Yield Curve: Slowly I Toined…

The 10yr-2yr yield curve has un-inverted; yet in the media? Crickets.

Slowly I toined [cue Brooklyn accent], step by step…

The 10yr-2yr yield curve un-inverted last week, turning from inversion to steepening after a long creep from extreme inversion.

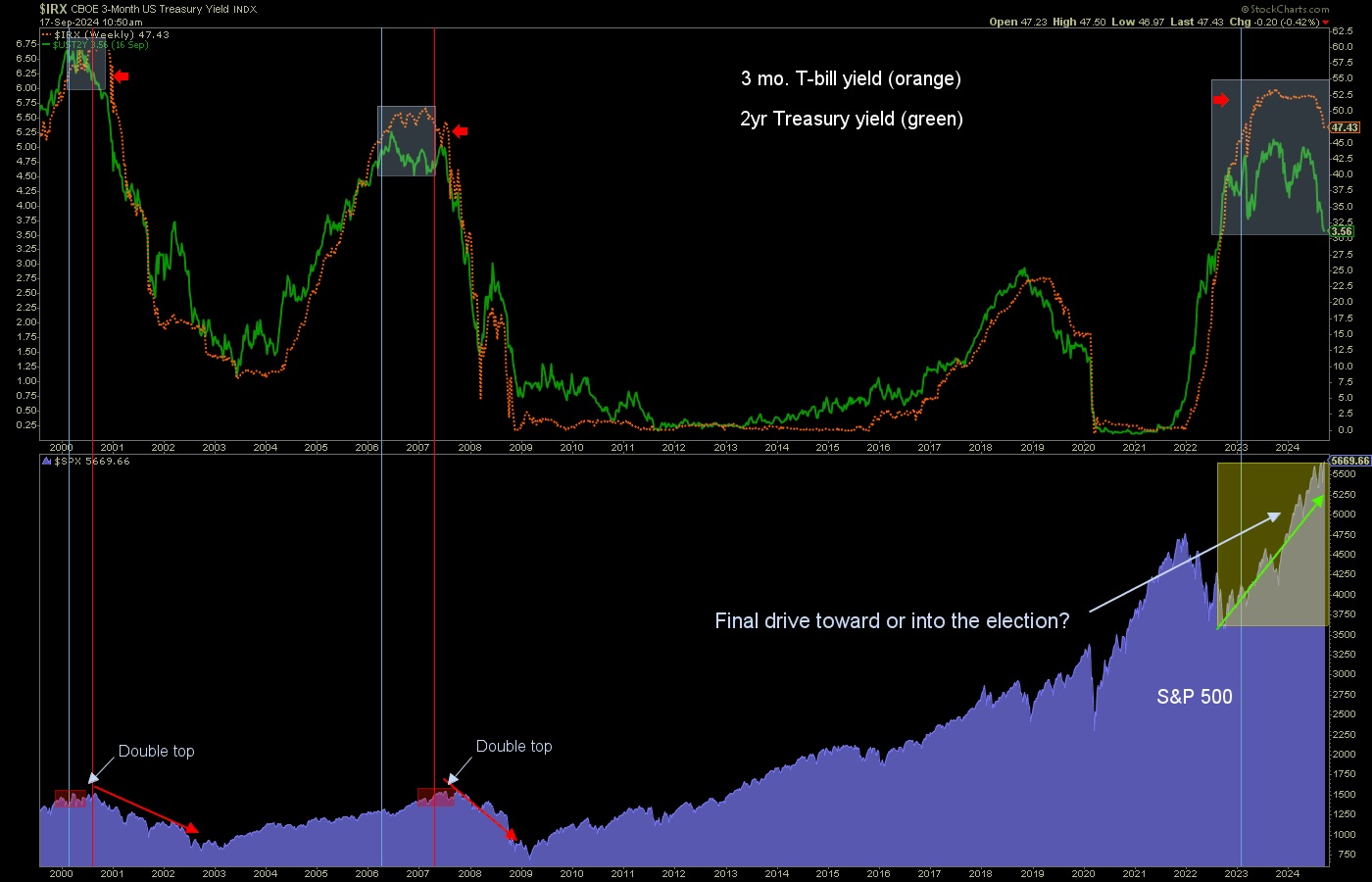

First I’d like to clear something up after a mild debate with a fund manager friend of mine. He questioned why I don’t use the 10yr and T-bill (a tighter Fed Funds proxy) rather than the 10 and the 2yr. My answer is that we are looking for forward direction, and so I want to view the thing (2yr yield) that is leading the T-bill (and thus, the Fed), not the tardy Fed itself. I want to see where the Fed is being compelled to go, not where it has squatted to this point. Look no further than the interminable “transitory inflation” stance the Fed asked us to buy into before they finally got off their dovish ass and began to fight the inflation problem they primarily enabled, if not outright manufactured.

Never trust an over-schooled egghead. That’s my motto.

Back to the big picture macro chart we’ve been monitoring over the last couple of years, you can see the progress the macro is making in compelling our eggheaded meeting-goers to finally spring into action. The 2yr yield (green) divergence has finally jerked the T-bill into a downturn, which will… voila! Jerk the Fed into action (of some kind) tomorrow. It’s not rocket science, but to automatons and robots following mainstream economists, it may appear to be.

This chart is history, and I have little reason to think history will not play out bearish as it did in 2000 and 2007, under similar indicator circumstances. Today, SPX is putting on a whopper of a FOMO for those not aware or not caring about the indicators and internals of the markets. Greed is always punished, sooner or later. So is ignorance.

Back on theme, the 10-2 yield curve has un-inverted under disinflationary pressure of declining nominal yields. Just as expected and projected several times in advance, publicly, and consistently in NFTRH. Slowly toins the curve after its steepening tick to de-inversion.

It is funny how the media are not making any sort of deal about this after sounding all kinds of recession alarms in 2022 and 2023 as the inversion took hold and dug deep. Now they go quiet? Well yes, they are the media, after all. They are not going to get you a straight deal, market management wise. They harvest eyeballs for ad revenue and for whatever reason, the “INVERSION” tout is the eyeball grabber.

The straight deal is that a curve flattening to inversion tends to run with an economic boom and a steepener tends to trigger an economic bust. T-minus…

By now the media have moved on from negativity about the inversion to AI promo, to Trump, to Harris, to who’s better (or worse) for markets, to market rotations and any other easy to comprehend (selling eyeballs, after all) concepts they can get their hands on to try to spellbind you. The media and its advertisers think you are too unsophisticated to grasp ideas about what’s going on beneath the surface of markets and the economy; what may be directing them. If you read and agreed with me at the time, you did not bite on the yield curve inversion hysteria. Now? A different story to play out in the months ahead. You are free to bite or deny at will.

Our original view was and still is “to or through the election” for the intact macro and bull market. If that holds true (in the face of very concerning indicators to the contrary) the question then becomes how far “through” the election? It’s a good bet that fiscal policy (including unprecedented government hiring) enacted by government this election year will relax at best or ramp hard down at worst when the election is either secured and won, or lost, as the case may be.

For “best of breed” top down analysis of all major markets, subscribe to NFTRH Premium, which includes an in-depth weekly market report, detailed market updates and NFTRH+ dynamic updates and chart/trade setup ideas. Subscribe by Credit Card or PayPal using a link on the right sidebar (if using a mobile device you may need to scroll down) or see all options and more info. Keep up to date with actionable public content at NFTRH.com by using the email form on the right sidebar. Follow via Twitter@NFTRHgt.

********

More from Gold-Eagle