Russia Collusion Story: A Big “Nothing Burger” Or A Case For Gold?

Gold got a boost Friday on weaker-than-expected inflation and retail sales figures, casting doubt on the Federal Reserve’s ability to continue normalizing interest rates this year.

Consumer prices rose slightly in June at their slowest pace so far this year. The consumer price index (CPI), released on Friday, showed the cost of living in America rising only 1.6 percent compared to the same month last year, significantly down from the most recent high of 2.8 percent in February and below the Fed’s target of 2 percent. Much of the decline was due to energy prices, which fell 1.6 percent from May.

As I’ve explained elsewhere, CPI is an important economic indicator for gold investors to track. The yellow metal has historically responded positively when inflation rises—and especially when it pushes the yield on a government bond into negative territory. Why lock your money up in a 2-year or 5-year Treasury that’s guaranteed to give you a negative yield?

But right now the gold Fear Trade is being supported by what some are calling turmoil in the Trump administration. Last week the Russia collusion story took a new twist, with emails surfacing showing that Donald Trump Jr.; Jared Kushner, the president’s son-in-law and now-senior advisor; and former Trump campaign manager Paul Manafort all agreed to meet with a Russian lawyer last summer under the pretext that she had dirt on Hillary Clinton.

Whether or not this meeting is “collusion” is not for me to say, but the optics of it certainly look bad, and it threatens to undermine the president’s agenda even more. For the first time last week, an article of impeachment was formally introduced on the House floor that accuses Trump of obstructing justice. The article is unlikely to go very far in the Republican-controlled House, but it adds further uncertainty to Trump’s ability to achieve some of his goals, including tax reform and infrastructure spending. I’ll have more to say on this later.

A Contrarian View Of China

A new report from CLSA shows that Asian markets and Europe were the top performers during the first six months of the year. Korea took the top spot, surging more than 25 percent, followed closely by China.

Despite persistent negative “news” about China in the mainstream media, conditions in the world’s second-largest economy are improving. Consumption is up and household income remains strong. The number of high net worth individuals (HNWIs) in China—those with at least 10 million renminbi ($1.5 million) in investable income—rose to 1.6 million last year, about nine times the number only 10 years ago. It’s estimated we could see as many as 1.87 million Chinese HNWIs by the end of 2017.

According to CLSA, global trade is robust, with emerging markets, and particularly China, driving most of the acceleration this year. In the first three months of 2017, global trade grew 4 percent compared to the same period last year, its fastest pace since 2011.

“Indeed the early months of 2017 have seen China become easily the biggest single country driver of Asian trade growth,” writes Eric Fishwick, head of economic research at CLSA.

A lot of this growth can be attributed to Beijing’s monumental One Belt, One Road infrastructure project, which I’ve highlighted many times before. But according to Alexious Lee, CLSA’s head of China industrial research, a “more nationalist America” in the first six months of the year has likely given China more leverage to assume “a larger global, and especially regional, leadership role.”

This comports with what I said back in January, in a Frank Talk titled “China Sets the Stage to Replace the U.S. as Global Trade Leader.” With President Donald Trump having already withdrawn the U.S. from the Trans-Pacific Partnership (TPP) and promising to renegotiate or tear up other trade agreements—he recently tweeted that the U.S. has “made some of the worst Trade Deals in world history”—China has emerged, amazingly, as a champion of free trade, a position of power it will likely continue to capitalize on.

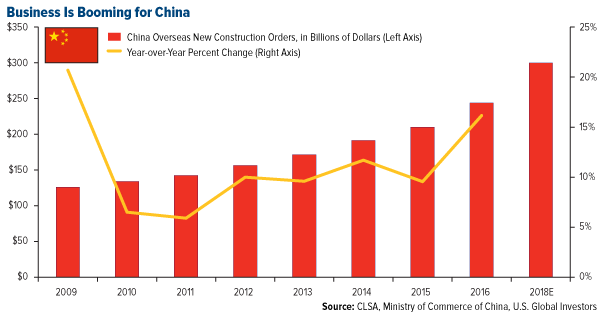

The country’s overseas construction orders have continued to expand, with agreements signed since 2013 valued at more than $600 billion.

Interested in investment opportunities in China and the surrounding region? Click here!

Emerging Europe Expected To Remain Strong

Another recent report, this one from Capital Economics, shows that the investment case for emerging Europe remains strong in 2017. Russia is expected to strengthen over the next 12 months, while Poland, Hungary, the Czech Republic and Slovakia are likely to remain attractive.

“Russia’s economy has pulled out of recession and growth in the coming quarters will be stronger than most anticipate,” the research firm writes, adding that its central bank’s loosening of monetary policy should support the recovery even further.

To be sure, the region faces strong headwinds, including a rapidly aging population and the loss of an estimated 20 million skilled workers to foreign markets over the past 25 years, according to a July 11 presentation from the International Monetary Fund (IMF).

But I believe that as conditions in central emerging Europe countries continue to improve, many of those workers will be returning home. Life in the region is not the same as it was 10 or 20 years ago, when good jobs might have been scarce. Firms are now growing at a healthy rate and hiring more workers. As you can see below, unemployment rates in Poland, Hungary and the Czech Republic have been falling steadily since at least 2012 and are now lower than the broader European Union.

This strength is reflected in emerging Europe’s capital markets. For the 12-month period as of July 12, Hungary’s Budapest Stock Exchange is up 38 percent. Poland’s WIG20 is up more than 43 percent. Meanwhile, the STOXX Europe 600 Index—which includes some of the largest Western European companies—has made gains of only 17 percent over the same period.

Learn more about investment opportunities in emerging Europe by clicking here!

Markets Still Believe In Trump

As we all know, the mainstream media’s criticism and ire aren’t reserved for China alone. Ninety-nine percent of the media right now is against President Trump, for a number of reasons—some of them deserved, some of them not.

Markets, however, seem not to care what the media or polls have to say. The Dow Jones Industrial Average continues to hit new all-time highs. Even though it’s stalled a few times, the “Trump rally” appears to be in full-speed-ahead mode, more than eight months after the election.

Back in November, I wrote about one of my favorite books, James Surowiecki’s The Wisdom of Crowds, which argues that large groups of people will nearly always be smarter and better at making predictions than an “elite” few. Surowiecki’s ideas were vindicated last year when investors accurately predicted Trump’s election, with markets turning negative between July 31 and October 31.

For the same reason, I think it’s important we pay close attention to what markets are forecasting today.

The White House is under siege on multiple fronts, which, as I said, has been positive for gold’s Fear Trade. But equity investors also seem to like the direction Trump is taking, whether it’s pushing for tax reform and deregulation or shaking up the “beltway party,” composed of deeply entrenched D.C. lobbyists and career bureaucrats. Just last week, the president made waves for firing a number of bureaucrats at the Department of Veteran Affairs (VA), long plagued by scandal and controversy. Since he took office in January, Trump has told more than 500 VA workers “You’re fired!”

The Fundamentals Of “Quantamental”

Of course, we look at so much more than government policy when making investment decisions. We take a blended approach of not only assessing fundamentals such as market share and returns on capital but also conducting quantitative analysis.

It’s this combination that some in the industry are calling “quantamental” investing. At first glance, “quantamental” might sound like nothing more than cute wordplay—not unlike “labsky,” “bullmation” and other clever names we give mixed-breed dogs—but it’s rapidly replacing traditional investment strategies at the institutional level.

Business Insider puts it in simple terms: “Quantamental managers combine the bottom-up stock-picking skills of fundamental investors with the use of computing power and big-data sets to test their hypotheses.”

See my Vancouver Investment Conference presentation, “What’s Driving Gold: The Invasion of the Quants,” to learn more about how we use quantitative analysis, machine learning and data mining.

Wall Street: The Birthplace of American Capitalism and Government

The concept of quantamentals helps explain our entry into smart-factor ETFs. As most of you already know, members of my team and I visited the New York Stock Exchange (NYSE) three weeks ago to mark the launch of our latest ETF.

While there, Doug Yones, head of exchange-traded products at the NYSE, gave us a short history lesson about the exchange and surrounding area.

Most investors are aware that the NYSE, which is celebrating its 225th anniversary this year, is the epicenter of capitalism—not just in the U.S. but also globally.

What many people might not realize is that on the site where the exchange now stands, Alexander Hamilton, the first U.S. treasury secretary, floated bonds to replace the debt the nascent country had incurred during the Revolutionary War.

Right next door to the NYSE is Federal Hall, where George Washington took his first oath of office in April 1789. The building today serves as a museum and memorial to the first U.S. president, whose statue now looks out over Wall Street and its passersby.

In this one single block of Wall Street, therefore, American capitalism and government were born. Here you can find the essential DNA of the American experiment, which, over the many years, has fostered our entrepreneurial spirit to form capital and to create new businesses and jobs. Growth, innovation and competition run through our veins, and that’s largely because of the events that unfolded centuries ago at the NYSE and Federal Hall.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Budapest Stock Exchange Index is a capitalization-weighted index adjusted for free float. The index tracks the daily price-only performance of large, actively traded shares on the Budapest Stock Exchange. The WIG20 Index is a modified capitalization-weighted index of 20 Polish stocks which are listed on the main market. The STOXX Europe 600 Index is derived from the STOXX Europe Total Market Index (TMI) and is a subset of the STOXX Global 1800 Index. With a fixed number of 600 components, the STOXX Europe 600 Index represents large, mid and small capitalization companies across 18 countries of the European region: Austria, Belgium, Czech Republic, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

For more insight and commentary like this, subscribe to my award-winning CEO blog, Frank Talk.

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com. You can contact Frank at: [email protected].

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com. You can contact Frank at: [email protected].