The Narratives Driving Gold

Is the hype real, or is it a mirage?

With silver and mining stocks declining sharply on May 11, the PMs' volatility was on full display. And while base effects provide the trio with inflation cover through June, the second half of 2023 should elicit more economic anxiety.

For example, New York Fed President John Williams upped the hawkish ante on May 9. He said:

“In my forecast I see a need to keep a restrictive stance of policy in place for quite some time to make sure we really bring inflation down from 4% all the way to 2%. I do not see in my baseline forecast any reason to cut interest rates this year.”

So, while the PMs have benefitted from rate-cut prophecies, QE dreams, bank contagion fears, and the prospect of a depressed U.S. dollar, these narratives contrast the realities that should unfold in the months ahead.

Williams added:

Thus, while the crowd assumes that zero-interest-rate (ZIRP) policy is next, we warned throughout 2021, 2022, and recently that those bets are increasingly premature.

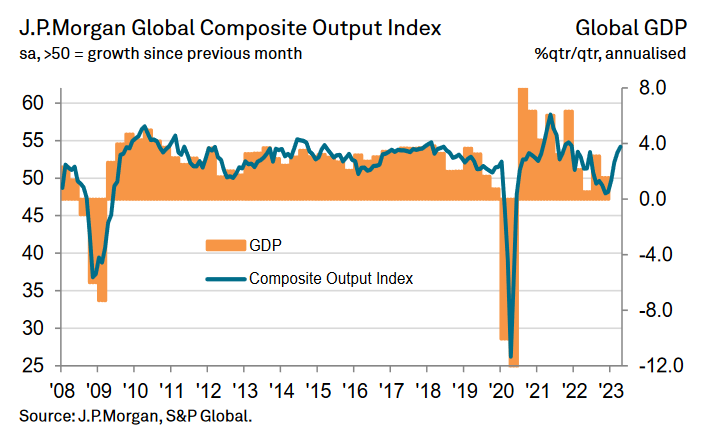

As evidence, S&P Global and J.P. Morgan released their Global Composite PMI on May 5. The headline index increased from 53.4 in March to 54.4 in April, reaching a 16-month high. The report stated:

“The start of the second quarter saw a further acceleration in the rate of global economic expansion. Growth of output and new orders hit their highest levels since December 2021 and March 2022, respectively, as job creation and business optimism also strengthened….

“All of the 14 nations for which April composite PMI data were available registered an expansion of combined manufacturing and service sector output, the first time concurrent growth has been recorded since June 2022.”

Please see below:

To explain, the blue line above tracks the Global Composite PMI, while the orange bars above track annualized global GDP growth. If you analyze the relationship, you can see that the former often leads the latter.

More importantly, the right side of the chart shows how the blue line’s ascent signals resilient GDP growth in the months ahead. As such, a PMI of ~54 is nothing like 2008 or 2020, and this is why talk of lower interest rates is much more semblance than substance.

A History Lesson

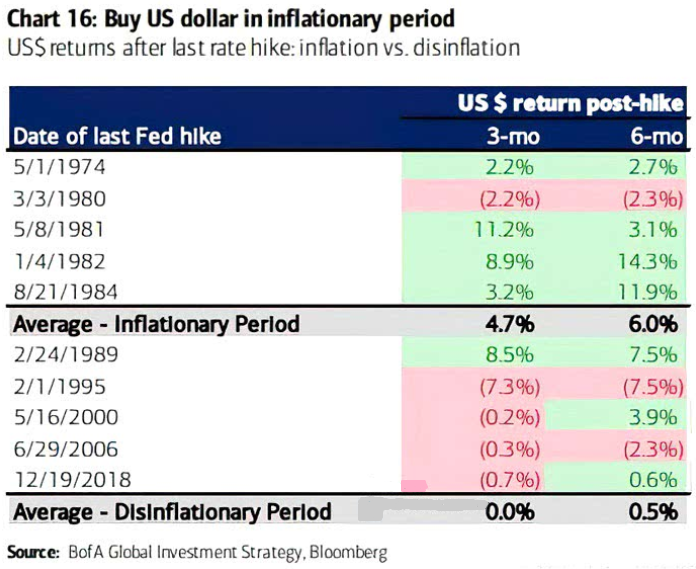

While the crowd assumes a dying U.S. dollar will help revive gold, it’s another narrative that contrasts history.

Please see below:

To explain, Bank of America compiled a performance table for the USD Index three and six months after the Fed’s final rate hike. If you analyze the top half, you can see that during four of the five inflationary periods, the dollar basket strengthened over the next three and six months.

Now, we don’t believe the Fed has completed its rate-hike cycle, but the data highlights how a pause is not bearish for the USD Index. Therefore, while realities of sticky inflation and resilient demand should surprise the crowd over the medium term, even the pause bulls are fighting history.

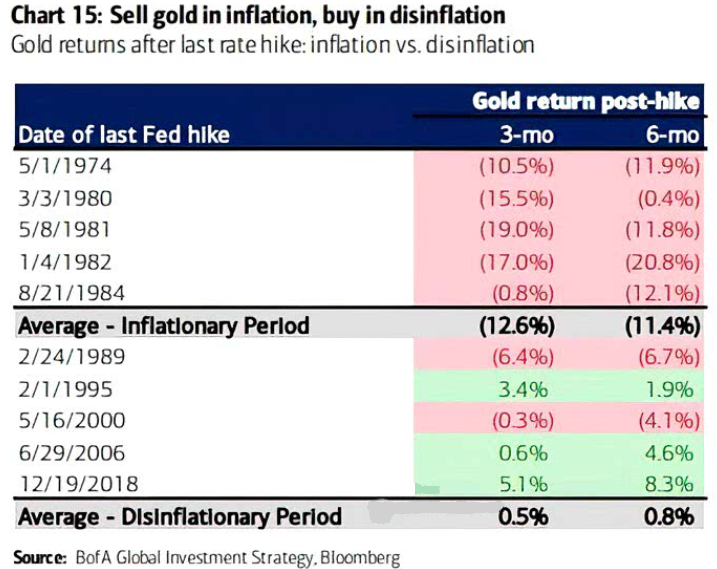

To that point, Bank of America compiled a similar performance table for gold.

Please see below:

To explain, the figures at the top half show how after the Fed’s last rate hike during the inflationary periods of the 1970s/1980s, gold weakened over the following three and six months.

Again, we believe the Fed’s rate-hike cycle has more room to run. However, even if 5.25% is the peak, the medium-term outlook for the USD Index is bullish, while the medium-term outlook for gold is bearish.

Pushing Expectations Further

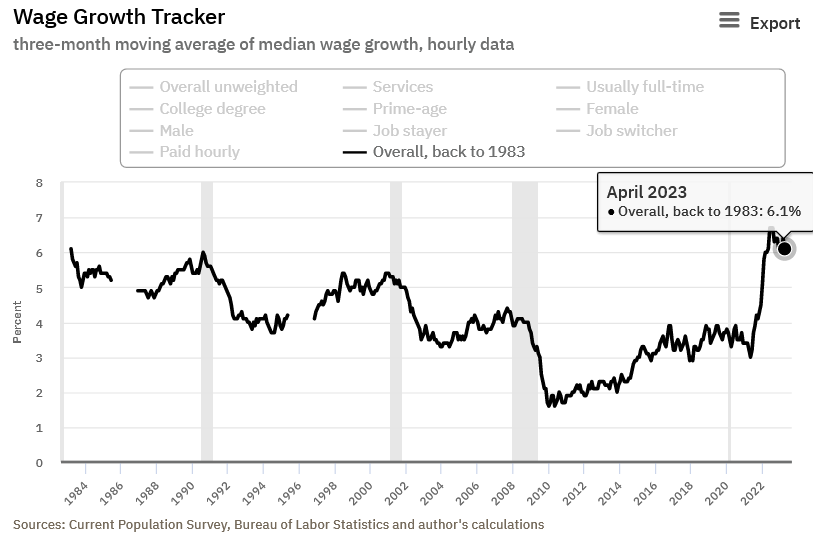

Finally, while the Atlanta Fed’s Wage Growth Tracker dipped in April, it’s only 0.6% below the record high set in 2022. Moreover, if we exclude the post-pandemic period, 6.1% would be an all-time high dating back to 1983.

Please see below:

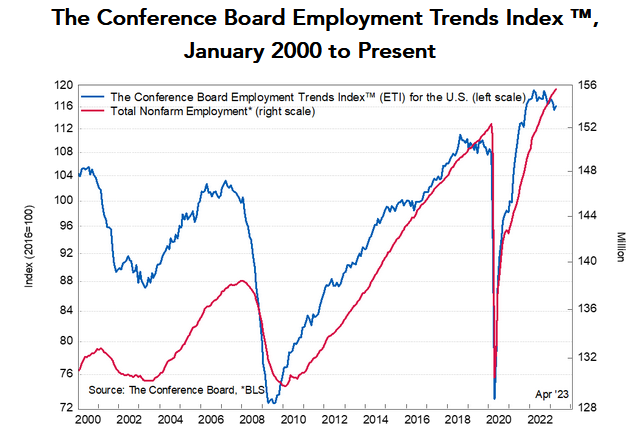

Likewise, The Conference Board released its Employment Trends Index (ETI) on May 8. The metric increased from 115.51 in March (a downward revision) to 116.18 in April. Frank Steemers, Senior Economist at The Conference Board, said:

“The labor market remains resilient and tighter than before the pandemic, complicating the Federal Reserve’s efforts to slow inflation. This may prompt the Fed to raise interest rates by an additional 25 basis points to decelerate job growth and wage gains.”

Thus, while Steemers expects “a short and mild recession starting in 2023,” he conceded that “it may take until later in the year to see a substantial weakening in job growth or monthly job losses.”

Consequently, while the recession bulls continue to forecast doom, non-compliant data keeps pushing those expectations further into the future. And this was the story throughout late 2021 and 2022.

Please see below:

Like the Atlanta Fed’s Wage Growth Tracker, the ETI has come down from its recent peak. However, the progress has been relatively mild, highlighting why interest rates are too low to create lasting disinflation.

Overall, short-term sentiment helped gold, silver, and mining stocks, as bullish narratives distracted the crowd from the fundamental realities. But, the data-driven analysis does not support these consensus conclusions, and we believe the PMs are vastly mispriced. As a result, more meltdowns like the one on May 11 should unfold in the months ahead.

Should you sell gold after the Fed’s last rate hike, or is this time different?

********

Alex Demolitor hails from Canada, and is a cross-asset strategist who has extensive macroeconomic experience. He has completed the Chartered Financial Analyst (CFA) program and specializes in predicting the fundamental events that will impact assets in the stock, commodity, bond, and FX markets. His analyses are published at GoldPriceForecast.com.

Alex Demolitor hails from Canada, and is a cross-asset strategist who has extensive macroeconomic experience. He has completed the Chartered Financial Analyst (CFA) program and specializes in predicting the fundamental events that will impact assets in the stock, commodity, bond, and FX markets. His analyses are published at GoldPriceForecast.com.

More from Gold-Eagle