Why the Federal Reserve Pays Interest to Your Bank—and You Get Nothing

I think the average American does not know that the US Federal Reserve currently pays 4.90% interest to banks on people’s checking and savings deposits—this includes the cash in the drawer! I just checked my personal savings account and I am currently getting .01% on my savings account. My hard-earned money is earning my bank 4.89% interest—this is not right. How much is your bank making off your deposits?

Additionally, did you know that your deposits no longer get loaned out to small businesses and consumers the way they used to? It is true, part of your deposits at the bank partially fund government deficit spending rather than going to private loans for small businesses and individuals. Americans are partially funding government spending with their checking and savings deposits! If you’re upset about this, you are not alone. The recent inflation and growing debt have me upset and that prompted this article.

Customer checking account deposits are mostly interest free, but The Federal Reserve Bank of the US (Fed) pays banks interest on a fraction of those deposits. For example, if you have $1,000 in your checking account earning 0%, the bank may have $600 of your deposit on deposit with the Fed earning 4.9% as of April 2023.

The Fed is now more than ever considered to be the “banker’s bank.”

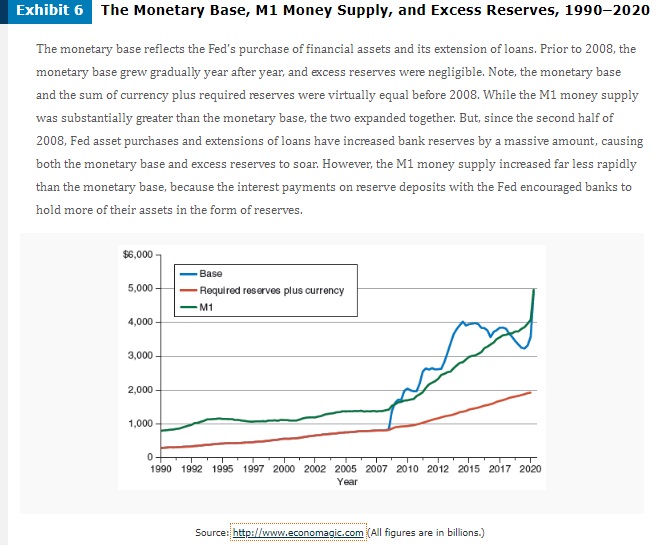

In 1913 when the Fed was created, banks were required to deposit a fraction of their customer’s deposits with the Fed. The intent of the law was to give confidence to depositors that the bank would keep a reasonable amount of their money on hand and could not loan out all the depositor’s money. Historically, banks earn a profit by making loans to individuals and businesses at interest rates higher than what they pay on customer’s checking and savings accounts. This fundamentally changed in 2008 when deposits began partially funding government spending. COVID policy spending has continued to dramatically change how the government uses checking and savings accounts.

In 1933, FDIC insurance was added to further increase bank customer confidence with deposits being fully insured up to a maximum level (technically $250,000 today, but apparently unlimited for customers at some banks in 2023).

Prior to 2008, banks had an incentive to loan out 90 percent of your deposits (called excess reserves), about 10 percent was required to not be lent out or invested. For example, the required reserve ratio historically was about .10 (10%) and this meant that to make a profit banks would loan out or invest 90 percent of customer deposits. So, if you deposited $1,000, $100 would be kept either at the bank itself or it would be deposited at the Fed. The bank could then lend out the other $900 and make interest on it. The system works so long as the amount of vault cash on hand services day-to-day turnover of customer’s new deposits and withdrawals.

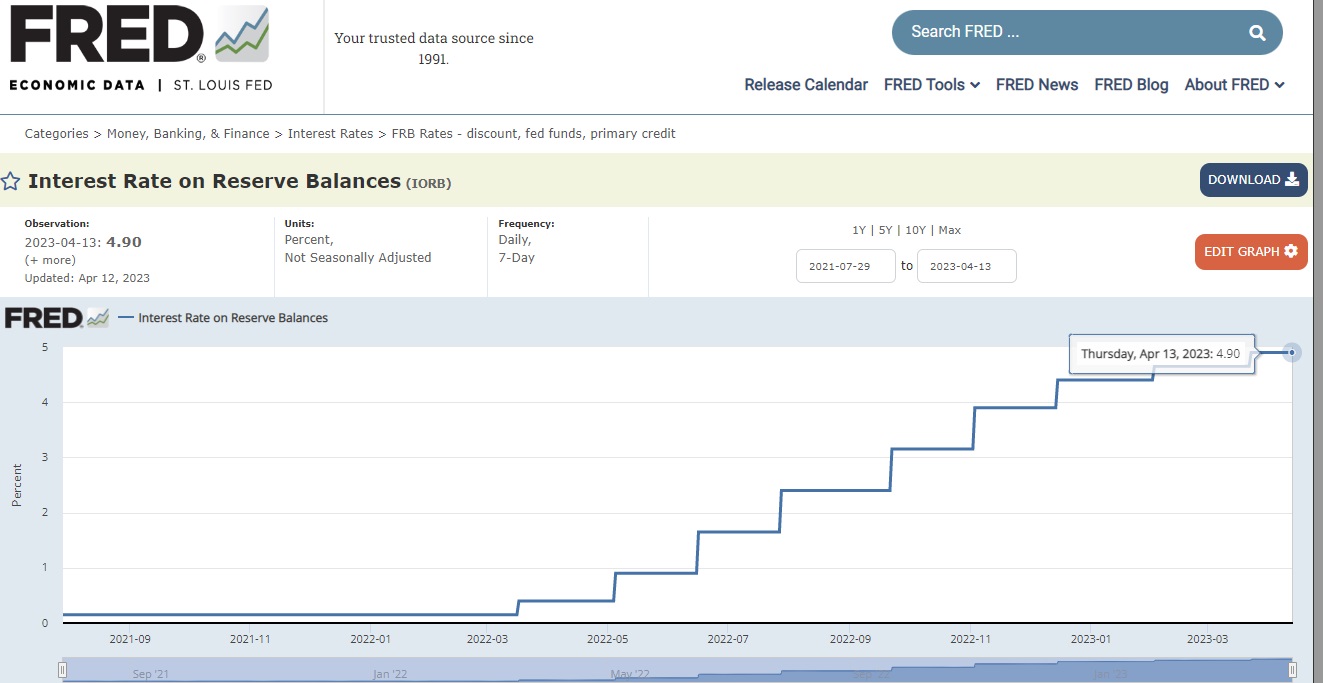

After the financial crisis, the Fed added a new tool to control the supply of money. The Fed now pays interest to banks for money they do not lend out to private individuals and businesses. Economists call this tool interest on reserves. Banks now have an incentive to keep deposits with the Fed instead of lending them out to individuals and businesses because the deposits at the Fed pay risk-free interest of 4.9% as of April 2023. The bank’s “investment” is risk-free because the Fed can always print money to pay the interest to the bank (the bank can withdraw its deposit at the Fed anytime, and it is impossible for the Fed to default on its payment—they make the money!)

If individuals and businesses are willing to pay interest rates higher than what the Fed pays, there is still incentive to loan money out. However, interest earned from the Fed is risk-free while other loans have default risk with them. Additionally, deposits at the Fed are easy to turn into vault cash compared to waiting for customer payments on 5 to 10-year loans from businesses and individuals.

So, what’s the issue with this new interest on reserves tool?

Banks Get a Risk-Free Spread on My Money?

Concern #1: Is it fair that banks are earning a risk-free spread on Americans’ deposits at banks? No! On April 21, the interest on reserves was 4.90 percent while my savings account interest rate was .01 percent and 0 percent on my checking account! I called my bank to get a quote on some other rates. A premium saving account with a $10,000 minimum balance paid .03 percent—three times the simple savings! A 9-month Certificate of Deposit of $25,000 paid 3.25% which gives my bank a risk-free spread of 1.65%—I commit to 9 months, but they can withdraw their funds from the Fed anytime. Prior to 2008, banks would take on some risk to justify their profit (or loss) on reserves and now that is gone. The dramatic increase in ‘Reserve Balances’ by banks show that they love having some risk-free money as part of their portfolio.

When the interest on reserves was low along with all other deposit rates, this tool seemed insignificant and therefore issues of fairness were not as apparent. From 2008-2022, the interest on reserves was never higher than 2.4 percent and most of that time it was under 1 percent. This is new territory for the Fed at 4.9 percent, and I think it exposes problems with the policy.

Why is the Fed facilitating a risk-free investment for the bank and risk-free interest rate for the depositor through FDIC insurance? It gives the Fed access to cheap funds through your deposits for the national debt.

The interest on reserves obscures the Fed’s facilitation of financing the federal government’s debt. Don’t we have a right to know how the government funds government spending? Yes! It would be more obvious if they would just raise enough taxes to pay for spending, but these creative funding streams don’t seem right to me and foster national debt growth—smoke and mirrors diminish our right to transparency of how our dollars are spent.

Since the Fed sets the interest rate on reserves, it can always keep that rate high enough to leverage low/no interest checking/savings accounts as a source of government funding, effectively keeping this money out of private sector investments—a step toward abuse of power.

The government sells bonds to pay for spending it has not collected enough taxes for. Had the Fed not purchased the vast majority of the $4 trillion government bonds following Covid-19, the interest rates in the loanable funds market would have increased. Just like a car auction, prices go up when there are more bidders in the room. The price of borrowing money is the interest rate and if the government had entered the bond market competing with other private borrowers, interest rates would rise just like car prices would at the auction. Instead, the government had the Fed as its private buyer, and therefore the government did not have to compete in the bond market—what a deal.

Fearing recession from Covid and Covid policy, the Fed pursued “easy money” policy by purchasing the “Covid bonds” and apparently hoped inflation would not be too bad despite this historic increase in the money supply—they were wrong. The part of the story I am adding is that the interest on reserves policy redirected depositors’ money from private investment and borrowing and into government borrowing.

The interest on reserves caused Americans’ deposits at banks to effectively subsidize government debt. Perhaps if policymakers’ actions were subject to market discipline, we would not have some of the inflation problems we are now experiencing. The Fed is now using “hard money” policy and driving up interest rates to fend off inflation they created. How much better would the average American be if the Fed had not purchased all those Covid bonds? Much better! There are millions of dollars more being spent at the grocery store with the inflation we are experiencing now because of Fed policy.

My Deposits Where?

Concern #2: Is it fair for the government to diminish private borrowing with government borrowing? Not to me. I would rather see banks choose private borrowers rather than government borrowing.

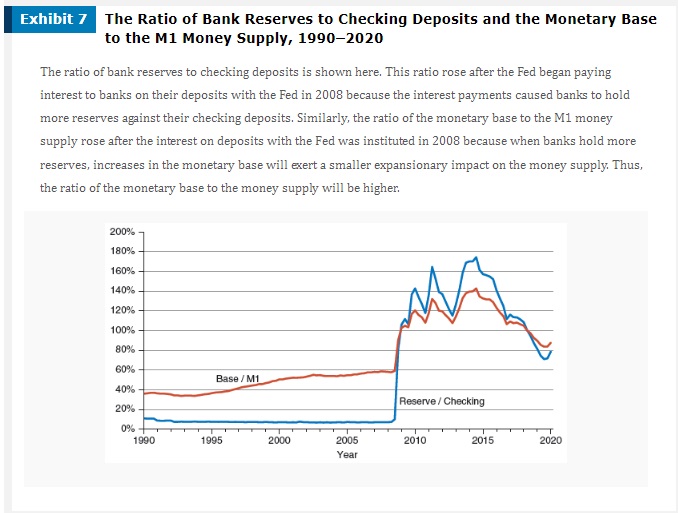

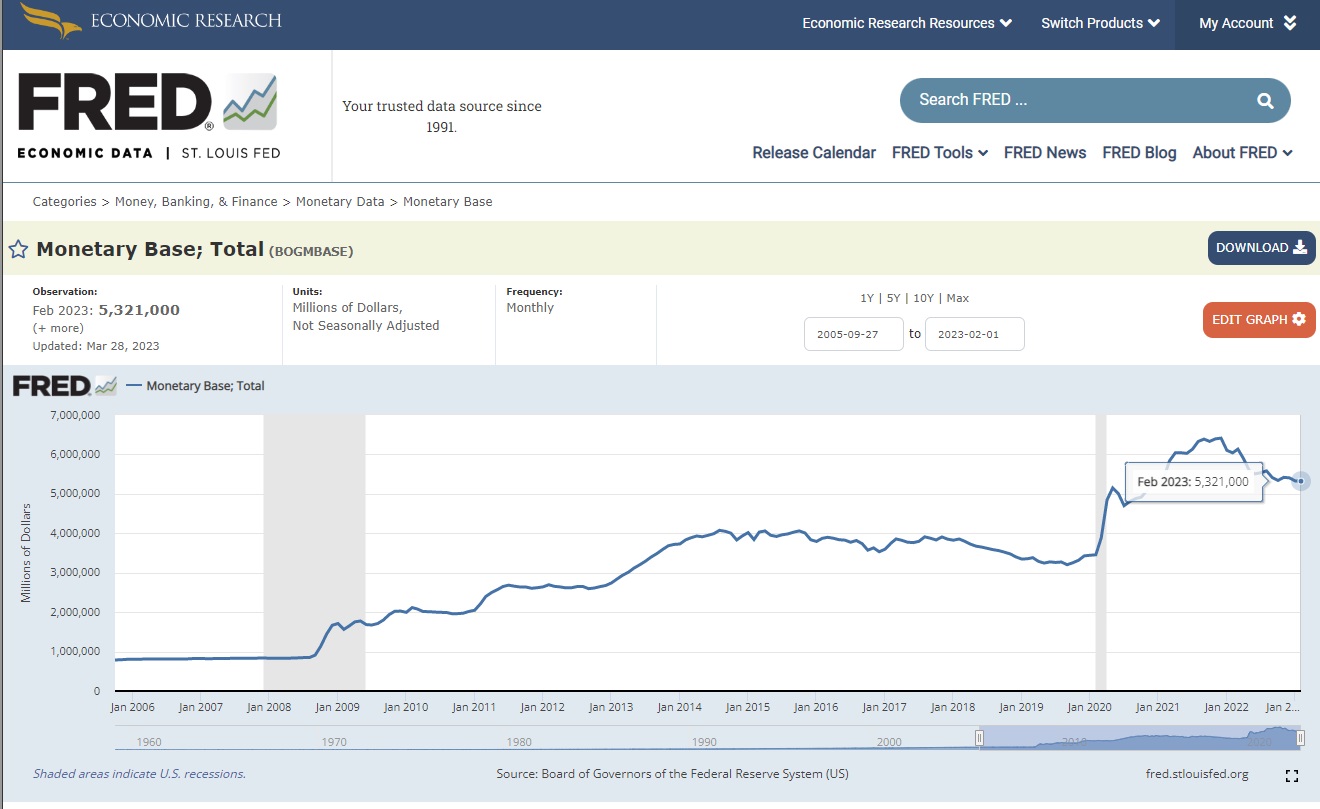

Prior to 2008, the Monetary Base (currency in circulation plus bank reserves at Fed plus vault cash) was virtually equal to “required reserves plus currency.” By applying the old policy average 10 percent of required reserves to 2023 data, the required reserves under the old policy would be $1.7T (10%*$17T) leaving $15.3T to be loaned out or invested by banks. The current Monetary Base is $5.3T. This implies a difference of $3.6T of customer bank deposits funding government debt and not making its way to private sector investment and borrowing as it has in the past. Our 2022 income for the nation was about $26T!

The rebuttals from policymakers and bureaucrats I expect from calling attention to these two concerns are this. “Paying interest on reserves allows the Fed to better manage bank reserves and control the supply of money to better manage recessions, unemployment and inflation.” They might also point out that “all profit by the Fed each year is turned over to the US Treasury, so this new structure does not matter.” It does matter when there is less private borrowing. Interest on reserves policy allows the government to borrow at cheaper rates, which in turn leads to more borrowing—the law of demand. Our current situation of funding deficits through this new channel has now shed light on the hubris of those in control—they cannot manage the economy as well as they think they can (Hayek’s Fatal Conceit).

It is clear from the outcomes of these recent Fed policies that our country’s deposits are better off in the hands of thousands of competitive banks making choices about who to make loans to and what investments to make. Channeling our deposits into a few decision makers at the Fed will lead to big problems like the high inflation we are experiencing now. While thousands of banks will also make errors here and there, the consequences will only be on those who made the bad choice, those errors will not cause systemic hardship of general inflation for the average American.

I recommend abolishing the interest on reserves policy so that private checking and savings accounts get directed to private investments as originally intended in entrepreneurial America. If you think increased government spending using deficits is bad, then using the tool of interest on reserves to fund those deficits only makes it worse. To have the US Federal Reserve pay private banks to use depositors’ money in order to continue buying US government bonds that increase the national debt is a use of creative financing that runs contrary to freedom and free enterprise.

Courtesy of Fee.org

*********