Where We Are Now

As we move into the final quarter of the year – a time when markets have been known to go bump in the night – finding an encouraging word on the gold and silver markets isn’t easy. As September ended, gold had broken below critical chart support levels after starting the month with promising moves to the upside. Of course, the precious metals are not alone in nursing deep wounds, for the most part, at the hands of a suddenly assertive Federal Reserve. Year to date, stocks (S&P 500) are down 24%; bonds (TLT) are down 28.3%, and crypto (Bitcoin) is down 57.4%. With those markets as points of comparison, silver (down 17%) looks respectable, and gold (down 7.6%) downright admirable. Only the US dollar – up 16.7% – has kept its head above water in 2022, but that gain is measured against the rest of the world’s lowly currencies. In the real world, where consumers must meet their living expenses and investors scramble to retain value, the US dollar has lost 8% of its purchasing power over the past two years.

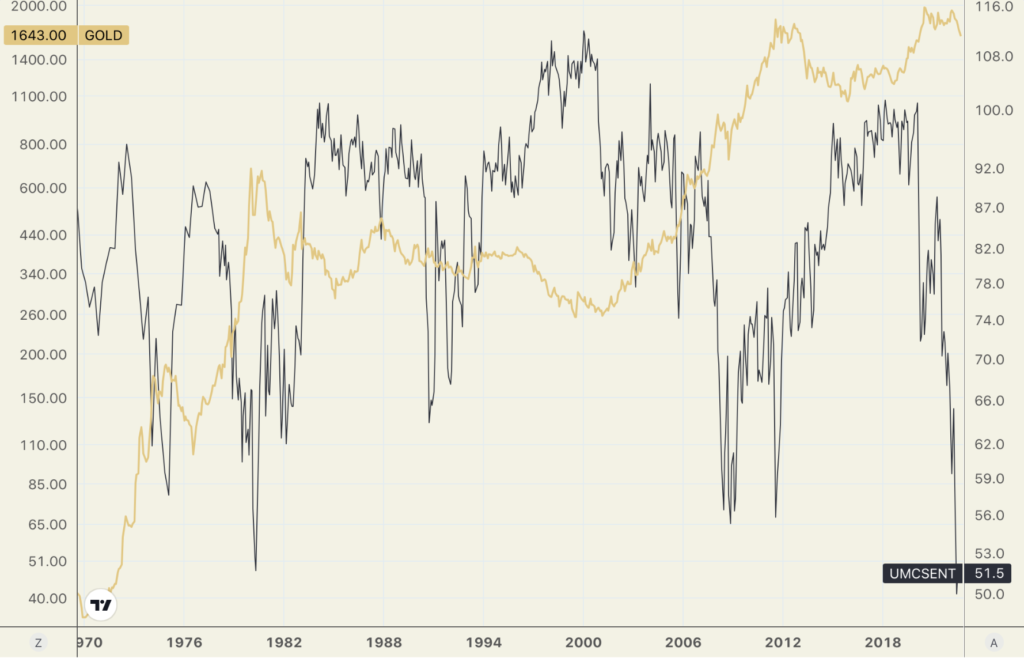

With that as the backdrop, we direct your attention to the chart posted directly below. It might be one of the more relevant included in this newsletter over the past several months. The University of Michigan Consumer Sentiment Index is now at its lowest level since 1971 (and, in fact, at a record low), a development that market analysts have largely overlooked. We superimposed the price of gold to show its long-term correlation with the ebb and flow of sentiment. The vertical downward spike in consumer sentiment has yet to be reflected in the price of gold, though demand remains strong globally. We would attribute that reticence to Wall Street’s trading houses, the dominant force in pricing on the major exchanges. Thus far, they have essentially bought into the Fed’s argument that it can control inflation with the right blend of tightening policies. Of late, though, a groundswell of analysts and money managers has begun to question if current Fed policies are genuinely up to the task.

University of Michigan Consumer Sentiment Index and the price of gold

(log scale, 1971 to present)

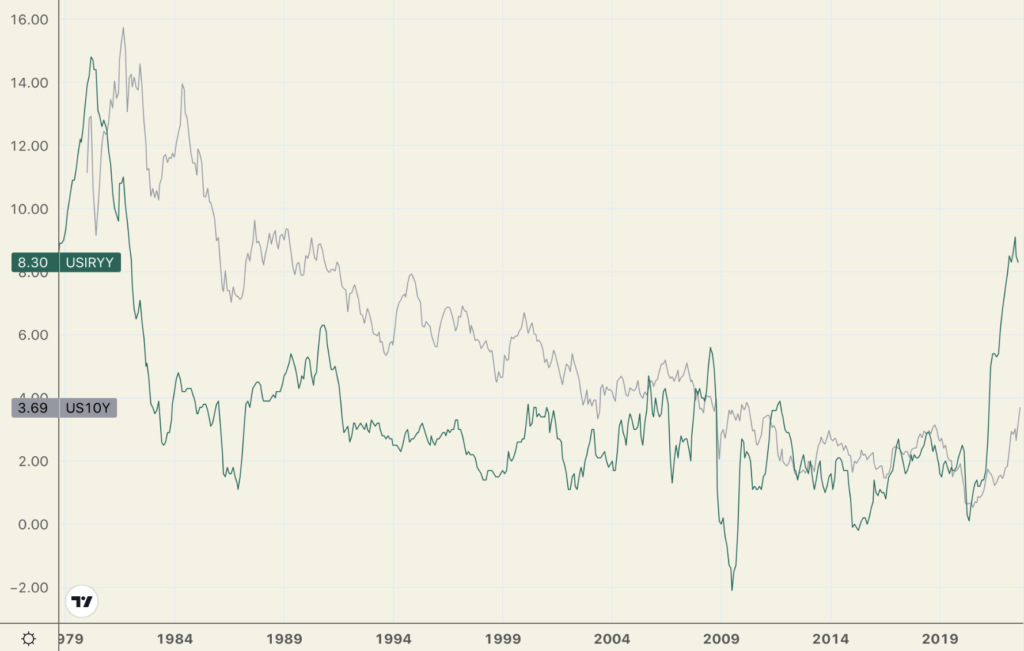

In an op-ed piece titled “What comes after a week that shook the world,” Bloomberg’s John Authers says that, as a rule of thumb, the fed funds rate must get above the inflation rate for policy to be “meaningfully restrictive.” If that is the case, he says, “this episode has a long way to run” – a view not too distant from our own. As shown in the chart below, there is considerable distance between the headline inflation rate at 8.3% and the yield on the 10-year Treasury at 3.7%. Authers goes on to explain that we have had a clean break with the past on two scores. The first is in the long-term trend of falling rates. The second is in the real rate of return on the 10-year Treasury. “We’re living through arguably the most truly global attempt to tighten financial conditions in memory,” he warns. “This is shifting the tectonic plates beneath the world economy and threatens dangerous developments in society and in politics as we all try to adapt. And yet what strikes the eye after a week of market landmarks and aggressive interventions by central banks is the continuing discord.”

Albert Edwards, the chief investment strategist for Societe Generale, offers an even more pointed assessment of where we are now. “The theme of secular stagnation which underpinned our Ice Age thesis for so long,” he says, “has been dealt a fatal blow as politicians begin to shed their fiscal shackles. Until recently, economic ideology had prevented them breaking free from fiscal austerity. That had caused central bankers to fill the economic void with super-expansionary monetary policy. Those days are now over and aggressive fiscal activism reigns supreme, most visible currently in the UK. This will bring higher growth, higher inflation, and higher interest rates across the curve. The party for investors is over. The Great Melt will not only melt the ‘Ice’ in ‘Ice Age,’ but investor returns are set to melt away too.”

Yield on the 10-Year Treasury note and headline inflation

(%, 1980-present)

Charts courtesy of TradingView.com

Short & Sweet

AS WE MOVE INTO THE FINAL QUARTER OF THE YEAR, the one event in the recent past likely to leave an indelible impression is Britain’s surprise turnaround on monetary policy. It happened quickly and without hesitation. In the end, the risk of inflation was far preferable to a collapse of a large portion of the country’s pension system and the potential for a domino effect. Britain’s decision will not be lost on investors in other nation-states whose bond markets rest on similarly shaky ground. Historically, central banks have opted for monetary inflation as their baseline policy because the alternative – an economic depression – is something no policymaker wants to add to their resume. Demand for gold is running strong in the United Kingdom, and its price in British pounds is up almost 12.5% so far this year.

ONE CAN NOT HELP BUT RECALL, under these circumstances, Britain’s decision in the late 1990s to auction off a significant portion of its gold reserves in order, it said, to diversify into various currencies. What would it give today to have that asset still on the books – one it sold for under $300 per ounce? As it turns out, the BoE sale was among the last major liquidations before the group went from net sellers of the metal to net buyers in 2011. Since then, the official sector has added over 5000 metric tonnes to global reserves (See chart.). International Banker’s Nicholas Lawson says there is now an “insatiable appetite for the yellow metal” among central banks.

“WHERE IS THE SILVER GOING that is leaving the LBMA and COMEX?” asks market analyst Patrick Heller in a Numismatic News article. Metals Focus India reports that silver demand in that country, perhaps the world’s top silver consuming nation, is now so strong that the silver price in India is trading at a premium to the world silver spot price. In July 2022, almost 58 million ounces of physical silver were imported into India. This was at least 50 percent higher than in any month in the previous four years and may be an all-time high record amount of imports into India in any month.” LBMA physical silver stockpiles are now at their lowest level since 2016. Likewise, COMEX inventories are currently running at about one-third of what they were in 2020. Silver, like gold, travels west to east.

“SOMETHING STOPPED THE SELLING OF PAPER GOLD and silver back then [in 2008], “writes Investment Research Dynamic’s David Kranzler, “some trigger event – and the paper shorts scrambled to start covering, driving the market higher and setting off a 2 1/2 year bull move in the precious metals sector. Whatever that catalyst was – and it was connected to the de facto credit market/banking system collapse – will be triggered again. It’s a matter of timing.” Kranzler refers to the “bifurcated” structure of the gold market – paper gold vs. physical gold. As a result of the low pricing generated in the paper market, he says, there has been a large flow of cheap gold and silver to buyers in the Eastern hemisphere. Now, he cautions, “the set-up in the markets is startlingly similar to that of late September and early October 2008.” He predicts a similar trigger event to occur possibly before Christmas.

Gold price and major market events of 2008

Chart courtesy of TradingView.com • • • Click to enlarge

Annotations by USAGOLD

“WITH THE FED DOUBLING THE PACE at which its bond holdings will ‘roll off’ its balance sheet in September, some bankers and institutional traders are worried that already-thinning liquidity in the Treasury market could set the stage for an economic catastrophe — or, falling short of that, involve a host of other drawbacks,” writes Joseph Adinolfi in a MarketWatch article. We’ve worried about a black swan event precipitated by quantitative tightening for quite some time. It’s not just the selling – that’s one thing. The sudden withdrawal of support for bond issuance from the federal government is also a cause for concern. As you probably already know, both China and Japan – the two largest foreign holders of U.S. Treasuries – are out of the market. Though the Congressional Budget Office optimistically projects the borrowing needs of the federal government will decline to $1 trillion in 2022, it still projects a $1.6 trillion shortfall from 2023 through 2032. Consider, too, that revenue usually falls during recessions, while spending ramps up.

IN THIS LARGE UNSETTLED INVESTMENT ENVIRONMENT, influenced heavily by algo-based trading systems, It would be a mistake, in our view, to draw hasty conclusions. The jury is still out on how the investment community will adjust to the current inflation trend. Keep in mind it has not even been a year since Wall Street fully embraced Fed reassurances that inflation was transitory. For better or worse, it still clings to that notion when it is more and more looking like wishful thinking. In fact, there is a growing perception that headline inflation could rise above the 9.1% high in June of this year. We’ve gone from Inflation not being a problem to being manageable, from manageable to transitory, from transitory to persistent, from persistent to a significant problem – all in the space of less than a year. And now, some believe the Fed may become more zealous than it needs to be, thereby inflicting more damage than is necessary.

STUDENTS OF ECONOMIC HISTORY WILL RECALL that during the 1970s, the Fed consistently informed the public of its commitment to taming inflation while simultaneously keeping interest rates below the inflation rate. All the while, inflation moved steadily higher. So, where is the current Fed? Is Jerome Powell following in the footsteps of Paul Volcker, as he intimates, or of Arthur Burns? At the moment, public posturing aside, Burns, in our view, looks to have the inside track.

WE HEAR A GREAT DEAL THESE DAYS ABOUT INFLATION as the chief influence on the price of gold. Still, a study recently published by the JP Morgan Center for Commodities at the University of Colorado finds that since 2001 it has taken a back seat to two other significant concerns. “Gold is regarded as protective against bad economic times,” reads the study. “…In the early part of the sample [i.e., 1971-2000], variation in inflation or inflationary expectations was the single most important consideration for the real price of gold. From 2001 on, however, long-term real interest rates and pessimism about future economic activity appear as the dominant factors. While disinflation since 2001 might have been expected to result in low gold prices, any effect of low inflation was more than compensated for by unprecedentedly low long-term real interest rates and by pessimism about future economic activity.”

“WE NEED TO GET OUT OF THESE DISTORTED MARKETS that have created a lot of damage,” famed economist Mohamed El-Erian recently told CNBC per a review of the conversation at YahooFinance. Both the stock market and the bond market have been tumbling lately, and HE notes that when these market corrections happen simultaneously, investors should move to ‘risk-off’ assets.” We will add that cash is king at the moment, but there might come a time when the markets reflect the full effect of stagflation, even runaway stagflation, and begin trading on economic fundamentals rather than chasing the latest speculative frenzy. When it becomes evident that real capital preservation is the name of the game, gold and silver are likely to become a favorite resting place for hot capital.

GLOBAL GOLD ETF STOCKPILES, the World Gold Council reports, declined for the fourth consecutive month in line with the price performance. However, UK-based analyst Charlie Morris isn’t all that concerned about the decline of interest among funds. “Don’t worry,” he advises in the latest edition of Atlas Pulse, “they’re collectively behind the curve, and you can guarantee they’ll be back.” Meanwhile, central banks continue to acquire the metal, with over 300 tonnes purchased thus far in 2022. “As the bond yield continues to rise,” writes Morris, “the downward pressure on US equities bites as they become extended. The move since March 2020 is one for the record books. The risk facing gold is marginal compared to the risk facing US equities, and it is hard to see a scenario where gold doesn’t win.”

–––––––––––––––––––––––––––––––––––––––––

The six keys to successful gold ownership

This eye-opening, in-depth introduction to precious metals ownership will help you avoid many of the pitfalls that befall first-time investors. Find out who invests in gold, what role gold plays in serious investors’ portfolios, and the when, where, why, and how of adding precious metals to your holdings. To end right, it is critical that you start right, and the six keys to successful gold ownership will point you in the right direction.

––––––––––––––––––––––––––––––––––––––––––

Notable Quotable

“I think what needs to happen for gold to become more responsive is if the Fed ultimately raises rates, the economy weakens, and they pause. And then they see they can’t control inflation. Then it’s not going to come down to 2%, at best. Maybe they get it down to 4%, 5% or 6%, and then the economy weakens, they have to ease again. And then inflation comes back. At that point long-term inflation expectations will rise. People will not believe the Fed can control it. And then I think gold rises to higher levels.” – John Paulson, Bloomberg Interview

“Perhaps what gives us the highest conviction on commodities as an asset class is not the similarities to historical bull markets but the differences. In particular we continue to believe that the global focus on climate mitigation strategies and decarbonisation is limiting the supply response to higher prices to an extent that is unprecedented. That breakage of the link between higher prices and a supply response is likely to significantly extend the commodities bull market. When we combine these factors to our belief that we are entering a fundamentally more inflationary age, the case for an enlarged commodities allocation remains compelling.” – Schroders, recent client advisory

“The Federal Reserve has two big levers to pull in its bid to influence the economy and tame inflation, and while most investors are fixated on interest rate policy, the Fed’s balance sheet plans can have an even bigger impact.” – Ned Davis Research, Markets Insider

“Not even the most hawkish Federal Reserve in decades can beat down the exuberance of gold enthusiasts at the industry’s biggest annual gathering. Bullion prices will reach $1,806.10 an ounce by year-end, according to the average estimate in a survey of 10 participants at the Denver Gold Forum, the yearly meetup of mining executives, investors, bankers and analysts.” – YahooFinance/Bloomberg report

Cartoon courtesy of MichaelPRamirez.com

“People tend to hear what they want to hear and believe what they need to believe. In no place is this more true than on Wall Street. The Fed has made abundantly clear that it will tighten monetary policy until inflation is virtually vanquished. And yet, those who have no choice but to be nearly fully invested at all times have completely ignored this fact and were left trying to convince the investing public not to believe their own ears.” – Michael Pento, Pento Portfolio Strategies

“There are three groups of traders [on the COMEX]: the commercials, the large speculators and the small speculators. The commercials tend to be seen as the smart money, and, as they are often acting on behalf of miners, they tend to be sellers and so they tend to be short. Every Friday evening, the positions of the various traders the previous Tuesday – the open interest, as it is known – is announced. On Friday we discovered something extraordinary. That the commercials are net long – ie buyers – for only the third time in 40 years. That suggests a genuine shortage of metal. Meanwhile the speculators, who for the most part do not have metal to deliver, are net short. This opens up the possibility for a short squeeze.” – Dominic Frisby, Money Week

“If you look at asset classes, bonds are certainly a problem, Bonds have not been so expensive ever. Property has been forming a bubble in many countries. Many technology stocks are also forming a bubble. The only asset class I know that is cheap are commodities, which are real assets. If we have inflation, you should own things that will go up in price. Real assets always go up in inflation and that is the way I am looking to protect myself.” – Jim Rogers, Live Mint interview

“Probably the more germane discussion would center around the impact of Fed liquidity withdrawals in a backdrop of de-risking/deleveraging and waning market liquidity. Moreover, it’s worth pondering potential market function issues for the global derivatives marketplace in the event of a serious bout of de-risking/deleveraging in conjunction with QT and central bank liquidity support (i.e. ‘Fed put’) ambiguity. Market liquidity and dislocation concerns make selling market protection an only riskier proposition. Summing it up, there’s a strong case that global markets are at the cusp of succumbing to Crisis Dynamics, which will be especially difficult to shake this time around. The Super Credit Bubble is at the brink. Quoting Grantham: ‘If history repeats, the play will once again be a Tragedy. We must hope this time for a minor one.’ I’m holding out hope, but nothing I see points to ‘a minor one.’” – Doug Noland, Credit Bubble Bulletin

“The European Central Bank can either bail out Italy,” he says, “or save its credibility in Germany. It will struggle to do both.” – Ambrose Evans-Pritchard, The Daily Telegraph

“Finally, the U.S. got very rich by doing QE. But the license for QE came from the ‘lowflation’ regime enabled by cheap exports coming from Russia and China. Naturally, the top of the global economic food chain – the U.S. – doesn’t want the lowflation regime to end, but if Chimerica and Eurussia are over as unions, the lowflation regime will have to end, period. As we noted in our prior dispatch, the special relationship between China and Russia (‘Chussia’) is a powerful one: a marriage of commodities and industry, uniting the largest commodity producer (Russia) and the factory of the world (China), potentially in control of Eurasia.” – Zoltan Pozsar, Credit Suisse

Final Thought

‘If you try and print too much money, it eventually causes terrible trouble.” – Charlie Munger

We have always emphasized inflation as a process rather than an event – a viewpoint that argues in favor of gold coins and bullion as a semi-permanent inclusion. Unfortunately, the Fed treated inflation as an event, and we see the results – failed policy, lost credibility, and an economy and financial markets on the brink of disaster. Charlie Munger, the outspoken 98-year-old partner in Berkshire Hathaway, also sees inflation as a process rather than an event.

“There’s never been anything quite like what we’re doing now,” he says in an interview posted on YouTube, “and we do know from what’s happened in other nations if you try and print too much money, it eventually causes terrible trouble. And we’re closer to terrible trouble than we’ve been in the past, but it may still be a long way off. I certainly hope so.… If you look at the Roman Republic, they inflated the currency steadily for hundreds of years. Eventually, the whole damn Roman Empire collapsed. So inflation it’s the biggest long-range danger we have probably, apart from nuclear war. I think the safe assumption for an investor is that over the next hundred years, the currency is going to zero. That is my working hypothesis.”

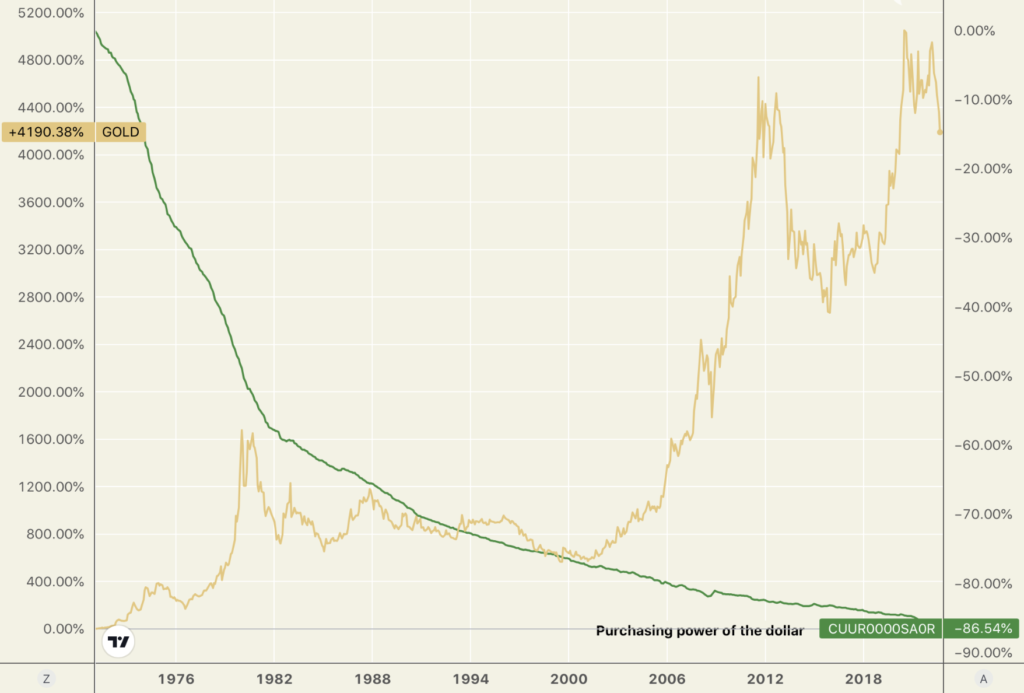

The chart below testifies to the viability of Munger’s “working hypothesis” and the notion that inflation is a process rather than an event. Since 1971, the year the United States severed the dollar’s link to gold, it has lost 86.5% of its purchasing power and is now worth 13.5¢. Over the same period, gold appreciated 4,190% – a historical record often overlooked by the mainstream media and too many financial advisors.

Gold and the purchasing power of the US dollar

(%, 1971-September 2022)

Chart courtesy of TradingView.com • • • Click to enlarge

______________________

Worried about the sequel to the Great Financial Crisis?

DISCOVER THE USAGOLD DIFFERENCE

ORDER DESK:

1-800-869-5115 x100 • • • [email protected] • • • ORDER GOLD & SILVER ONLINE 24-7

––––––––––––––––––––––

Disclaimer – Opinions expressed on the USAGOLD.com website do not constitute an offer to buy or sell or the solicitation of an offer to buy or sell any precious metals product, nor should they be viewed in any way as investment advice or advice to buy, sell or hold. USAGOLD, Inc. recommends the purchase of physical precious metals for asset preservation purposes, not speculation. Utilization of these opinions for speculative purposes is neither suggested nor advised. Commentary is strictly for educational purposes, and as such, USAGOLD does not warrant or guarantee the accuracy, timeliness, or completeness of the information found here. The views and opinions expressed at USAGOLD are those of the authors and do not necessarily reflect the official policy or position of USAGOLD. Any content provided by our bloggers or authors is solely their opinion and is not intended to malign any religion, ethnic group, club, organization, company, individual, or anyone or anything.

********

More from Gold-Eagle