The Mother Of All Margin Calls!

share

share

share

share

share

share

share

share

share

share

The chart in question shows three very distinctive spikes, the first was Sept. of 2008, again in 2011 and the current spike. It is Dave’s contention that something behind the scenes has or is blowing up financially.

Let me explain what I believe is happening, I do not disagree with his theory but I think he may have stopped just one step short of the full story. By adding one more chart in a moment, I’ll try to explain. Please read the above article as it is a good explanation of “reverse repurchase agreements” and saves me the need for a long winded rehash.

For years I have described the current financial situation as a “giant margin call” waiting to happen. The derivatives market is a zero sum game where someone wins and someone loses, the danger of course is someone losing so badly they become insolvent and cannot make payment to the “winner” …which would make all parties a loser in the game. This is the fear, the derivatives chain breaks somewhere along the way and creates a domino effect both upstream and downstream causing the entire credit system to lock up.

Think about what has happened over just the last six months alone. We have seen unprecedented FOREX movements. The dollar has strengthened close to 30% over this timeframe while oil has dropped about 50%. The cross between the euro and the Swiss franc saw an almost 30% move in less than 10 minutes one Monday morning in January. There have been some very big gains AND some very big losses which would explain the need for “more collateral” which is exactly what these reverse repo’s provide.

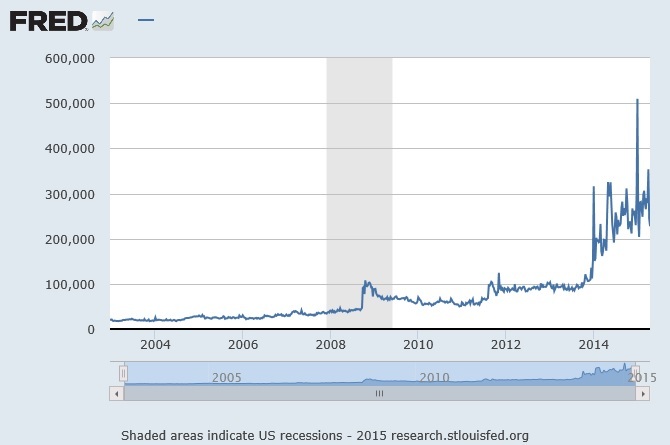

Please look at the following chart:

I believe this is “the rest of the story” as I mentioned above. You can clearly see the spikes in 2008, 2011 and again currently but “this time is different”. It is different because of both size and the long lasting duration! The first chart that Dave put out on Friday was of RRP’s with “Foreign Official and Institutional Accounts” whereas the chart you just looked at are “ALL” RRP’s.

It is my belief the first chart’s movements are a function primarily of international FOREX movements and represents “collateral demand” from the likes of Deutshebank, SocGen, Barclays etc. …AND from The Bank of England, the ECB and other central banks. The second chart is of ALL players, not just foreign. This chart in my opinion is “how” the Fed has aided and abetted the system as a whole in “hiding” the losses from derivatives! The Fed places collateral into the system which gets lent out over and over (rehypothecated) many times and “pledged” as collateral by the loser in derivatives trades… thus the system continues “unbroken” because the collateral is put up to meet the margin calls.

Do you see? For well over a year I have wondered and even written in disbelief and amazement that no one ever admits to any large losses when in fact there had to be losses well into the multiple $ trillions! Think about it, there are almost $10 trillion worth of “dollar derivatives” outstanding, a 30% move means someone won and someone else lost about $3 trillion. I don’t know of any firms that could lose even 5% of this and remain solvent, do you? And this is just “dollars”, not oil, not interest rates, not equities, not iron ore, copper, gold or anything else!

If you see the buildup of RRP’s over the last year+, this I believe is how the margin calls have been met and the losses hidden …but is it even legal? In a technical and practical sense, no it is not. However, from a practical sense, if this is what is being done then we now know how no one has been declared a loser and no one has had to “book” their losses. The margin calls have been met, the positions stay open and no one is the wiser right? I do want to point out that under the rule of law, if the Fed “knows” this, it is without a doubt a criminal act. If they are doing business with bankrupt institutions, one which they know or should have knowledge of as being bankrupt, the Fed is flat out fraudulently and blatantly breaking all banking laws on the planet.

Going just a step further, if this is the case, what does it say about the Fed’s own balance sheet? If they are doing swaps or RRP’s with bankrupt institutions, will the Fed ever get their collateral back? As Dave Kranzler so aptly tied together, this is why the “failures to deliver” have spiked. The collateral which was originally lent out has been re lent 10 times more, or even 100 times more, who knows?

Please walk away from reading this piece with one understanding, the chart above is telling you something very big has changed and been changing for over a year. I believe it shows the system is in and has been fraudulently meeting a systemic margin call. Maybe I am wrong but I wouldn’t bet on it. The chart does however give you proof beyond any doubt that “stress” of some sort has been and is building up “somewhere”. The stress is now multiples of what we saw in late 2008 …when we were only hours from the system seizing up in a giant meltdown.

I bounced this theory off of Jim Sinclair over the weekend and received a short but very enlightening reply. He said “The concept is correct. We have another OTC derivative explosion at hand but no practical way to expand liquidity. Bad derivatives never die, they just get larger”. Think about what Jim is saying here, we again have an autumn of 2008 event triggering …only bigger! And no way to actually meet the margin calls. Each episode of QE was used to meet the margin calls and hide the losses. Each one expanded the risk while pulling more and more collateral out of the system until we reached a tipping point, NOW!

Let me finish with this one point. When this era is looked at in hindsight, “it will all be about counterparty risk”. Do you know of anything without counterparty risk? Can you say G-O-L-D?

********

Courtesy of www.milesfranklin.com

share

share

share

share

share

Bill Holter writes and is partnered with Jim Sinclair at the newly formed Holter/Sinclair collaboration. Prior, he wrote for Miles Franklin from 2012-15. Bill worked as a retail stockbroker for 23 years, including 12 as a branch manager at A.G. Edwards. He left Wall Street in late 2006 to avoid potential liabilities related to management of paper assets. In retirement he and his family moved to Costa Rica where he lived until 2011 when he moved back to the United States. Bill was a well-known contributor to the Gold Anti-Trust Action Committee (GATA) commentaries from 2007-present.

Bill Holter writes and is partnered with Jim Sinclair at the newly formed Holter/Sinclair collaboration. Prior, he wrote for Miles Franklin from 2012-15. Bill worked as a retail stockbroker for 23 years, including 12 as a branch manager at A.G. Edwards. He left Wall Street in late 2006 to avoid potential liabilities related to management of paper assets. In retirement he and his family moved to Costa Rica where he lived until 2011 when he moved back to the United States. Bill was a well-known contributor to the Gold Anti-Trust Action Committee (GATA) commentaries from 2007-present.