Yield Curve Returns to Normal”? Signals for Gold, Stocks, Economy

While indicators like the above have been warning of bad things to come for today’s wildly over-bullish herds…

Bloomberg

Bloomberg…the sentiment picture has been over-bullish all year, subject to brief spikes in anxiety that served to refuel the market, as late stage bulls will often do.

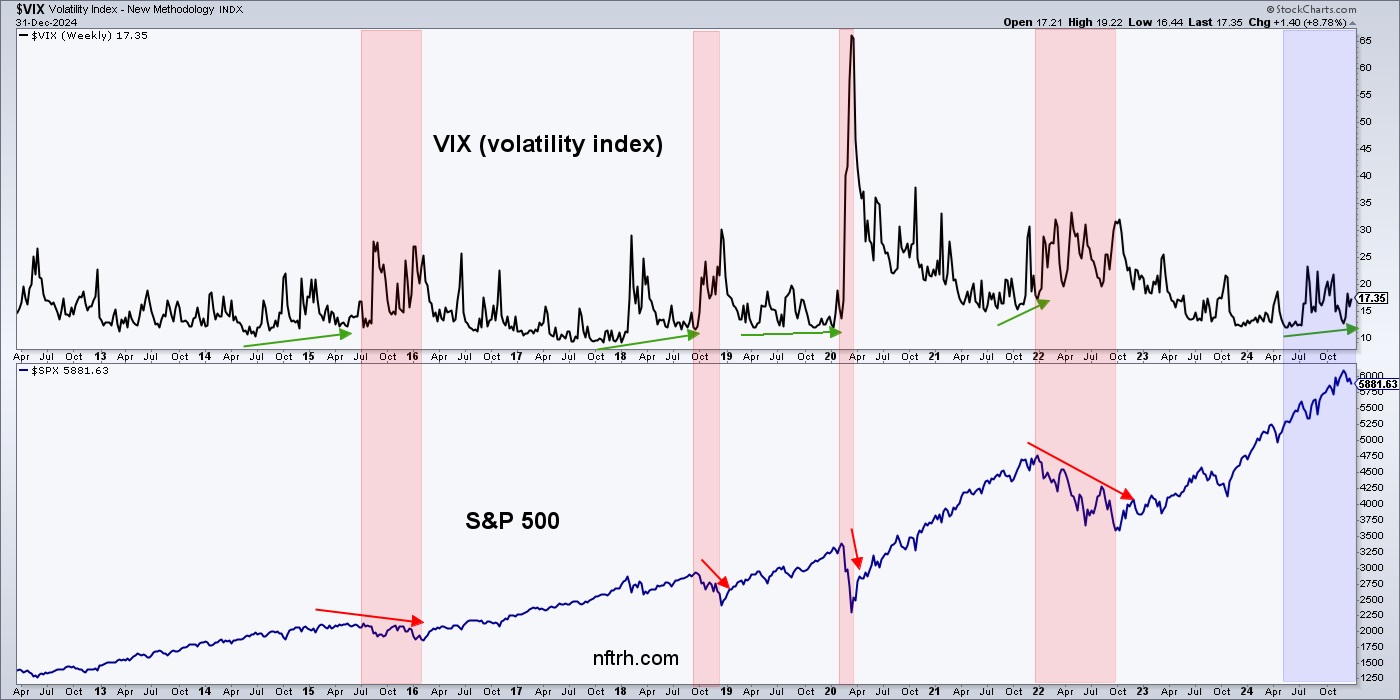

The VIX is an indicator of market volatility that has been asleep for most of the year, waking up, spiking and getting pushed back down by the ongoing bull momentum. However, we have for much of the year been tracking this negative divergence for stocks. With the VIX higher now than when the S&P 500 was at a significantly lower level, a divergence is in play that has, with much grind and patience, proven bearish for stocks in the past.

Finally, with a note that there are plenty of other indicators in play that theoretically present a bearish view, we’ll end with another sound asleep risk indication, High Yield spreads, which show a completely intact speculative environment when at a depressed level, as they are today. The spread has started to inch upward from its extreme but is far from conclusive. This and the VIX tend to be more immediate risk indicators, and they too helped keep us on the bull theme all year as they slept soundly, but aware of the high risk a contrarian would see in that sleepiness.

St. Louis Fed

Bottom Line

We used nominal market TA and the still asleep risk indicators like the VIX and HY Spreads to maintain a bullish stance in 2024. But we used the Yield Curve steepeners, the 2yr/T-bill yield divergence and the USD/GSR combo as imminent risk indications. NFTRH was not bearish in 2024 and hence, is credible (not talking a perma-bearish book) in its assertions that 2025 is at clear and increasing risk. Credibility is important, you know?

I would sign off with a “Happy New Year!”, but instead I’ll sign off with an “Interesting New Year!” because it’s not going to be happy for everyone.

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed market updates and NFTRH+ dynamic updates and chart/trade setup ideas. You can easily subscribe by Credit Card or PayPal (see all info and options). Keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar, or take it to another (intermediate) level with our free eLetter. Follow via Twitter@NFTRHgt.

********

share

share

share

share

share