The Next Crisis Is The Mother Of All Counter-Party Risks (Part 2)

In Part I I explained the counter-party risk that is all around us - and will come to the fore in the next financial crisis. In this second part I reflect on the rescue operations of the Fed following the 2008/2009 recession and the following QEs and ZIRP policies that have led to diminishing returns and that will ultimately weaken the US dollar: the biggest counter-party risk of all counter-party risks.

Addendum 8 - CDS, Credit Default Swaps. Ultimately it should be considered that when we encounter these systemic events that it will impact the underlying currency. For example when the pension underfunding gets so problematic that the Government has to print more money to meet and rescue the obligations the counter-party risk will be reflected in the devaluation of the currency or the loss of purchasing power, the goods that you can buy with the same amount of nominal money will tumble.

We saw one of the most poignant examples of counter-party risk in 2008 when AIG that had given off numerous CDS (Credit Default Swaps) to banks because it never expected the markets to tank the way they did (typical Wall Street view, things can only go up, that is what the Japanese thought till 1989!!). So issuing CDS or Collateralized Debt Obligations (CDOs) was a “no-brainer” for AIG. Anyway a breakdown of the system will happen again but this time it will be 10x worse than in 2008 and then the system can’t be saved because all the tools in the toolbox will have been exhausted and therefore won’t carry the weight, credibility or effectiveness they had “solving” the 2008 crisis. It will mean we will go deeper and longer (5 years!?).

According to the underlying contracts AIG’s credit default swaps did not call for collateral to be paid in full in case of just “market changes”. In most cases, the agreement said that the collateral was owed only if market changes exceeded a certain value or if AIG’s credit rating fell below a certain level. AIG was accruing unpaid debts—collateral it owed its credit default swap partners, but did not have to hand over due to the agreements’ collateral provisions (misleading clauses drafted by lawyers?).

But when AIG’s credit rating was lowered, those collateral provisions abruptly kicked in—and AIG suddenly owed its counterparties a great deal of money. On September 15, 2008, the day all three major agencies (what a coincidence!) downgraded AIG to a credit rating below AA-, calls for collateral on its credit default swaps rose to $32 billion and its shortfall hit $12.4 billion—a huge change from $8.6 billion in collateral calls and $4.5 billion in shortfall just three days earlier.

AIG had written credit default swaps on over $500 billion in assets. But it was the $78 billion in credit default swaps on multi-sector collateralized debt obligations—a security backed by debt payments from residential and commercial mortgages, home equity loans, and more—that proved most troublesome. AIG’s problems were exacerbated by the fact that these were one-way bets. AIG didn’t have any offsetting positions that would make money if its swaps in this sector lost money, basically AIG in all its wisdom never thought that the CDSs would be called in. Why? Because the blatant naivety of investors that the markets couldn’t possible tank the way they did though this time it will be 10x worse and still the majority of people don’t believe it will happen, they haven’t learnt their lesson. It is sometimes a real mystery to me how people on Wall Street make money. It must be the tunnel vision that really helps! It definitely isn’t the all-encompassing universal knowledge that here is at play. They have this theory and unbridled “confidence” that markets and government only benefit when the markets go up and thus the government will do everything they can to sustain this Shangri-La though as we have seen with Japan in 1989 at one stage reality kicks in and Shangri–La is no longer. And the more its valuations are out of whack with the median the stronger the reaction (it is pure physics: action is reaction) and on top of that everything is so intertwined that Japan, China, BRICS and the EC, that all have similar issues, will exacerbate the problems.

AIG, a global company with about $1 trillion in assets prior to the crisis, lost $99.2bn in 2008. On September 16 of that year, the Federal Reserve Bank of New York stepped in with an $85 billion loan to keep the failing company from going under and also the parties that had bought CDS from AIG. I should emphasize that when counter-party risk arises there are no winners and a lot of value is destroyed.

Goldman Sachs has always insisted that it wouldn't have lost a nickel if AIG had failed in 2008. The investment bank claims that it was fully insured against the risk that the financial giant could collapse under the weight of its credit derivative-related losses. That story is complete BS or fake to use an applicable term. New documents turned up in a congressional probe that show conclusively that Goldman had in fact, purchased insurance against the possibility that AIG might go bankrupt -- from financially troubled firms that were in no position to make good on their obligations. Voila counter-party risk. That is like winning the battle and losing the war. Hence why Paulson, the ex Goldmans CEO and Treasurer Secretary at that time, had to save AIG!!

For instance, one company that would've had to make a $175m payment to Goldman if taxpayers hadn't saved AIG is Lehman Brothers. Citigroup, itself the recipient of a government bailout, owed Goldman $402 million if AIG failed. Indeed, the list of companies that had sold credit default insurance to Goldman on AIG, including numerous foreign players, is riddled with firms that had been severely damaged by the financial crisis. See how you think you have protection against possible events and how it turns out to be not the case.

Goldman had entered into agreements to spread the risk with 32 entities. Overall, after the feds showed unusual largess by paying 100 cents on the dollar to save AIG Goldman Sachs received a $12.9 billion payout including $8.1 billion linked to credit default swaps from the government's bailout of AIG. Goldman Sachs also revealed to the Senate Finance Committee that it would have received $2.3 billion if AIG had gone under. Other large financial institutions, such as Citibank, JPMorgan Chase and Morgan Stanley, sold Goldman Sachs protection in the case of AIG's collapse. Those institutions did not have to pay Goldman Sachs after the government stepped in with tax money. Goldman exploited its and AIG's status as companies that were "too big to fail" to make the U.S. government an offer it couldn't refuse. Then New York Federal Reserve Bank chief Tim Geithner, Paulson and other government regulators who brokered the deal with Goldman quickly caved, either in panic over the disintegrating financial system or deference to Wall Street (probably both). It is amazing how these bankers and especially Goldman Sachs get away with blackmail and lying and exploiting the system to their own advantage and to the detriment of the taxpayers. “Doing God’s work” to cheat people, pathetic! What a joker that Blankfein.

Banks create their own systemic risk for obvious reasons: their survival! And avoid as much tax as they can.

Anyway what is important in my point of view is to understand how banks create their own systemic risk, intentionally or not intentionally, using their fractional banking (leverage), and how these banks abuse the concept of systemic risk to their own advantage: bailout at any costs at the expense of the taxpayers whilst they can continue their corruptive practices against all costs. We all know the story “if you owe the bank $1m you have a problem whilst if you owe the bank $500m the bank has a problem”. The banks operate on the basis of this adagio and they most likely invented it. The banks paid Hillary Clinton $250,000+ per speech in order to ensure her backing in terms of taxpayers (not The Clinton Foundation money!!) money when needed when she would become president, which she didn’t as we know. By the way see what happened to the contribution from Norway and Australia to the Clinton foundation! Do you need any more proof about the “pay for play” by the Clintons? Isn’t it funny these governments penalize kickbacks but they practice the art of kickbacks themselves.

The idea that is sold to the people why the banks need to be rescued with taxpayer’s money is that without a sound banking system the economy can’t function and the rescue of the banks therefore is in everybody’s interest. Another reason why this can be pulled off is that the common man in the street doesn’t have the faintest idea how all the financial machinations work hence why they don’t protest. Ignorance of the citizens, next to the principle of diffusion of responsibility, is bliss for the bankers in order to massively abuse the system, think Goldman Sachs and the Clintons (ever wondered why their son in law had such a big position in Greek securities!?) manipulating the balance sheet of Greece, for fees in excess of $700m!!, so that Greece would qualify for the EU. And guess who ended up with the bill to rescue Greece! The European taxpayers and the Greek! And then adding insult to injury the banks do everything they can “within the legal framework” to avoid paying taxes and deprive the taxpayers from their rightful revenue stream. So they want the bailouts but steal from the taxpayers in terms of tax avoidance schemes. See the Oxfam report http://fortune.com/2017/03/27/oxfam-europe-banks-tax-havens/. Focusing on the continent's 20 biggest banks, Oxfam found that these banks paid no tax on up to $416 million in profits registered in seven tax havens in 2015, with a total of $5.32 billion in profits registered in tiny Luxembourg (low tax regime)—more than the profits in the U.K., Germany and Sweden combined.

Hold them accountable contract or no contract and punish them where it hurts: THEIR money.

This is what happens if you don’t hold people responsible by sending them to prison and confiscate all their money and more, contract or no contract! These bankers know the “spiel” and thus behave in a way that they can get away with murder; there basically is no downside for them. Money and power corrupt. Just look at those losers of Merryl Lynch and Wells Fargo, Stanley O Neal and John Stumpf who blew up the bank and stole from deposit holders and they both walked away with hundreds of millions because of the contract they had. And don’t even start with me about $75m being clawed back. Am I missing something here? So you steal from people and you get rewarded! Why are instead these people not being sued for inflicting so much damage and value destruction of the companies they were “managing”? This is sick beyond my comprehension and undermines everything that justice stands for. It erodes the justice system because it basically says crime pays if you do it in “a sophisticated way” or in a way that nobody really understands or when too many people that are well connected operate the scheme (Dudley, Draghi, Carney, Gensler). This has kind of always been the rationale of the Goldmans strategy. Target governments on a national or local level, because it is easier to get away with enormous fees, next to that these unknowledgeable government official are often “esteemed” (for the wrong reasons, ask the Libyans) they are dealing with Goldman. And be the first to create products nobody really understands so that they can charge their suck up clients any commission and get away with murder. Or you use a couple of political (Clintons) and monetary heavyweights (Draghi) to get Greece in the EMU for a hefty sum. And then as a couple of pathetic losers they blackmail the monetary authorities that if they don’t get saved the system will fall over! Do you get the gist? You have to look at the concept, the wiring that is being followed here over and over again. There are no check and balances anymore. It pays to steal from the taxpayers.

Different money systems. Only precious metal backed systems give power to the people!

Anyway going back to the misperception that banks are too big to fail abusing the fractional banking system. This is where the different money systems come in. I believe there are three money systems:

- Fiat money –places the power in the hands of the banks. As a result of the fractional banking system their “leverage” (10x-25x) and thus potential damage to the economy is more than proportional. Fiat money is a currency that a government has declared to be legal tender. Legal tender means that “the designated, the legal money” is valid payment for all debts. Fiat money it is purely based on “creditability” (whereby the fundamentals of the monetary system ultimately prevail and not the government regulation that money is legal tender, see Zimbabwe or Venezuela). Fiat money is a currency established as money by government regulation or law. The term fiat derives from the Latin fiat ("let it become or be", "it will become") used in the sense of an order or decree. It differs from commodity money, money backed by the real value of gold or silver, as was the case in the olden days. The value of fiat money is derived from the relationship between supply and demand (scarcity aspect) rather than the value of the material that the money is made of, paper versus gold or silver. And because fiat money is not backed by real value ultimately fiat money always fails as is proven by history time and time again, see below.

- Digital money – digital money places the power firm in the hands of the Government because they can control and monitor everything when currency is digital and only consists of ones and zeros. Can you imagine the easiness with what you can create, and therefore also destroy, money, you just create ones and zeros though the devastating pitfall also is that it can be wiped out by a grit failure, virus or push on the button. Digital money means total surveillance, citizens will become even more a “derivative” of the Government, you just say yes and Amen! If the Government orders that you have save you save otherwise they will force you. Modern day slavery in the hands of a couple of political maniacs! And then there is the BS argument of Rogoff or Larry Summers who argue against cash money because of the “facilitation” of drug dealers, terrorists or black money though they should go back to school and first learn about the principle of cause and result. Take strict and harsh enough measures against these people and only the lunatics will dare to challenge the system. And apparently they, the no-cash supporters, have forgotten about the Bangladeshi Central Bank money that was stolen from their account in the NY Fed by Philippine/North Korean hackers. They, Rogoff and Summers, are clearly out of whack with reality and have never heard of or thought through the consequences of acts by hackers and from grid outages. In the latter case how would people get access to their money and what would happen to transactions? It is completely flawed, the vulnerability of the monetary system increases manifold. Last but not least it is known that some black money facilitates the oiling of the economy but these guys are so theoretical that they don’t understand how things would work out in reality. They are too much in their head then present in reality.

Bitcoin is an example of digital money, which in my point of view only has “value” because of the fixed number of bitcoins (supply/demand scarcity), its “portability or transferability” and the credibility by the people who believe in the concept of bitcoin. Though except for these reasons I believe bitcoin doesn’t have any value what so ever, it is a combination of ones and zeros, there is no inherent value except for its created scarcity!! At present it is being used by the Chinese to “export” their wealth out of China. Last but not least Bitcoin could be seen as a proxy for the sentiment towards gold, which as we know is suppressed to make the US dollar look better for obvious reasons.

- Gold money – money backed by precious metals puts the power firmly in the hands of the people where it belongs. Citizens give politicians the mandate to govern in a certain way but definitely not to take their right and freedom away as we see in Turkey with that dictator Erdogan or as we now witness with the unmasking and spying on US citizens. What we have seen too often is that people in the Government or Deep State (career “civil” servants and members of the military industrial complex, $600bn annual budget) believe that they know best and feel that they can impose rules and regulations on citizens to their own advantage but definitely not to the good and the welfare of the people. This is all orchestrated so that they can maintain their position in power and look after their financial interests. This is where the stand off between real money (gold and or silver backed) and fake money (paper money) comes in.

If you can’t print money at infinitum, like is the case with paper money, you can’t direct and influence things the way you want and for example “you can’t bribe people” if you understand what I am saying, everything is accounted for. You can’t create debt and make unrealistic promises because you can only spend what you have. I believe “paper money equals manipulation whilst gold and silver money equal discipline”. With gold and silver backing the currency there is no faking it, you either have the precious metals to back up your money or not. No nonsense! Next to that it should again be emphasized that paper money is solely dependent on the credibility of the economy and the credibility of the monetary authorities and therefore also representing counter-party risk because it is dependent on the performance of a third party. The counter-party risk is the devaluation of currency or said differently the loss of purchasing power, the number of goods that you can buy with the same nominal amount. The difference with gold or silver money is that they have inherent value that isn’t dependent on the state of the economy or the credibility of the monetary authorities or the performance of a third party. Gold and silver have value of their own; people are willing to pay for gold or silver n’importe quai! There are no promises that have to be fulfilled or policies to be followed for gold and silver to have value. Gold and silver are nobody’s obligation to deliver! And that is the big difference with fiat money, bitcoin or digital money, gold and silver have value of their own, no counter-party risk, value regardless of any third party obligation, with thousand years of validation and history. Only people that have no knowledge of history and don’t understand the spill function gold and silver play in the monetary system call gold “the barbaric relic”. As mentioned several times the only barbaric relic is debt not gold!

The Functions Of Money

Money provides four key functions for an economy:

- Medium of exchange, medium of exchange means that money is used to conduct transactions instead of having to for example schlep heavy silver. A piece paper is much easier to exchange than having to carry and exchange 100 ounces (or almost 3kg) of silver. The Chinese word for “Bank” is literally translated as “Silver House”.

- Unit of account, also termed measure of value, means that prices are stated in terms of money, measurement in the same unit being one dollar one values a bread at $5 whilst for example jeans are quantified at $100. Everything is measured, standardized in the same unit called dollars. It is kind of similar to measuring distance in meters and centimeters or yards and inches or measuring weight in grams and kilos. One carat diamonds for example wouldn’t suffice as an unit of account because they have different colors and impurities and thus different value. With barter trade whereby goods are exchanged you don’t have the same way of measurement. How many breads for one pair of jeans, how many breads for a plumber job or how many jeans for one car!!

- Store of value, Store of value means that value, to satisfy basics and desires, can be stored over time in the form of unallocated, unused money. Money represents unallocated purchasing power and thus value.

- Standard of deferred payment or credit. Standard of deferred payment means that future payments, such as paying off a car loan, are also in terms of the monetary unit, it is the yardstick for credit, which could be regarded as the “opposite” of cash money.

The primary function of money is to act as the medium of exchange. Money makes transactions easier because everyone is willing to trade money for goods and goods for money. To see why money makes transactions easier, consider a barter economy that has no money, where one good is traded directly for another. The key to successful barter trades is the double coincidence of wants, each trader has what the other wants and wants what the other has. A perfect match though this in general is very unlikely. And without double coincidence of wants, a barter economy can become exceedingly inefficient and thus hinders the growth of the economy. This problem doesn’t exist when there is one medium of exchange and measurement such as the dollar.

Difference between money and currency: Currency (paper, bitcoin, precious metals) is what brings money to life!

Key difference: Money is an intangible asset, it is a concept, which means it cannot be touched, it cannot be smelled; however it can be “seen” in terms of numbers, US dollars. Money does have a few properties such as it must be a medium of exchange; a unit of account; a store of value; and, occasionally in the past, a standard of deferred payment.

Currency is the tangible concept that is based on the intangible concept of money. Currency is the promissory note (paper) or coin (commodity), which is the tangible expression of money. “Currency is what brings money to life”. It is what is traded in return of goods or services. The term “currency” is derived from the Middle English word “curraunt”, meaning “in circulation”, current (hence why we also talk about velocity of money). These are the coins and bank notes that are in circulation. There was approximately $1.5 trillion in circulation as of February 22, 2017, of which $1.47 trillion was in Federal Reserve notes. Each country has its own currency, which can be traded against another currency against the existing currency exchange rate. Throughout history, various different things have been used as currency including silver, shells and even stores of grains. This describes that basically any medium that can be used to purchase another commodity, good or service as long as people accept as the currency of exchange.

Money (M(oney)2 was $13.3trn in January 2017) and currency ($1.5trn, February 2017) are often used interchangeably in today’s world because of their similar concepts. However, as described here above they are not exactly the same.

Why did they stop publishing the M3? To not report repurchase liabilities?

M1, M2 and M3 are different measures of money. The exact definitions of the three measures depend on the country. These three money supply measures, M1, M2 and M3, represent slightly different views of the money supply. The most restrictive, M1, also called narrow money, normally include coins and notes in circulation and other money equivalents that are easily convertible into cash, only measures the most liquid forms of money; it is limited to currency actually in the hands of the public. This includes travelers’ checks, demand deposits (checking accounts), and other deposits against which checks can be written. M2 includes all of M1, plus savings accounts, time deposits of under $100,000, and balances in retail money market mutual funds. But that is all small potatoes, M3 includes all of M2 (which includes M1) plus large-denomination ($100,000 or more) time deposits, balances in institutional money funds, repurchase liabilities issued by depository institutions, and Eurodollars held by U.S. residents at foreign branches of U.S. banks and at all banks in the United Kingdom and Canada.” In other words, M3 tracks what the large institutions are doing with their money. This includes US dollars held in banks in Canada and the UK (called Eurodollars). So the question immediately arises why would the FED stop tracking this? I believe it is because the M3 includes the repurchase liabilities issued by depository institutions! Why? Because they indicate the collateral that is been supplied to financial institutions, for the positions that are underwater or in trouble, to avoid systemic risks.

The average life expectancy for a fiat currency is 27 years so we are 19 years “overdue”

The history of Chinese currency spans more than 3000 years. Currency of some type has been used in China since the Neolithic age, which can be traced back to between 3000 and 4500 years ago. Cowry shells are believed to have been the earliest form of currency used in Central China, and were used during the Neolithic period.

According to a study of 775 fiat currencies by DollarDaze.org, there is no historical precedence for a fiat currency that has succeeded in holding its value, because it really doesn’t have any value! Twenty percent failed through hyperinflation, 21% were destroyed by war, 12% destroyed by independence, 24% were monetarily reformed, and 23% are still in circulation approaching one of the other outcomes. The average life expectancy for a fiat currency is 27 years, with the shortest life span being one month. Founded in 1694, the British pound Sterling is the oldest fiat currency in existence. At a ripe old age of 317 years it must be considered a highly successful fiat currency. However, success is relative. The British pound was defined as 12 ounces of silver, so it's worth less than 1/200 or 0.5% of its original value. In other words, the most successful long-standing currency in existence has lost 99.5% of its value. Given the undeniable track record of currencies, it is clear that on a long enough timeline the survival rate of all fiat currencies drops to zero. History has a message for us: No fiat currency has lasted forever. Eventually, they all fail and quite logically because they pay an interest and therefore they in fact work ultimately towards their own destruction through interest payments.

Every month still $200bn injected in the system whilst returns are diminishing. It is not working!

So the average life expectancy for a fiat currency is 27 years and basically every 30 to 40 years the reigning monetary system fails and has to be retooled. The last time around for the U.S. was in 1971, when Nixon cancelled the convertibility of dollars into gold. The world bought into the dollar no longer backed by gold as its reserve currency, the dollar was the currency of the most powerful country in the world. Reserve currency and economic and military power go hand in hand (just see how wars were financed in history). But here we are 40 years later and the dollar has been diluted through the QEs and other programs, following the 2000 and 2008 recessions, like it has gone out of fashion. The reduction in purchasing power correlated to inflation of course is something one in general doesn’t experience till it is too late because it happens gradually over time. That is different for hyperinflation when prices visibly change from month to month with 1%, 5%, 10%, 20% and even higher percentiles.

Anyway eight years after the crisis of 2008-09, central banks are still injecting almost $200 billion a month into the global financial system to keep it from imploding whilst returns are dimishing. In economics, diminishing returns is the decrease in the marginal (incremental) output of a production process as the amount of a single factor of production is incrementally increased, while the amounts of all other factors of production stay constant. Just stand still for a second and think about this. And ultimately the result will exactly be what they are trying to prevent: Armageddon.

The Liars In Chief

For a long time there has been no discipline whatsoever to ensure balanced budgets. In fact during Obama’s reign the US debt doubled from $10trn to $20trn, the largest debt increase in history whilst Main Street suffered. And see what happens with politicians looking after their own interest Obama just signed a $60m book deal! For what! For writing down all the lies he told us! We also shouldn’t forget of course Clinton’s lock-box plan, which was of course nothing more than a scheme to use more than $3 trillion in Social Security surpluses to “bring down” federal debt. In exchange, the Social Security trust fund gets another $3 trillion worth of IOUs. Clinton basically “stole” from several trust funds (Medicare and Social Security) pretending he created a budget surplus, which was of course purely cosmetics, robbing Peter to pay Paul. And then this scheme artist has the audacity to boast to audiences that he had a few budget surpluses under his reign. Same way he said that the Clinton Foundation was doing good work, whilst only 10% of all the donations going to the people it was raised for. What is happening to the remaining 90%? Back to another BS artist Obama, I find it so “funny” that this ignorant man had the nerve in April 2016 answering questions from London students boasting about his legacy that “he got unemployment down to 4.7%” and "saving the world from a Great Depression – that was quite good." See the following chart.

The guy was and is really delirious and clearly doesn’t have any understanding of economics (as shown by the chart here above) though has an excellent understanding of being mischievous. The reason I am so fierce towards these people, such as Clinton and Obama, is that they lie to the people that have chosen them, purely for their own good and to make their so-called legacy look good. Give me a brake they are the biggest con artists there are.

The real unemployment situation is much, much worse. ShadowStats shows more realistic figures with a U6 of 22.5%

Anyway back to the factors that show that the economy hasn’t gained any traction as a result of the stimulus measures. For March the U3 the official unemployment rate was reported at 4.5%. U5 includes discouraged workers and all other marginally attached workers and U6 adds on those workers who are part-time purely for economic reasons. The current official U6 unemployment rate as of February 2017 according to the BLS is 8.90%! Though according to ShadowStats by John Williams the figure is 22.5%! To give you some background on Walter J. "John" Williams, he was born in 1949. He received an A.B. in Economics, cum laude, from Dartmouth College in 1971, and was awarded a M.B.A. from Dartmouth's Amos Tuck School of Business Administration in 1972, where he was named an Edward Tuck Scholar. During his career as a consulting economist, John has worked with individuals as well as Fortune 500 companies. I would say that his biography is pretty good and that John probably knows what he writes about (unlike Obama does) unless you believe that Ivy League schools like Dartmouth are fake! The official unemployment figures, that clearly show a huge discrepancy with the real unemployment figures according to ShadowStats, and that show Obama’s “past achievements” couldn’t be further from the truth. It is now up to Trump to make these figures more realistic and call a spade a spade.

The ShadowStats Alternate Unemployment Rate for March 2017 is 22.5%.

Inflation Figures Have Been Underreported To Facilitate The QEs And ZIRP And To Control The Increases In Social Security Payments

Next to the real unemployment figures published by ShadowStats.com even Goldman Sachs Group Inc. has raised questions about the success of the efforts by the Federal Reserve and its peers to spark inflation and improving real income in the wider economy with a chart (see below) showing what’s happened with prices in the largest developed economies since the start of 2009. Clearly it is been much much more an asset gain than a gain for the consumers, hence why real incomes have kept on deteriorating. Assets have been inflated, real incomes have declined and the currency has been diluted (QEs) without barely any productivity against it. The chart below does illustrate how well financial markets recovered from the 2007 to 2009 meltdowns. By contrast, consumer price inflation, incomes and other such gauges of the “real” economy have put in muted performances. Though it is my believe that the inflation figures have been heavily manipulated in order to allow the QEs and ZIRPs and in order to prevent huge increases in social security payments that are inflation linked. The low reported inflation figures also explain partly why reel incomes haven’t risen in the last 15 years. For politicians, the chart essentially sums up the frustrations that have helped propel the populism that Brexiteers and Donald Trump rode to victory. People are fed up with the empty promises of the politicians and their lack of accountability and this is a trend we see everywhere in the West and Middle East. Change is in the air.

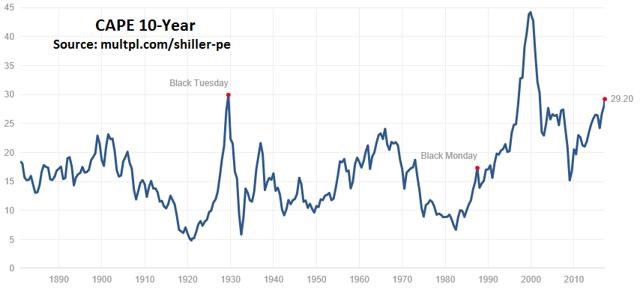

After so many years The QEs and ZIRP policies are clearly missing their goal of returning confidence to the markets with the intended add-on effect of restoring consumer spending. `The chart below shows that the Fed has just “blown up” assets with the cape Shiller PER now at almost 30x. According to Yale finance professor Robert Shiller, the S&P 500 SPX, now trades on a cyclically adjusted price-to-earnings (cape) ratio of 30x, compared to a historic fair value for this measure of about 16x.

The cape Shiller Index at 30x and the Q or Buffett ratio at 1.2x+ clearly show overvalued the markets are whilst the economy hasn’t picked up and GDP is even declining.

Since the 1870s, there have been a total of three periods in which the average stock P/E ratio was above 26.5x. The first time was around the Panic of 1893, the second was around the 2000 dot-com crash and the third was around the 2008 financial collapse. Need any more proof that these markets are overvalued? See here below.

And according to the Federal Reserve, the so-called “Q” factor, which compares stock-market values with the real-world prices of corporate assets, is way above the historic average though it’s not yet in crazy year-2000 territory. The Q factor has a solid track record. Here below is the “latest” Fred (St Louis Fed) Q chart showing the Q factor from 1975 until January 1, 2014. By the way I wonder why the Fred doesn’t have a more recent chart!!

The Q factor, a long-term valuation indicator, has become popular in recent years, thanks to Warren Buffett. Back in 2001 he remarked in a Fortune Magazine interview that "it is probably the best single measure of where valuations stand at any given moment." Right now, for example, the total size of the US stock market according to Federal Reserve data is $22.6 trillion. Meanwhile the total size of the US economy is $18.8 trillion. This puts the Buffett valuation at around 1.2x, meaning the stock market is about 20% pricier than the entire US economy.

Historically speaking everything in excess of 1.2x is expensive. Stock markets start getting into trouble when the ratio surpasses 1.0. (The Buffett ratio was 1.11 before the 2008 crash…). Assets have been inflated, real incomes have declined and the currency has been diluted without barely any productivity to account for, between $4-$10 in debt is needed to create $1 of GDP growth (diminishing returns). What we have witnessed is that all this money has been pumped in the markets and economy without real improvements in the economy except for the top 1%. The Atlanta GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2017 is 0.5% on April 14, down from 0.6% on April 7.

Again proof that the M2 has been endlessly increased without any significant productivity improvements or increased velocity of money to show for.

The dilution of the currency clearly shows in the real median household income that isn’t even at 1999 levels!

Anyway my point is to emphasize that currencies clearly represent counter party risk when the currency gets diluted or devalued too much as a result of too much debt, continuous budget deficits and unsound monetary and economic policies whilst no productivity improvements to show for. The dilution of the currency clearly shows in the reduction of real income the goods you can buy with the same amount of nominal income. And although the Fred chart here below only runs to January 1, 2015 (Updated: Sep 13, 2016) with a median real income of $56,516 we seem to be still below the real median income in 1999!!

We see also see the effect of the dilution of the currency read loss of productivity happening in China, where for example uninhabited cities were built just to keep its workforce employed, with as a result the enormous capital flight, out of fear of future difficult times, which triggers further weakening of the Renminbi. People often don’t see the reduction in purchasing power as counter-party risk though it is the most systemic counter-party risk in our societies. Hence why currencies are the ultimate benchmark of your (global) wealth.

In the end it is how your currency or purchasing power stacks up against other currencies on a global scale. Your currency is the proxy of how the rest of the world appreciates or values how your economy is being run and represents real wealth, expressed in the exchange rate. Ask people how they regard the currencies of Zimbabwe or Venezuela where they “weigh” paper money to do a trade! Paper has become paper again.

When the dollar loses its reserves status we will need another anchor for a new or temporary monetary system: gold, the mirror image of the reserve currency.

Fiat monetary systems have a limited lifetime as shown here above, on average 27 years, but when the currency finally loses its function in society we need another anchor that replaces or bridges the period till a new monetary system can be implemented and enough trust in the system is restored. For the time being it most likely will be not another fiat paper system because there will be no trust in the political and monetary establishment creating another phony fiat paper system. In general people go back to basics like something they can hold on to and that has value of it own and that is not dependent on the phony promises and lies of the politicians and monetary and economic conditions. And as we know through history gold and silver have proven to be the ultimate anchor in this respect. There is a reason why currencies in many languages refer to gold or silver just think of geld, argent or sterling.

Gold is the mirror image for the currencies and especially the reserve currency because that is the spill of the monetary system. Though ultimately the anchor of all monetary systems is gold. Anybody who states the opposite doesn’t have a clue about finances just look how much gold reserves the central banks have and are still accumulating. There must be a reason besides the uneducated “barbarous relic” argument. No!? Anyway gold and silver are in general only strong when the reserve currency is weak and visa versa. There is no reason for gold to be strong when the reserve currency is strong when investors have all the confidence in the monetary system. So there is no better way of comparing the real value of a currency against the ultimate yardstick in the financial system: gold. The comparison with the gold price shows us, as seen in the chart below, what happened to the purchasing power of the US dollar.

In 1933, through a series of gold-related acts, culminating in the Gold Reserve Act of 1934, America realized a dollar devaluation of 41% when it adjusted the price of gold from $20.67 per ounce of gold to $35 per ounce. America, like the others before, had its economy bottom and recover as a result. At least nine other major economies had enacted a devaluation of their currency by removing it from the gold standard, all of who emerged from depression. A similar devaluation of the US dollar against gold as happened in 1933 shouldn’t be excluded today. Anyway what is clear is that a debasing of the currencies against gold reduces the purchasing power of the underlying currency as demonstrated also by the chart here below.

In the 1920’s and 30’s the performance of Homestake Mining clearly expressed the strength and value of gold.

For the moment the authorities will do everything in their power, legal or illegal, to keep the reserve status for the US dollar and therefore expect volatility, uncertainty, and financial dislocations on the road to the reign of gold and silver. Though ultimately the fundamentals will win and they won’t be able to keep the weakness of the existing currencies at bay with the prices of gold and silver showing the way.

Conclusion: The Lender Of Last Resort Will Be Gold And Silver!

The AIG bailout is a lesson in how interdependency in financial markets stacks up like a house of cards. Of course it wasn't only Goldman that was made whole when the government came to AIG's aid -- it was all of the insurer's credit insurance counterparties. When taxpayers rescued AIG, they were at the same time absorbing losses Wall Street firms like Citi, Bank of America, JPMorgan Chase and Morgan Stanley would've suffered on the credit default contracts they'd sold to Goldman. Everything is intertwined as never before and therefore the extreme measures by the Fed, the ECB, the BOJ and the BIS, with injection in the system of around $200bn a month, are needed to keep the system going because of the alternative that basically is no alternative! And what do we see the BofA finds that surging consumer confidence does not result in higher spending hence why the retail sector is doing so badly. I think a lot people just don’t seem to accept that the consumer is maxed out. Just look at some statistics such as the U6 unemployment figure of 22.5% (ShadowStats), record 95m Americans not in labor force (number grew 18% since 2009), according to a recent Bankrate survey of 1,000 adults, 57% of Americans don’t have enough cash to cover a mere $500 unexpected expense. There is no way out and the only option is to keep things going till a miracle turns everything around or till the moment we will face the abyss. But when it gives we most likely will witness extreme moves in interest rates, the US dollar and gold and silver.

The situation is like a rubber band that you try to stretch more or a ball that you try to keep underwater till it snaps and then it really snaps. When something snaps and it really doesn’t matter what snaps, all imbalanced situations will break because they have been in such an imbalanced situation for such a long time. And when they all snap the Fed won’t be able to initially do something about it because when things snaps they are so uncontrolled that you first have to wait till they settle down before you can take measures against the situation. All the HFT programs will go haywire because as past volatile situations have shown their algorithms don’t function in extreme situations.

The credit risk we are facing with respect to the enormous debt in the US is clearly illustrated in the chart here below where the 35-year downtrend is threatened. The reversal of the 35-year downtrend will cause unimaginable losses in the global bond markets that will ultimately have their effect on the currencies that are the real proxy of a country’s credibility and wealth. There is no discrimination as to the size or perceived stability of a nation’s economy; if the leaders abuse their currency, the country will pay the price.

And as mentioned the real stone to fall will be the reserve currency, the US dollar, which will generate huge wealth destruction. I believe the only way to hedge that destruction will be to revert to the basics of monetary policy which means investing in, next to agricultural land, real money: gold and silver.

As we know JP Morgan said “gold is money everything else is credit”, all credit represents counter-party risk. And the dollar currency is nothing else than an obligation by the Fed to “guarantee” the value of the US dollar; it is the lender of last resort. Lender of last resort is defined as an institution, usually a country's central bank that offers loans to banks or other eligible institutions that are experiencing financial difficulty or are considered highly risky or near collapse which is of the crucial importance to avoid a breakdown of the financial system as we almost experienced in 2008. Though contrary to 2008 when the banks caused the breakdown in the markets this time it will be the central banks that will cause the collapse in the markets. Just look at the SNB (Swiss National Bank) that has large equity holdings. The only “lender of last resort” left will be gold and silver, physical gold and silver!

© Gijsbert Groenewegen April 14, 2017

[email protected]

More from Gold-Eagle