12 Reasons Why Ritholtz and Many Experts Are Mistaken On Gold

Being involved in the fairly niche business of an international gold brokerage for nearly 12 years now, we find ourselves continuously engaged in conversation with people who demonstrate an incredible lack of understanding of the function of gold and the importance of gold as a DIVERSIFICATION and as a SAFE HAVEN asset.

This lack of understanding is not confined to the public…but also prevalent with some financial experts. One example of this is one of the more vocal anti-gold experts in recent months – leading Bloomberg columnist Barry Ritholtz.

This lack of understanding results in many investors being very exposed and at risk of financial losses due to their significant over exposure to paper assets and fiat digital currencies and complete lack of any allocation to gold whatsoever.

These experts are highly intelligent people. As are many in the public and yet the concept of diversifying and having an allocation to gold is utterly foreign to them.

The public have little terms of reference except for movies such as Goldfinger and fairytales about Leprechauns and crocks of gold. Indeed, their primary reference point is often jewellery, wedding rings and of course the recent ‘cash for gold’ phenomenon.

They have no understanding of the central role gold plays in macro-economics, geopolitics and of course monetarily.

They have no knowledge of the fact that gold has protected people throughout history from financial and economic crashes and from currency devaluations. The significant body of academic research on gold showing it to be a hedging instrument and a safe haven asset is ignored and unknown.

We find ourselves constantly confronted by the same set of ill-informed opinions on gold.

Many of these misconceptions were encapsulated in a 2013 article by Barry Ritholtz, with the peculiar title “12 Rules of Goldbuggery”.

Oddly, we happen to agree with a lot of what Ritholtz has to say. There are some – among the diverse range of people online who promote ownership of physical bullion coins and bars – whose enthusiasm for the metal can border on religious zeal. They are a minority.

At the same time we feel that Ritholtz’s article was somewhat disingenuous. It was unbalanced and simplistically denigrates gold ownership – ignoring academic research and indeed history and the experience of recent years – the U.S. and Euro zone debt crisis, Lehman Brothers etc.

The article was very widely disseminated and will have discouraged many investors from allocating to gold in a properly balanced portfolio.

The immediate problem with critiquing the disparaging remarks in “Goldbuggery” is that Ritholtz doesn’t approach his distaste for gold head-on. Instead he puts words in the mouth of apparent “gold bugs”. He therefore avoids making statements he may later regret.

Certainly, some of these views are held by some gold buyers but, in our experience with our clients, they are by no means the mainstream view in the gold community.

It is worth noting that there is no asset-class other than gold where its proponents have their own derogatory classification. We are labelled “gold bugs”, but there are no “stock-roaches” or “preying-bankers.” Let alone “paper bugs”, “dollar bugs,” “euro bugs” or heaven forfend “banker bugs.”

One has to ask – why the silly name calling regarding gold. Why use a pejorative and derogatory term for those who own physical gold to protect themselves from market turmoil and currency devaluations? It suggests an anti gold agenda or at least anti gold beliefs.

Let us now look at Ritholtz’s Twelve Rules of Goldbuggery. We will look at each of these contentions and deconstruct them one by one.

1.Gold is Currency

That gold is a form of currency and money is self evident. If it were not, central banks, particularly in Asia, would not be buying vast amounts of it and Western central banks would not continue to be holding vast amounts of gold reserves.

When the U.S. shut Iran out of the SWIFT system Iran began successfully trading oil for gold. In extremis, at this time and place in history, gold is the ultimate form of payment as Alan Greenspan recently pointed out.

Ritholtz suggests that proponents of gold ownership view it, irrationally, as a permanent store of value because it was declared so in Greece 2700 years ago and “it shall ever be thus.”

Placing monetary value in a piece of metal is an abstraction, we agree. However, in practical terms there is no company, currency or empire that has outlived the value that man has placed on gold.

Maybe the time will come when humankind devise a more sophisticated means of exchange but in the here and now gold is money. In the not unlikely event of a monetary crisis, with currencies based on confidence alone today, gold – which has industrial applications and psychological appeal – will again retain value and outperform.

The ECB’s Mario Draghi said gold is a monetary “reserve of safety”.

2. The price of gold cannot fall, it can only be manipulated lower.

Like all currencies gold fluctuates in value relative to other currencies. No rational person would ever state otherwise. At the same time there is mounting evidence that violent downward swings in the price of gold have been orchestrated by large banks.

This is achieved by dumping large contracts for gold which they are not in physical possession of (naked short selling) onto the market during quiet periods when there are few buyers to support the price.

In fairness, Ritholtz wrote his article before it was exposed last year that banks were rigging practically every market on the planet and continue to do so.

This week it has emerged an astounding ten of the major banks may be directly involved in rigging the gold-price are now being investigated by the Department of Justice in the US and by the CFTC.

Under investigation are the household names of International banking including Barclays PLC, Deutsche Bank AG, Credit Suisse Group AG, UBS and Societe General. Of course no banking scandal is complete without JP Morgan Chase & Co. and Goldman Sachs Group Inc.

3. If the price of gold is rising, it is doing so despite enormous and desperate efforts by manipulators to prevent the rise

This is possible. As is the possibility of a tactical retreat whereby banks aware that physical demand may overwhelm their manipulation of gold and silver prices decide to gradually allow prices to rise, hoping that this will dampen physical demand and they can cap prices at higher prices.

Ultimately, the price of most things will be dictated by the forces of supply and demand of the nearly 7 billion people on the planet. Banks can prevent price discovery in the short term but in the long term, the small physical gold market will dictate the price.

4. The world MUST return to the Gold Standard one day

Ritholtz fourth rule – that the world “MUST” return to the gold standard one day – is also not a view widely held in the gold community.

Certainly, there is a potential for such – and some would suggest a necessity – but nobody knows what political action will be taken in different countries if confidence is finally lost in the world’s erstwhile reserve currency – the dollar.

If China and the Eurasian Economic Union headed by Russia choose to partially back their currencies with gold, which seems possible, given the huge volumes they have been accumulating, they could potentially challenge the dollar’s role as reserve currency.

In such a case it is not unreasonable to suggest that the U.S. might be forced to back it’s enormous debt with the 8,500 tonnes of gold it claims to have. In such a case the very high prices of gold that Ritholtz ridicules – such as $15,000 – would not be so completely outlandish – although there are many more conservative estimates of gold over $5,000 per ounce.

Of course the purchasing power of those dollars would be greatly impaired. This is precisely why we advise clients to own gold. It is not necessarily for building wealth but for protecting it.

5. Central Bankers are printing money relentlessly, and this can only drive Gold prices higher

This is true and to suggest otherwise is misguided.

Central banks are printing money hand over fist. This will inevitably destroy the purchasing power of currencies in the long term. There is no precedent in history for the scale of the currency debasement of central banks in the past fifteen years.

Whether or not the central bankers have finally, this time, perfected the alchemy of wealth creation through money printing is yet to be seen. Prudence would dictate that one takes measures to hedge against the typical outcome of such monetary incontinence throughout history. That is, uncontrollably high inflation. Historically gold has behaved as such a hedge.

Ritzholtz says that “gold-bugs” try to ignore the fact that gold had not gone markedly higher in the two year period before he wrote his piece despite massive QE.

Well, as Alan Greenspan explained in his address to the CFR last year, QE had not caused the desired inflation because all the cash got swallowed up in the stock markets or was loaned abroad causing high inflation in emerging markets.

Should the stock market bubble burst or should emerging markets shed their dollars, a wave of dollars will hit the real economy in the U.S. engendering very high inflation. Whether gold performs its traditional function in this scenario remains to be seen but in the absence of any other alternative we are confident that it would.

6. Gold works whether the economy is good or bad

The purpose of owning gold is to hedge risk and protect against uncertainty. When things go very bad it rises as one’s other assets fall, cancelling or at least reducing the loss. Ritholtz mockingly refers to it as “a trade that never fails!” Owners of physical gold do not view gold this way. They do not speculate with it. They hold it as an insurance policy that has no counter-party risk.

Therefore, yes if owned as financial insurance, gold like insurance, is useful and “works whether the economy is good or bad.”

Generally, gold performs better when the economy is bad. However, we live in a very uncertain world and no one can protect the economic cycle hence the vital importance of DIVERSIFICATION.

7. Gold will survive after the world economy crumbles

The assertion is that if the world economy collapses, we would be in a post-apocalyptic ‘Mad Max’ type scenario. This is childish nonsense. Industrial, technological and agricultural capacities would remain intact for the most part.

Social chaos and war may ensue during the transition with some resulting destruction but by and large trade would continue in most parts of the world.

The economic catalyst for a collapse in the global economy, should it happen in these times, would likely be the failure of paper currencies due to gargantuan unpayable debt.

In such a climate it is reasonable to suggest that gold could be the last man standing. It may not be held in great esteem in the West but in the East, it certainly is.

In the event of a currency collapse exporters will expect something of value in exchange for their produce. When faced with a choice between unlimited paper and digital fiat currencies with no tangible backing on one hand and gold-backed Eurasian or Chinese money on the other, it is reasonable to speculate that they will choose the latter.

8. Never admit that Gold is essentially a sucker’s bet

Ritholtz lists periods when gold has not performed well in dollar terms, choosing to ignore the intervening periods in which it thrived. Data mining is such an easy thing to do. One could pull similar rabbits from a hat to disparage the Dow Jones and S&P and other benchmarks.

The difference is that owners of physical gold still owned something at the end of a bad period whereas owners of stocks and shares of many companies lost everything.

Also gold was money throughout many of the periods cited as dollars were backed by gold. Gold has a fixed price of $20 per ounce and then $25 per ounce and it was not a freely traded market. Therefore it is unfair and disingenuous to compare it to stocks, traded markets or other speculative ‘bets’.

9. Gold is a rejection of government, and their control of fiat money and finance

This is another sweeping generalisation. Many of our clients believe this. Most don’t.

Most do not ‘reject’. Many are concerned.

Owning gold needs no ideological basis. True, it can protect one from the stupidity of the types of politician and policy maker who have destroyed economies throughout history.

Owning gold as protection from government stupidity and corruption is not a rejection of government per se.

The wise Founding Fathers of the U.S. were adamant that gold and silver – and nothing else – were money. So much so that they had it written into the constitution.

Did these “goldbugs” reject the concept of government? Or rather did they see the benefit of having monetary controls on bankers, politicians and governments?

10. All Gold discussions must contain ominous macro forecasts

This is another sweeping generalisation. Some gold analysts make ominous forecasts. Others do not. Some stock and bond market analysts make ominous forecasts. Others do not.

We generally do not make forecasts. We address macro-economic and geopolitical facts and highlight the unavoidable conclusion that there is very high, perhaps unprecedented economic and geopolitical risk in the world today for which people should be prepared.

Ritholtz suggests that gold analysts “avoid empirical data at all costs.” This is nonsense. We, and many of our competitors in the gold business, consistently use important data, much of which is studiously ignored by many bank and other economists when they conflict with the official narrative of “green shoots” of recovery.

11. Gold is always rallying in one currency or another

This is a statement of fact – especially in this era of currency devaluations and currency wars.

Obviously, the price of gold in another currency has no immediate bearing on the price of gold in an investor’s own currency.

However, it is highly relevant in demonstrating how owners of gold manage to preserve some of their wealth when the economy of the country in which they live is mismanaged and has an economic and or monetary crisis.

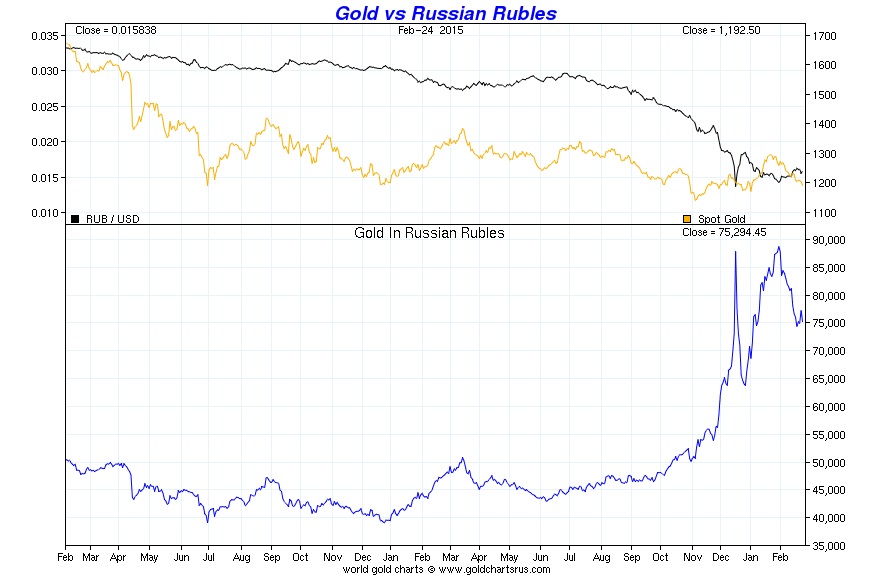

Gold priced in roubles rose 75% in 2014, during the Russian economic crisis. This aptly demonstrates the role gold plays in economic crises and it is relevant information in highlighting the case for owning gold.

Gold is again acting as a hedge against currency weakness and the ongoing devaluation of currencies as stealth currency wars continue.

The focus on gold solely in dollar terms is misleading. It shows a peculiarly dollar centric way of looking at the world. It is important for investors in the UK, EU, Japan and elsewhere to always consider performance in local currency terms and top not lose sight of the fact that all fiat currencies are being devalued today – including the dollar.

12. China & India know the value of Gold; The Western world does not

This is true too. Go to India, China and Asia and talk to ordinary people and you will quickly realise this.

The people of China and India live in societies where wealth has been periodically extracted from them through currency devaluations. Therefore, they have a natural affinity for gold as insurance and as a store of wealth.

It is not a matter of them “knowing” the value of gold. What is important is that actual direct experience has caused a mass of people – that compose one third of the entire population of the globe – to value gold.

Gold will remain a store of value for most Asians for the foreseeable future, thus supporting the price that people are likely to pay for it – especially in a crisis.

Western populations, except perhaps for Germans, are not prepared for a potential monetary crisis and severe inflation. They do not understand the potential for even deeper currency devaluations and the role that gold would play protecting their wealth in such a scenario.

Conclusion

This concludes our reply to Ritholtz’s 12 rules. As you can see, they are misleading and misrepresent the case for owning gold.

Gold has proven itself a safe haven both historically and again in recent years. There is now a large body of academic and independent research showing gold is a safe haven asset. Numerous academic studies have proved gold’s importance in investment and pension portfolios – for both enhancing returns but more importantly reducing risk.

The importance of owning gold in a properly diversified portfolio has been shown in studies and academic papers by numerous academics and by Mercer Consulting, New Asset Frontiers and the asset allocation specialist, Ibbotson.

This is not an attack piece on Ritholtz. As we said at the outset we share his views on many matters financially.

Rather it is an attempt to try and engender a more fair, balanced, nuanced and enlightened debate about gold as an asset and a safe haven.

As a frequent contributor to Bloomberg, I would welcome the opportunity to debate this with Barry.

What say you @ritholtz ? : )

Click here for Gold Is A Safe Haven Asset

MARKET UPDATE

Today’s AM fix was USD 1,206.50, EUR 1,062.06 and GBP 777.99 per ounce.

Yesterday’s AM fix was USD 1,195.50, EUR 1,057.97 and GBP 774.59 per ounce.

Gold fell 0.16% percent or $1.90 and closed at $1,200.20 an ounce on yesterday, while silver slipped 0.43% percent or $0.07 closing at $16.25 an ounce.

Gold in US Dollars – 5 Days (GoldCore)

Gold jumped 1 percent in late Asian trading after falling to a seven-week low in the prior session, as Fed Chair Janet Yellen’s dovish tone hinted at flexibility in raising U.S. interest rates – meaning she is happy to hold them near zero for as long as possible.

The timetable for the Fed’s interest rate hike is now perhaps June through September – if even that – ZIRP looks here to stay.

Yellen’s comments sent the U.S. dollar lower, and stoked a rally in precious metals with silver rising over 3 percent and palladium reaching a six week high.

China’s return from its Lunar New Year break also strengthened gold prices, with premiums on the Shanghai Gold Exchange (SGE) rising to $5-$6 an ounce over global spot prices, from $3-$4 before the New Year’s holiday.

In late morning trading, gold is $1,208.61 up 0.31%, silver is $16.54 up 0.77% and platinum is $1,169.20 up 0.22 %.

********

Courtesy of http://www.goldcore.com

Mark O'Byrne is executive and research director of www.GoldCore.com which he founded in 2003. GoldCore have become one of the leading gold brokers in the world and have over 4,000 clients in over 40 countries and with over $200 million in assets under management and storage.We offer mass affluent, HNW, UHNW and institutional investors including family offices, gold, silver, platinum and palladium bullion in London, Zurich, Singapore, Hong Kong, Dubai and Perth.

Mark O'Byrne is executive and research director of www.GoldCore.com which he founded in 2003. GoldCore have become one of the leading gold brokers in the world and have over 4,000 clients in over 40 countries and with over $200 million in assets under management and storage.We offer mass affluent, HNW, UHNW and institutional investors including family offices, gold, silver, platinum and palladium bullion in London, Zurich, Singapore, Hong Kong, Dubai and Perth.