Why Is The Dollar Rising As Treasury Yields Fall?

Generally speaking, the dollar and US bond yields rise and fall together, signaling a positive correlation between the two. Conversely, the price of a bond and its yield are negatively correlated. The lower the price, the higher its yield. A rising yield favors dollar bulls. Falling bond yields make for a softer dollar.

These are commonly accepted economic principles. Which makes it especially puzzling when the rules are broken.

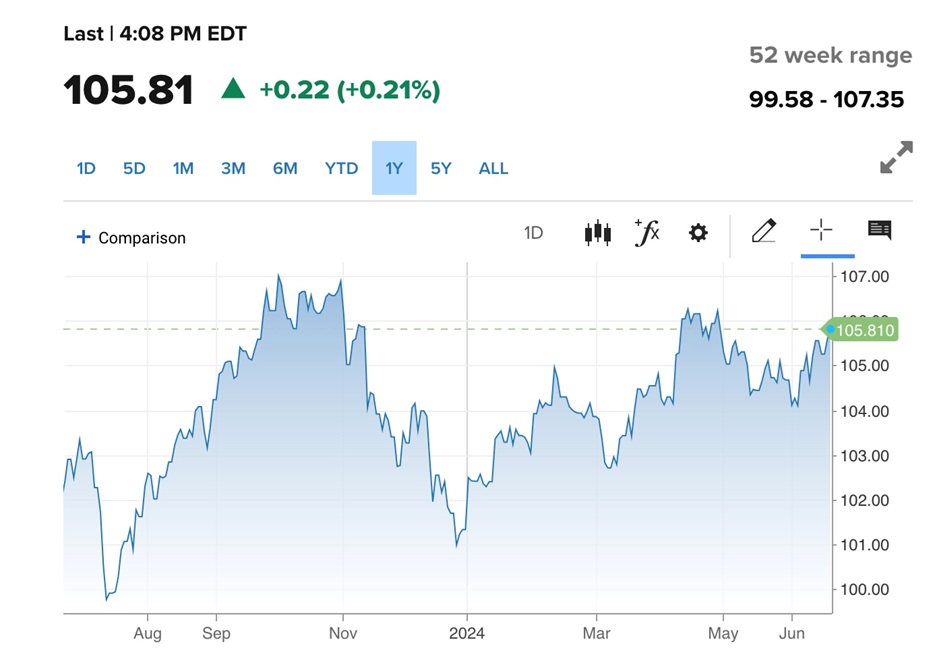

Demand for dollars has been strong, reflected in a US dollar index (DXY) over 105. DXY started 2024 at 102.49, and it is now at 105.80, a gain of 3.2%. This is partly due to the dollar functioning as a safe haven during war — the conflicts in Gaza and the Ukraine have raged all year and show no sign of ending — along with interest rates at their highest levels in 22 years, @ 5.25 to 5.50%.

US dollar index DXY. Source: CNBC

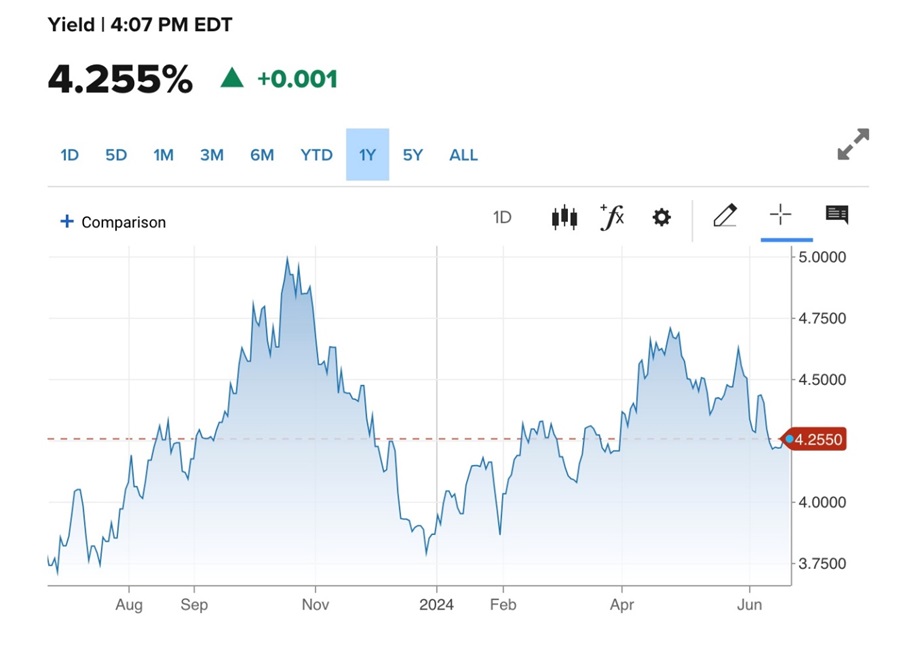

Yet Treasury yields are falling. The US 10-year Treasury yield as of Friday, June 21 was 4.25%. On April 24 the 10-year was at 4.70%, showing a drop of 10%.

US 10-year Treasury yield. Source: CNBC

The 2-year and the 30-year are also down, at 4.73% and 4.39% respectively.

So what gives? I have a theory, and it has to do with government debt and foreign Treasury purchases.

The Biden administration continues to spend beyond its means, and it likely won’t get any better under Trump, if he is elected in November, because Trump is promising tax cuts.

According to the nonpartisan Congressional Budget Office (CBO), this year’s deficit will be 27% higher at almost $2 trillion. The CBO sees the deficit reaching $1.92 trillion in 2024, about $400 billion higher than the $1.58T it predicted in February.

80% of the spike in the deficit can be blamed on four sources of funding, states free-market website Reason:

- $145B is due to changes in the federal student loan program that have resulted in massive waves of student loan forgiveness;

- The costs for deposit insurance have increased by about $70 billion because the Federal Deposit Insurance Corporation is not recovering payments it made when resolving bank failures;

- An additional $60 billion came from (unspecified) legislation;

- The remaining $50B came from higher-than-expected Medicaid costs.

Projecting further out, the CBO forecasts the federal debt will hit $50 trillion by 2034, or 122% of GDP.

While the dollar is the most important unit of account for international trade, the main medium of exchange for settling international transactions, and the store of value for central banks, “de-dollarization” is being pursued by countries with agendas at odds with the US, including Russia, China, Saudi Arabia and Iran.

Many emerging-market economies are buying gold because they don’t want to be stuck in the same situation as Russia, which had about half of its foreign-currency reserves frozen following the 2022 invasion of Ukraine.

Back to the debt, the CBO estimates the share of GDP going toward interest payments on the federal debt will increase to twice the amount Washington spends on national security by 2041.

Visual Capitalist in April reported the cost of paying for America’s national debt crossed the $1 trillion mark in 2033, driven by high interest rates and the ballooning national debt.

The CBO reported that debt servicing costs surpassed defense spending for the first time this year — something we warned would happen.

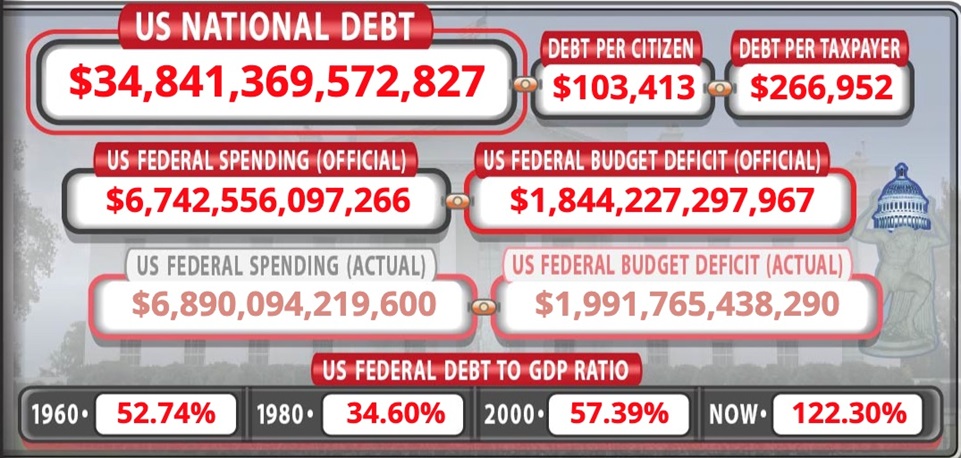

The US government relies on Treasuries to finance its increasingly out-of-control spending. Without Treasury buyers, the government could not continue to run budget deficits, which every year are added to the national debt, now sitting at a jaw-dropping $34.8 trillion.

Source: usdebtclock.org

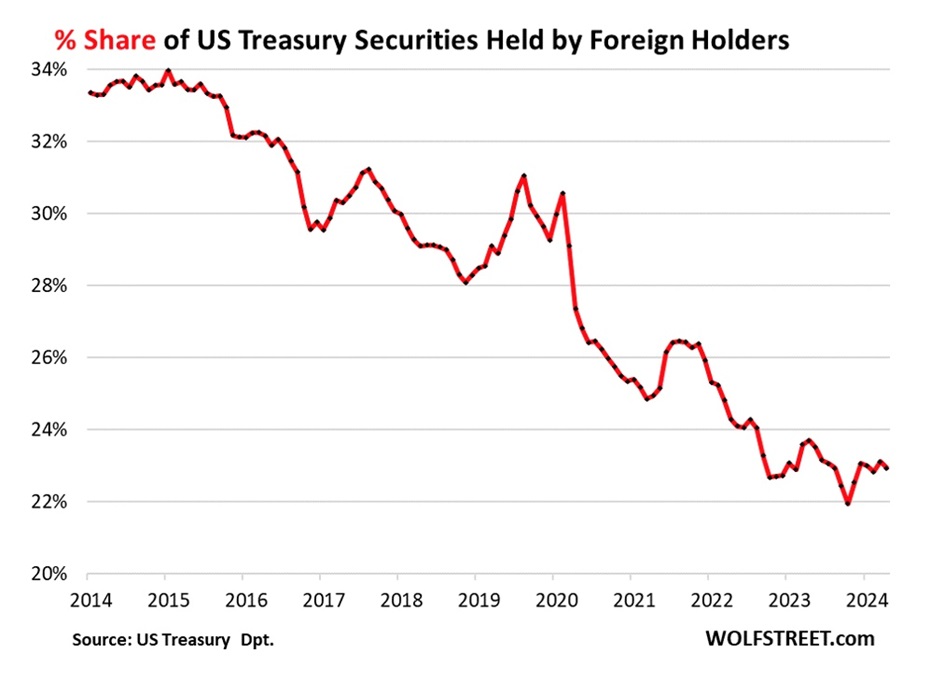

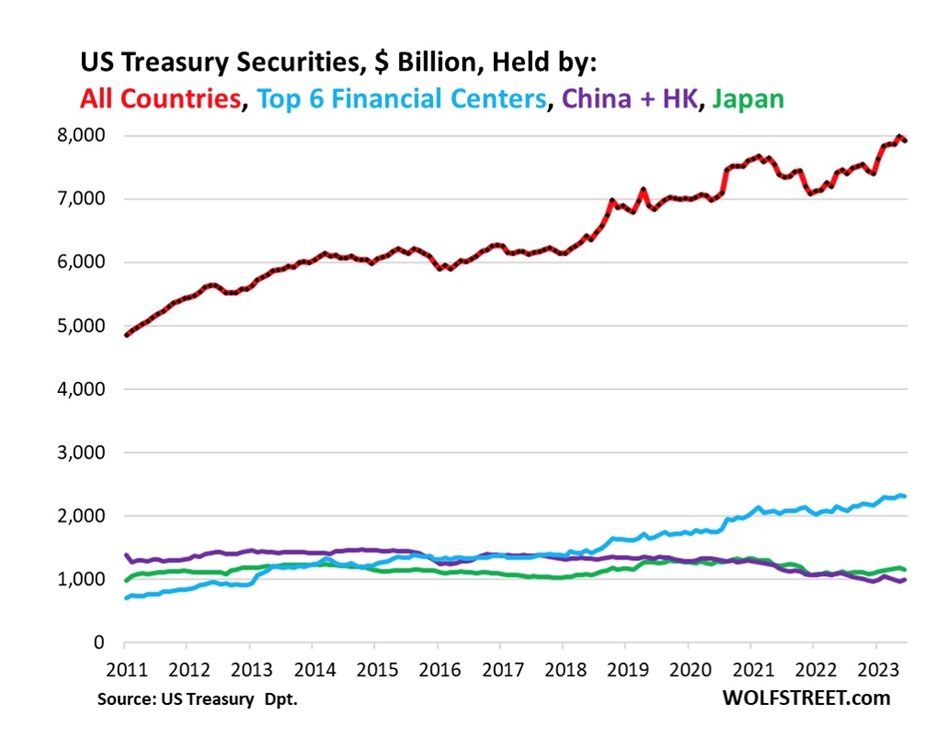

The first thing to understand is that foreign Treasury buyers have been declining. Foreign investors have continued to add to their holdings over the years, but the debt has grown faster, so the share of debt held by foreign entities has declined. In 2014-16, foreign investors held over 33% of the debt. Their share is now down to 22.9%. (Wolf Street, June 19, 2024)

Indeed, US debt financing has become less dependent on Japan and China, the biggest and second-biggest holders of American debt, who are pausing on buying, or dumping US Treasuries. Taking their place are Western buyers.

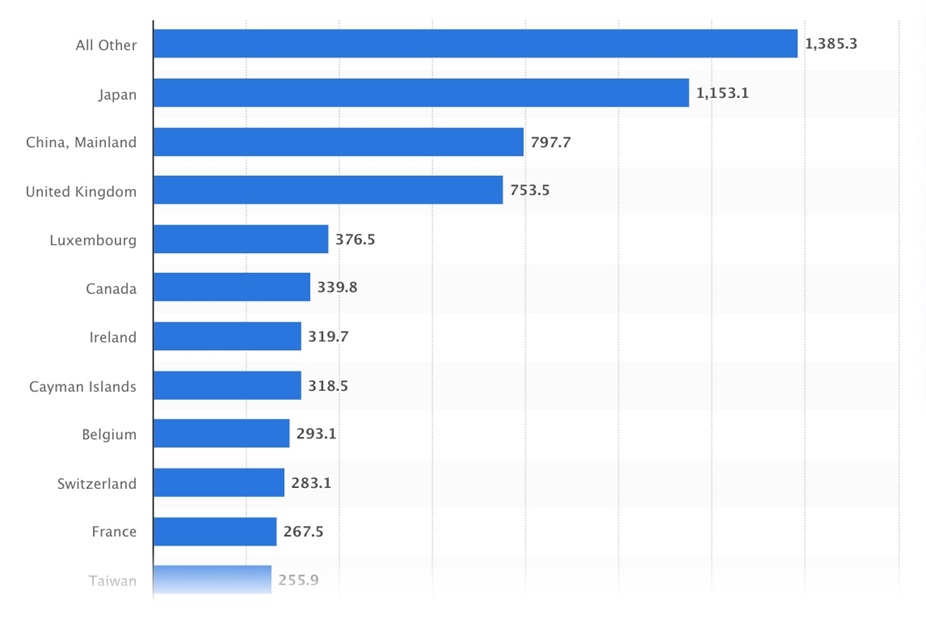

Major foreign holders of US Treasury securities as of January, 2024, in billions of dollars.

Source: Statista

Wolf Street provides charts showing that the top six financial centers (London, Belgium, Luxembourg, Switzerland, Cayman Islands, Ireland) currently hold $2.3 trillion in T-bills, a 9.2% increase year over year.

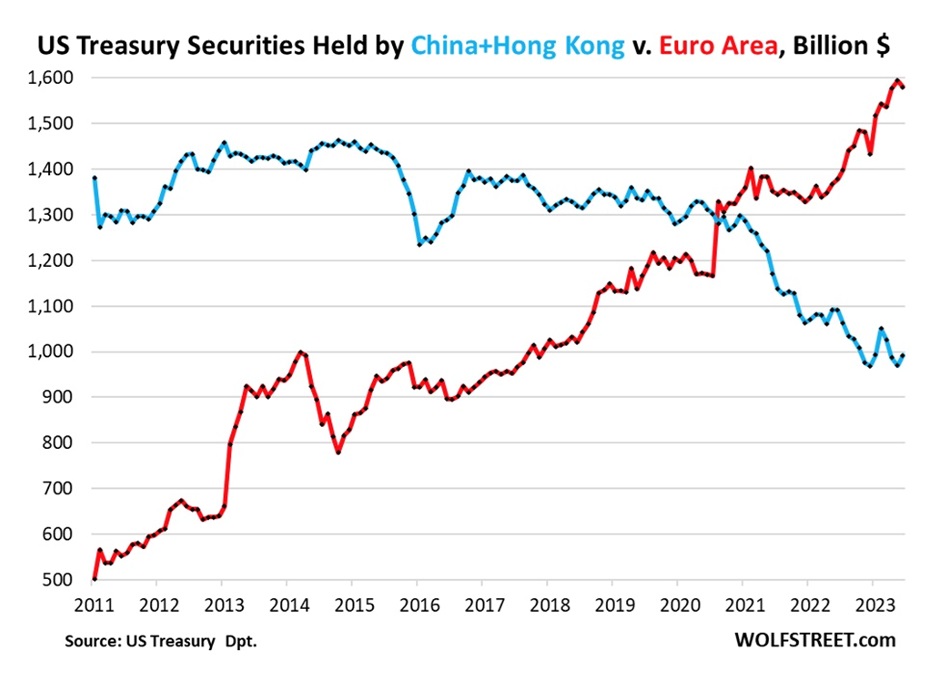

The countries of the Euro area have also been piling into Treasuries at a furious rate, expanding their holdings from $500 billion in 2011 to $1.58T now, says Wolf Street, adding that year over year, the Euro area’s holdings surged $202 billion, or 14.6%.

France is one of the biggest players, in April reaching a record-high $277 billion compared to Germany’s $87 billion.

Other top foreign holders of Treasury securities include Canada, @ $338 billion, a 36.9% increase year over year, and Taiwan, which increased holdings 5.3% to $257 billion.

Japan holds $1.5 trillion, a 2.2% increase from a year ago, but the key data point is China and Hong Kong combined, which hold 9.1% less Treasuries, year over year, worth $992 billion.

This compares to more than $1.4 trillion between 2012 and 2017.

Members of the BRICS have been pushing for de-dollarization, so it was no surprise to see China’s Treasury holdings take a hit. Fellow BRIC member India’s lessened by 2.2% to $234 billion. Brazil’s were down 2.7% to $224 billion, about one-third of their 2018 peak.

Business Insider reported China unloaded a record volume of bonds in the first quarter, selling $53.3B worth of US Treasury and agency bonds. The country dumped $300B between 2021 and mid-2023.

Conclusion

Of course, I see the BRICS’ reticence regarding Treasury-buying as part of a broader movement to diversify global finance, and chip away at dollar dominance. This is only likely to continue, imo, as the US debt situation continues to worsen, and credit agencies come a-knockin’.

But I also see recent buying by Canada, Europe and the world’s financial centers as a way of propping up the US dollar.

Obviously more countries are buying US debt than are selling it, because if it was the other way around, the dollar would be dropping.

“When the dollar strengthens, it means more foreign money is flowing into the U.S. than the other way around,” confirms Rob Haworth, senior investment strategy director at U.S. Bank Wealth Management.

I also wouldn’t be surprised if there is a concerted effort on the part of America’s allies to avoid hundreds of billions of dollars from the sale of Treasuries by countries like China, India and Brazil because inflation would be soaring as all those dollars coming ‘home to roost’ would be extremely inflationary – one of the most inflationary things that could happen. But inflation is slowing.

Instead, Western countries are sopping up these dollars and buying T-bills, keeping the dollar strong and inflation at bay.

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

*********