Strong Contrarian Bear Potential Into Inauguration Day

share

share

share

share

share

share

share

share

share

share

Signals in support of a contrarian bear setup in the US Stock.

Let’s look at some pictures of the developing risk situation in the US stock market, in light of Inauguration day upcoming on January 20, 2025, when the new president will be sworn in and his “Make America Great Again” jingle reconstituted. This group of indicators is far from exhaustive, as we use several other indicators and tools in the NFTRH service, many of which also currently forecast a coming phase when risk is to be realized, rather than just implied, as it is now.

That in itself – the probability that a large percentage of market participants believe that the “businessman” president will be good for equities – is a significant contrary indicator on its own, with the election hype coming after a year when the previous administration did all it could to keep the markets propped (successfully, and yet they were still ousted). The corporate tax cutting, deregulating new(ish) president may indeed turn out to be good for equities, but we are talking market forces in the here and now and the prospect of an oncoming bear phase, as opposed to the 4 year presidential term upcoming.

I do not personally, nor does NFTRH, manage the markets from the long-term “stocks always go back up again” point of view that is so adhered to by a vast majority. I want to miss the market liquidations, draw-downs and crashes, thank you very much. I want to catch the buying opportunities, a we did in Q1-Q2, 2020. As we did in Q4, 2008. Indeed, NFTRH was launched on September 28th of that year, in part because I saw the epic buy opportunities shaping up at the time and thought ‘it’s now or never’.

While not an accomplished short seller by any means, I’d like to try to patiently set up to capitalize on coming bearish events as well. But that is a lesser priority when cash and quality equivalents should manage risk just fine – and pay out income along the way.

This survey from AAII (Ma & Pa, AKA individual investors) members was taken after the election of one Donald J. Trump. 40% of members see the election result as positive for stocks and 63% see it as neutral or better. When you consider that half the country’s population voted against Trump, the results are clear; it’s a bearish contrary indicator.

aaii.com

With SPX looking upward at our operating target of 6180, a potentially final suck-in of the (dumb money) FOMOs is in progress. The daily RSI divergence supports the view of a coming top of some kind.

While there can be long phases when contrary indications are in place but stocks continue to rise or remain aloft, public sentiment will always be over-bullish at important market tops. The Public Optimism/Pessimism spread is currently over-bullish and is an intact “condition” for a market top, not a timing tool for a top.

Sentimentrader.com (my markups)

Here is an interesting historical indicator, the BMPM or Bear Market Probability Model. This indicator is cooked up by Goldman Sachs using five fundamental inputs: the U.S. Unemployment Rate, ISM Manufacturing Index, Yield Curve, Inflation Rate, and P/E Ratio. Whatever the inputs, the indicator’s forecasting record is excellent, even though its timing record, like many internal and sentiment indicators, is not good. So it is another indicator that is an intact condition for a top. Big time.

Most notably now, the last two major sell opportunities, 2006-2008 and 2019-2020 came after the indicator had been slipping for extended periods (orange arrows). My contention is that the 2022 correction has been inappropriately labeled a bear market by a majority of participants and media. In 2022 the SPX trend (higher highs/lows) remained intact to its bull market that began in 2009. It was a healthy correction, not a bear market. It all happened within one of those extended slips in the BMPM and that slippage is still in play. Risk is very high by this indicator.

Sentimentrader.com (my markups)

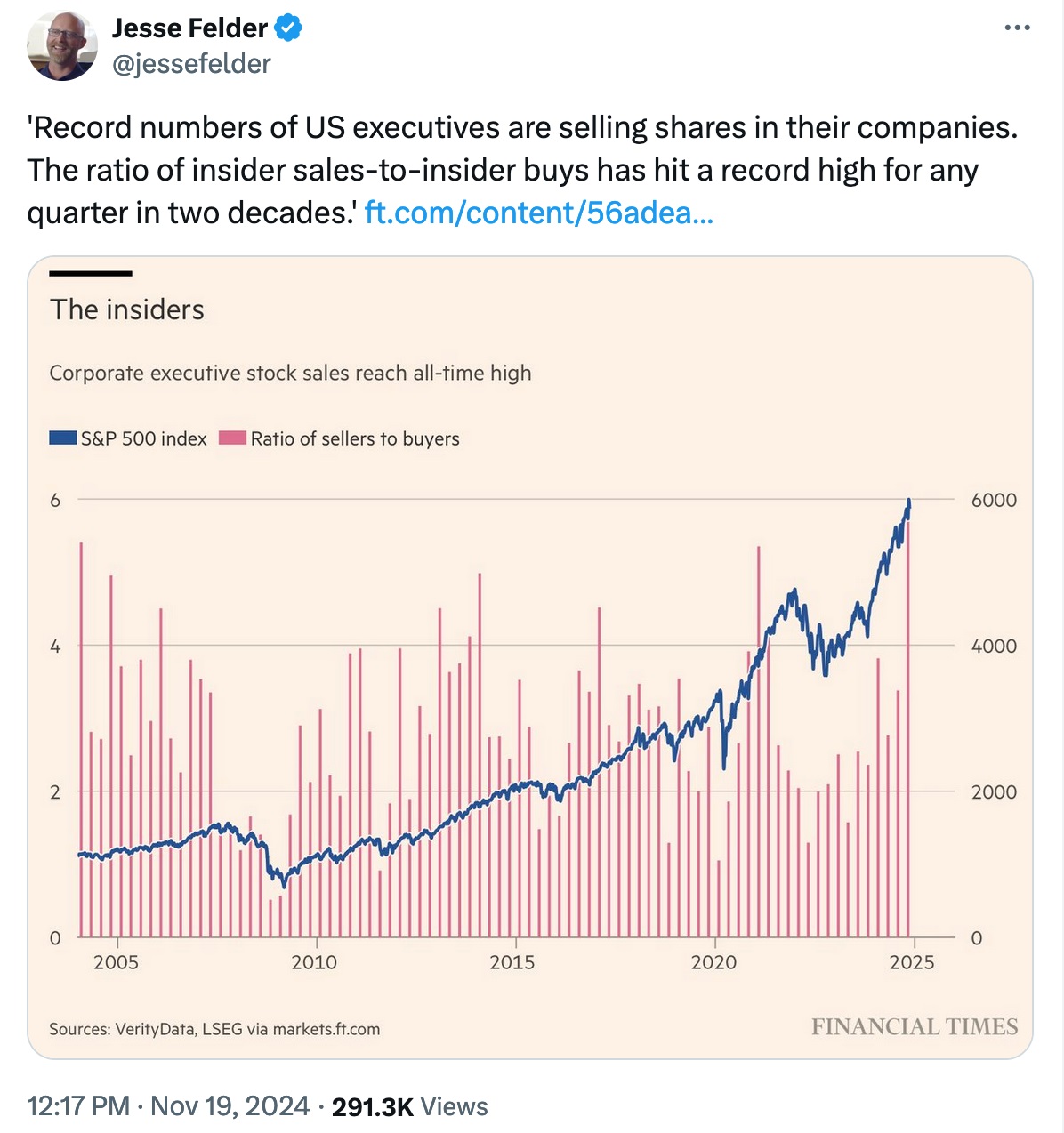

Jesse Felder had a good presentation of a couple of risk indicators, the net selling of corporate insiders and the market’s nosebleed valuations, on November 22. Here is the graph showing another topping “condition” (as opposed to a timer) currently in place.

From the vantage point of the Junk bond market we find investors’ appetite for the riskiest bonds (and their higher payouts) relative to quality bonds to be gluttonous, to an epic degree. Extreme investor complacency (and greed) like this will be in place at the next market top.

From the vantage point of market volatility, you can insert the same conclusion as directly above, with the added element of a still-intact divergence by the VIX to the northerly traveling S&P 500, going its way, seemingly without a care in the world. This divergence adds more caution to the high risk signal (and topping “condition”, not timer) of an extremely depressed VIX, which will always be in that state at important market tops.

There are many more market indicators and internals, from the Semiconductor > Tech > Broad (SPX) leadership chain, to yield curves, to the still-intact divergence of the 2yr Treasury yield to the (Fed proxy) 3 month T-bill yield, to the combo of the US dollar and the Gold/Silver ratio, and so many other indicators guiding the way forward and providing us with a smooth, manageable path as they have all year.

Each week NFTRH balances these macro and sentiment indications with nominal TA and trend analysis on markets and stocks to keep its subscribers on the right path. It’s been working for all of 2024 because I, as a human with emotions, have wanted to short this mess in the worst way. But the analysis has thus far only delivered conditions, but not triggers.

I’d like to make a final note. When presenting bearish analysis like the above, it is important to disclaim personal status. As of the writing of this article, I am not (yet) talking my book because the only current short position in my book is a hedge on the gold mining sector. Currently, I am in a slow process of selling and net profit taking, much like the corporate insiders are currently doing as they cash out while dumb money FOMOs and drives the market’s final MOMO phase. I am also building up defensive positions relative to risk-on positions. Cash is the ultimate defense, certain sectors are defensive and short-term Treasury bonds are defensive. All of those are actively favored right now.

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed market updates and NFTRH+ dynamic updates and chart/trade setup ideas. You can easily subscribe by Credit Card or PayPal (see all info and options). Keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar, or take it to another (intermediate) level with our free eLetter. Follow via Twitter@NFTRHgt.

*********

share

share

share

share

share