When The Fed Is Between A Rock And A Hard Place, Got Gold?

share

share

share

share

share

share

share

share

share

share

2022.01.05

Inflation is one of the best determinants of gold price movements, because investors buy precious metals (gold, silver, platinum and palladium) as an inflation hedge when the prices of goods and services are rising faster than interest rates.

Although gold offers neither a yield (bonds, GICs) nor a dividend (stocks and mutual funds), it is considered a smart investment when inflation diminishes an investor’s principal or erodes the purchasing power of a currency.

Gold is even more popular when real interest rates, typically the yield on the US 10-year Treasury note minus the inflation rate, are below zero, like currently.

The reason for this is simple, when real interest rates are at or below 0%, cash and bonds fall out of favor because the real return is lower than inflation. If you are earning 1.6% on your money from a government bond, but inflation is running 2.7%, the real rate you are earning is negative 1.1% — an investor is actually losing purchasing power. Gold is the most proven investment to offer a return greater than inflation, by its rising price, or at least not a loss of purchasing power.

Bond market and gold market observers keep a close eye on US Treasury yields, particularly the benchmark 10-year, because it serves as a proxy for other financial products, such as mortgage rates, and it also signals investor confidence. When there is low confidence in the economy, people want safe investments, and US Treasuries are considered among the safest. Demand for Treasuries bids up their prices and yields fall. Conversely, when confidence returns, investors dump their bonds, thinking they do not need to play it safe. This causes bond prices to sink and yields to climb.

The current 10-year Treasury note yields 1.74% and the December CPI rate of inflation is 7%, making real interest rates minus 5.26% — an ideal environment for gold prices.

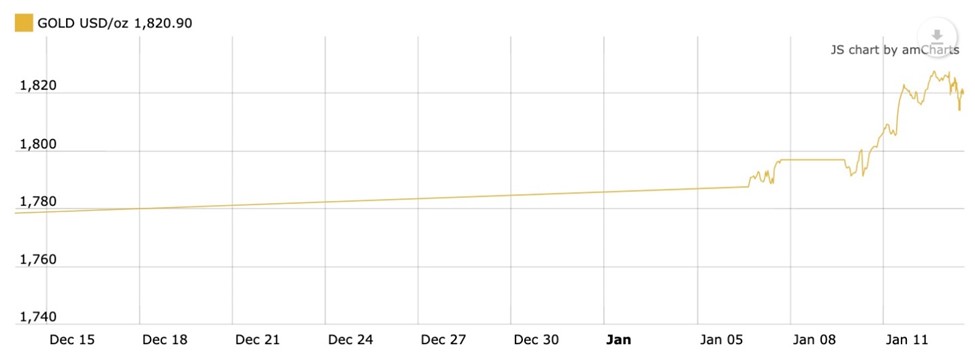

Spot gold on Friday climbed to $1,816/oz, at time of writing, corresponding with a lower US Dollar Index (DXY has fallen from 96.32 at the start of January to 95.17 currently) and following the release of December inflation figures.

1-month spot gold. Source: Kitco

1-month US Dollar Index DXY. Source: MarketWatch

Those hoping for a reprieve from the highest US inflation in decades, which many, wrongly imo, attribute to pandemic-related supply chain disruptions (there are in fact a number of reasons why current higher prices are likely to be with us for a long time) were disappointed.

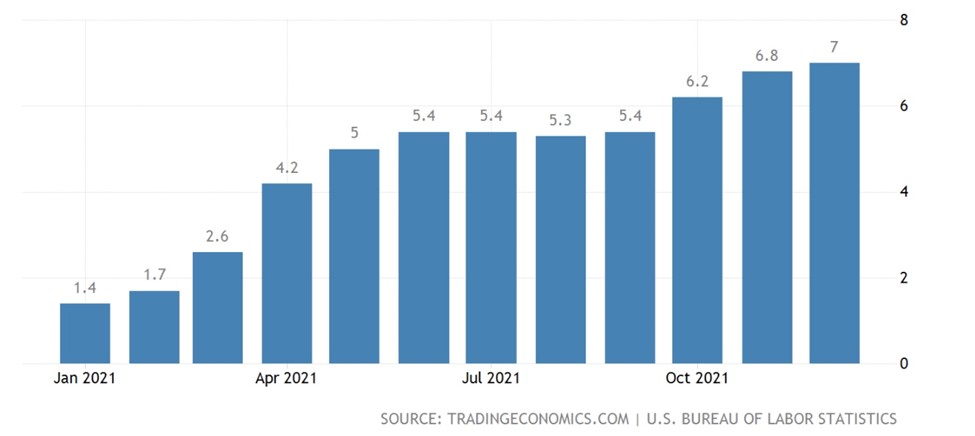

The US Labor Department said that its Producer Price Index (PPI) rose 0.2% from November to December, bringing producer prices to a record-high 9.7%, the biggest calendar-year increase since data was first calculated in 2010, the Labor Department report said.

The same report said US consumer prices increased solidly in December, led by gains in rental accommodation and used cars, culminating in the largest annual inflation rise in 40 years. The Consumer Price Index (CPI) surged 7% in the 12 months through December, which is the biggest year on year increase since 1982.

US inflation rate (CPI)

The US Federal Reserve, whose job is to keep unemployment in check and inflation (the Federal Funds Rate) in the “Goldilocks” zone of 2%, is telegraphing three interest rate increases of 0.25% each (1% at the high end of the range) this year.

The US government produces two main inflation indices, the Consumer Price Index (CPI) and the Personal Consumption Expenditures Index (PCE), and two “core” variations that exclude certain “volatile” goods. All have risen faster and more persistently than the Fed expected.

It’s important to note, the Federal Reserve doesn’t count food and fuel in its regular inflation forecasts, preferring the “PCE inflation” metric. As the name suggests, the Personal Consumption Expenditures price index measures changes in the prices of consumer goods and services. Thus the Fed is deliberately understating the real inflation rate, how they can exclude food and gas prices is beyond comprehension, we all eat, and we all use transportation.

The problem with the Fed’s game plan of a 1% increase in each of the next two years, is it is too dovish for what is required.

Arguably, rate adjustments of 2% will have little to no effect on skyrocketing inflation.

Yet herein lies the dilemma — anything beyond that could have a very negative impact on the US economy, because each interest rate rise means the federal government must spend more on interest, reflected in the annual budget deficit, which keeps getting added to the national debt, currently at $29 trillion and climbing.

A 0.75% interest rate hike would increase the interest costs per household by $1,400. That will hit the consumer right in the pocketbook, as will higher mortgage rates, car loans and credit cards, which will all go up following the rise in the Federal Funds Rate.

Corporations will also feel the squeeze. The interest on their loans will increase, forcing them to hike prices. Again the consumer pays. In the worst cases, companies will lay off staff, hurting workers and pushing the most vulnerable into severe economic hardship.

The US has borrowed about $6 trillion over the past 2.5 years to fight covid, placing a heavy burden on its finances.

The Congressional Budget Office (CBO) estimates that interest costs were $331 billion in 2021.

According to the Committee for a Responsible Federal Budget, each 1% rise in rates would increase interest costs by roughly $225 billion at today’s, end of 2021, debt levels.

We know that the Fed is planning a 1% rate increase this year. We also know that the federal deficit hit $2.8 trillion in 2021, the highest ever, except for 2020, an outlier due to massive coronavirus pandemic spending. For easy math, let’s call it $3T.

2022’s interest costs are calculated as follows: $331B (from 2021) + $225B (+1% rate hike) = $556B. This is without the debt increasing, but we know it’s going to increase, by at least $3T (2021 budget deficit).

The Fed is planning another 1% rate increase in 2023. 2023’s interest costs are calculated as follows:

$556B (from 2022) + $225B (+1% rate hike) = $771B. This is the interest payment due at the end of 2023. But again, this is without any new debt. Let’s add it.

The Congressional Budget Office (CBO) and the Committee for a Responsible Federal Budget (CRFB) — both reliable sources — project a deficit of $1.3T in 2022, and every year until 2031. This is the amount per year that will be added to the national debt, currently sitting at $29T.

Here are the total interest costs in 2023:

If we take the $29T debt and add $3T (2021 deficit) + $2.6T (deficits to end of 2023) = $34.6T, we are increasing the debt by ~20%. 20% of $781B is $156B. $781B + $156B = $937B. So at the end of 2023, interest payments will be almost $1T.

This to me is a very conservative figure. It doesn’t include Biden’s trillion-dollar infrastructure spending package that has been passed, nor additional covid-19 relief measures which are probable, with no sign of the pandemic letting up, two years in.

Inflation plays a big role here. Consider: even if the supply chain issues get ironed out (a big “if” given that covid appears to have taken on new life as the omicron variant), and that takes care of half the current 7% rate of inflation, there will still be another 3-4% inflation (food, energy transition, wage spiral, and climate crisis) left to deal with.

Let’s suppose the Fed wants to get serious about fighting inflation. Does it really think it can raise rates by a factor of 4, to match 4% inflation?

In 2023, interest costs could amount to $937 billion.

But that only brings rates up to 2%. Doubling the Federal Funds Rate to 4% would mean interest costs of nearly $2 trillion. Where is the government going to find the money?

There are only three choices: issue bonds, raise taxes, or print money. Higher taxes hit the poor and the middle class hardest, and in the United States, 70% of the economy is consumer spending. US household debt is reportedly on the rise, with families across the country more than $15 trillion in the red, according to personal finance app Nerd Wallet, via Twitter. The average household owes a whopping $155,622.

Next let’s consider the possibility of issuing more bonds. In a previous article we identified the trend of foreign buyers slowing their US Treasury purchases. Instead of foreigners buying T-bills, it is increasingly Americans, including consumers, banks and the biggest buyer of them all, the US Federal Reserve. From 2008, when the Fed balance sheet was ‘just’ $1 trillion, four rounds of quantitative easing, where the Fed engaged in monthly asset purchases of government bonds and mortgage-backed securities, to stimulate the economy, has raised the balance sheet to over $8 trillion. Since the fourth round of QE started in the spring of 2020, the Fed’s total assets have more than doubled.

Fed balance sheet. Source: US Federal Reserve

Again the inflation problem is paramount. The incentive for buying a US Treasury bill or bond is gone, the buyer’s purchasing power eroded by inflation. Wolf Street gives us a good explanation.

The current Federal Funds Rate is .08%, but CPI inflation is 7%, giving a real (after inflation) Effective Federal Funds Rate (EFFR) of -6.94%. This is the most negative EFFR since 1954. The real interest rate on savings accounts and Certificate of Deposit (CD) accounts, and the real yield on short-term Treasuries, is similarly -7%. The 10-year yield, which pays better interest, is -5.3% in real terms.

Even junk bonds, considered highly risky compared to Treasuries, have real yields below 0%. As Wolf Richter points out, You have to go to CCC-rated junk bonds – “substantial risk” of default – to get a yield above the rate of CPI inflation.

It really does beg the question, when foreign countries, individuals and corporations stop buying Treasuries, and Americans finally realize they are losing their T-bill purchasing power to inflation, who is going to buy US debt?

That leaves only one option available to the US government, and that is printing money — which of course, is inflationary — especially if the printing is “helicopter” style as in direct stimulus payments to consumers, which is responsible for a good percentage of the current CPI increase.

The Fed (and the Treasury) is between a rock and a hard place, the Fed can’t raise rates to combat high inflation because doing so will wreck the economy, and imo, the Treasury will soon struggle to find enough buyers for US government bonds because the yields are so low, in all cases negative.

Historically, the way the Fed has handled economic crises is to lower interest rates. We see this in the chart below by Real Investment Advice.

Source: Real Investment Advice

The 10-year rate started out at 4% in 1965 and hit a 57-year peak of >14% during the 1982 Latin American debt crisis. Almost every crisis, including the 2000 dot-com crash, the 2007 sub-prime mortgage debacle, and covid-19, has been followed by an interest rate cut.

Conclusion

In two years time will we look at this chart and see the black line rising, reflecting higher interest rates powering the US economy out of the covid-19 recession? Seems unlikely.

With 7% US inflation climbing faster and it being “stickier” than anticipated, the Fed has few policy options at its disposal. The horrendous yields on US Treasuries make them a poor investment, something foreign investors have already realized and US bond-buyers will surely cotton onto soon as well.

This practically guarantees the continuation of Fed bond buying (QE) despite the much-ballyhooed taper. As for raising rates, we have just proven that the Fed can’t do it, at least not at the levels required to beat 4% inflation, which may be charitable. We are talking about interest costs nearing a trillion dollars per year, when the deficit is accounted for.

In a recent article, Peter Schiff maintains that the government is using cooked CPI data that understates inflation. If it was using the formula it used in 1982, inflation would be higher in 2021 than it was then, he writes, just over 15%.

The fact is nobody is going to want to buy US debt at 7% inflation, let alone 15%. The Fed will continue to print money, buy bonds and keep interest rates below 1% for as long as it can — probably hoping that inflation will magically melt away — all of which is extremely positive for gold.

Rising geopolitical tensions continue to add to gold’s allure. There are a number of hot spots in the world today that could easily flare up into a conflagration that escalates into a shooting war or even the nightmare scenario of missiles being launched.

They include the ongoing threat of war between North and South Korea that would draw in the United States; tensions between the US, China and its neighbors over Taiwan; and a migrant crisis in Belarus that Ukrainian officials believe is a ruse invented by Russia to stage an invasion of Ukraine, similar to what happened in 2014 when Russian forces annexed Crimea.

There are 100,000 Russian troops on Ukraine’s border and on Friday photos were released showing its forces on the move. An alleged Russian cyberattack hit around 70 internet sites including the security and defense council, Reuters reported. Talks between Moscow and Western allies ended Thursday with no breakthrough.

When market participants see Fed rate increases as the hollow threats they are, amid rising and currency-debasing inflation, we expect many will see the light and return to gold.

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

*********

share

share

share

share

share