Gold Miners’ Q3’16 Fundamentals

share

share

share

share

share

share

share

share

share

share

The gold miners just finished reporting their third-quarter results, which proved very impressive. While this small contrarian sector is now languishing in the doghouse following a brutal post-election selloff, the gold miners’ fundamentals are strengthening. Lower costs and higher gold prices led to surging operating cash flows and profits. The major gold miners are great fundamental bargains for contrarians today.

Gold-stock bulls are among the largest ever seen in all the markets. The flagship HUI gold-stock index skyrocketed 1664% higher over 10.8 years ending in September 2011, trouncing general-stock-market losses of 14% per the S&P 500. Even this year between mid-January and early August, the HUI soared 182% in just 6.5 months! Radical wealth-multiplying upside like that is well worth any psychological price.

And that is extreme volatility in gold stocks, which alternatively soar then collapse. After the election as futures speculators dumped gold hedges, the gold stocks suffered an incredible second mass-stopping event in less than 6 weeks. That took the HUI’s total massive correction to a colossal 36.6% in just 3.3 months! Provocatively mid-bull corrections of this magnitude have been suffered before in gold stocks.

Unfortunately most traders get caught up in the popular fear such enormous selloffs generate, so they flee gold stocks in disgust and don’t look back. That’s tragic, as the deeper the correction the greater the buying opportunity and coming upside as gold stocks inevitably rebound. I’ve always found digging into gold stocks’ fundamentals is a great way to overcome prevailing fear in order to buy low after a massive correction.

For several weeks now, starting well before the election and subsequent gold-stock plunge, I’ve been researching the quarterly reports from the major gold miners. Like all publicly-traded companies, they are required to report results to investors and regulators four times a year. In normal quarters that don’t end fiscal years, these 10-Q reports are due 45 days after quarter-ends. That means November 14th for Q3.

These comprehensive reports are a treasure trove of valuable information for investors and speculators, a great boon to financial-market transparency. I’ve traded gold stocks for decades now, and there’s truly no information in this sector I look more forward to than quarterly reports. They reveal hard fundamental reality that shatters all the misconceptions driven by the ever-shifting winds of sentiment, a wonderful thing.

The definitive list of major gold-mining stocks to analyze comes from the world’s most-popular gold-stock investment vehicle, the GDX VanEck Vectors Gold Miners ETF. Its composition and performance are similar to the benchmark HUI. GDX utterly dominates the gold-stock-ETF space, with no meaningful competition. Its net assets of $9.7b are now running 35.4x those of the next-largest 1x-long major-gold-miners ETF!

Being included in GDX is the gold standard for gold miners, as it requires deep analysis and vetting by elite analysts. And due to ETF investing eclipsing individual-stock investing, major-ETF inclusion is one of the most-important considerations for picking great gold stocks. As the vast pools of fund capital flow into leading ETFs, these ETFs in turn buy shares in their underlying companies bidding their prices higher.

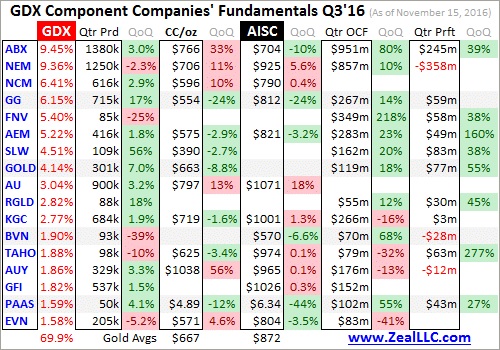

As of this week GDX included a whopping 52 major “gold miners”! Despite being advertised as a “Gold Miners ETF”, GDX also includes major silver miners, silver streamers, and gold royalty companies. GDX is nowhere near as pure as its name implies, but it’s what we’ve got. For weeks I’ve dug into the 10-Qs of the top 34 GDX-component companies, a number chosen because it fits neatly into the two tables below.

Collectively these top 34 GDX-component stocks account for 90.1% of GDX’s total weighting, a commanding sample. While the great majority of these companies’ Q3’16 results were released on time, a few didn’t make that 45-day cutoff. GDX includes foreign miners trading in Australia, the UK, and Hong Kong, which report in half-year increments instead of quarterly. So the Q3 results they released varied widely.

I waded through all these quarterly reports and fed the data into a spreadsheet, some of which made it into these tables. If a field is blank, that means the company didn’t report that data for Q3. Those half-year-reporting foreign companies usually don’t include Q3 financial statements, and royalty companies don’t report the same cost data as actual miners. Nevertheless, the Q3 results are a great fundamental snapshot.

The first couple columns show each GDX component’s symbol and weighting in GDX as of this week. Once again not all these companies trade in the States, so if you can’t find a symbol here it is a listing from a company’s primary foreign stock exchange. Next comes each company’s Q3’16 gold production. I used pure gold numbers wherever available, but some miners combine their silver into gold-equivalent ounces.

That’s followed by the quarter-on-quarter change, the absolute percentage difference between Q2’16 and Q3’16. For now I think that’s more relevant than year-over-year changes, because 2016 has proved so radically different from the deep gold-stock bear of 2015. QoQ changes are also listed for all the rest of the data. That includes both cash costs and all-in sustaining costs per ounce of gold mined in Q3.

Finally the Q3 cash flows generated from operations and actual quarterly accounting profits are shown. The former is the best proxy for how gold miners are currently faring, among their most-important fundamental tells. Both operating cash flows and profits generally exploded higher quarter-on-quarter in Q3, revealing gold miners’ great leverage to gold upside that has long made fortunes for brave contrarians.

One of the good attributes of gold miners is they can easily sell every single ounce they’re able to wrest from the bowels of the earth. Many of the elite GDX gold miners grew production in Q3, with these top 34 showing an impressive average gain of 2.4% QoQ. Higher production generally translates into lower costs too, since the huge fixed costs of mining are spread across more ounces. That means bigger profits.

Nevertheless, the total 9898k ounces produced by these elite gold miners in Q3 was 0.3% lower than the GDX top 34’s Q2 production. Part of that is due to the shifting composition of this leading ETF. As it is essentially weighted by market capitalization, different gold miners rise into and fall out of the top 34 from quarter to quarter. Their total Q3 production translates into 307.9 metric tons, which is interesting.

According to the World Gold Council’s recently-released Q3 Gold Demand Trends report, which is the world’s best read on global gold fundamentals, Q3 mine production ran 846.8t. So these top 34 GDX-component gold miners account for over 36% of the world total, a big chunk. Much gold is produced as a byproduct by companies that don’t specialize in this metal, so their stocks don’t offer much gold upside exposure.

Quarterly gold-miner production is fairly variable, so don’t read too much into big jumps or drops in the Q3 production of your favorite major gold miners. Rarely a new mine comes online or another gold mine is acquired leading to a sustainable production jump. But most of the time even significant changes in production from quarter to quarter are just mining-plan noise that will likely soon reverse the other way.

Gold deposits certainly aren’t homogeneous, with different areas in the same ore bodies having major variations in gold mineralization. Gold miners often have to dig through lower-grade ore to get to higher-grade ore underneath. So overall production slides in quarters where the ore mix fed into mills is lower-grade, and surges when it is higher-grade. Miners also target lower-grade ore when gold prices are higher.

And that was certainly the case in Q3, where gold averaged $1334 per ounce. That was up a big 6.0% sequentially from Q2, showing why gold miners’ collective results looked so strong. While gold is faring much worse so far in Q4, averaging just $1266 thanks to some sharp gold-futures selling, these Q3 results show miners’ great inherent profits leverage to rising gold prices. As gold soon rebounds, that will really kick in.

With that $1266 Q4-to-date average in mind, gold miners’ latest production costs are very interesting. For decades, the metric of choice was cash costs. They include all the cash expenses necessary to produce each ounce of gold, including all direct production costs, mine-level administration, smelting, refining, transport, regulatory, royalty, and tax expenses. They are the acid-test measure of gold-miner survivability.

The average gold cash costs of the top GDX miners reporting them in Q3 ran $648 per ounce. Although that was up 5.0% QoQ from Q2’s $617, it really hammers home how fundamentally strong this deeply-out-of-favor sector is today. The gold miners would face no existential threat even if gold was somehow able to miraculously plummet to half current prices! Even this week’s $1225 gold levels are very profitable to mine.

On an individual-miner basis, cash costs generally fell if quarterly production rose. Spreading the costs across more ounces naturally leads to lower per-ounce costs. But again that’s usually more a function of the particular ore being mined in a quarter than any operating efficiencies. With Q3’16’s average gold price the best seen since way back in Q2’13, the miners had some breathing room to process lower-grade ore.

Way more important than cash costs are the far-superior all-in sustaining costs. They were introduced by the World Gold Council in June 2013 to give investors a much-better understanding of what it actually costs to maintain a gold mine as an ongoing concern. AISC include all direct cash costs, but then add on everything else that is necessary to maintain and replenish operations at current gold-production levels.

These additional expenses include exploration for new gold to mine to replace depleting deposits, mine-development and construction expenses, remediation, and mine reclamation. They also include the corporate-level administrative expenses necessary to oversee gold mines. All-in sustaining costs are the most-important gold-mining cost metric by far for investors, revealing miners’ true operating profitability.

In Q3 these top 34 GDX companies which reported AISC averaged a very-impressive $855 per ounce! As long as the gold price stays above that, these elite major gold miners can operate indefinitely. That was actually a major 3.5% QoQ drop from Q2’s average of $886! While miners’ cash costs rose in Q3, in the key AISC realm that really matters they squeezed out more operating efficiencies. That means bigger profits.

At Q3’16’s average gold price of $1334, an $855 AISC leads to industrywide major-gold-miner profits of $479 per ounce. That’s a whopping 28.4% higher quarter-on-quarter on a mere 6.0% increase in the gold price! The gold miners’ great profits leverage to gold is the primary reason this sector enjoys such incredible upside in gold bull markets. Huge gold-stock gains are fundamentally justified by exploding profits.

Just like cash costs, all-in-sustaining-cost variations between quarters are often driven by changing gold production. Higher production spreads the big fixed costs of gold mining across more ounces, leading to lower AISC. While this proved true individually in many GDX components in Q3, remember that as a whole these top 34 miners’ production fell slightly QoQ. Thus this industry really did become more efficient!

Of course lower costs and higher gold prices fueled exploding operating cash flows and actual profits in Q3. The last time I did this analysis for Q2’16, the top 34 GDX-component stocks generated total cash flows from operations of $4070m. In Q3 alone this total surged 22.0% QoQ to $4964m! I really doubt any other sector in the world just enjoyed such massive sequential operating-cash-flow growth, it’s amazing.

And some individual gold miners naturally fared much better than their peers’ average. While GDX is a fine gold-stock investment vehicle, its performance always suffers from serious over-diversification. The performances of the best-of-the-best elite gold stocks, many of which are included in GDX, are offset by sub-par performances of the other laggards. I’d much rather own the best individual stocks and forgo the rest.

In Q3 the actual accounting-profitability growth dwarfed the big operating-cash-flow gains. The top 34 GDX-component companies had total Q2’16 profits of $277m. In Q3 that skyrocketed an astounding 155.4% QoQ to $707m! There is no other sector in all the stock markets that even came close to the gold miners in profitability gains. It’s hard to imagine a stronger or superior fundamental underpinning to this sector.

Those sharp recent gold-stock selloffs, early October’s stop running followed by that post-election one, have left gold stocks once again universally despised. Most investors and speculators lack the mental toughness, discipline, and knowledge to want to buy cheap in a battered sector. But for anyone taking the time to understand the major gold miners’ powerfully-bullish fundamentals, today’s buying op is outstanding.

In a lot of ways today’s dismal gold-stock psychology reminds me of mid-January, when the gold stocks were trading at fundamentally-absurd valuations relative to prevailing gold prices. Instead of looking at their underlying fundamentals, traders were all caught up in the popular fear dominating that time as the gold stocks languished at 13.5-year secular lows. Yet gold stocks would soon nearly triple from those levels!

Today investors and speculators are again making that same capital-slaying mistake. They see that the gold stocks have fallen sharply, so they extrapolate such extreme losses continuing into the indefinite future. Buying into herd psychology blinds them to the gold miners’ phenomenal fundamentals, and their enormous future upside potential. So instead of wisely buying low now, they will foolishly buy high later.

There’s little doubt the gold miners’ Q4 results will be considerably weaker than Q3’s strong ones. Once again so far in Q4, gold is only averaging $1266 compared to $1334 in Q3. If that average holds for the rest of Q4, and the gold miners can hold average all-in sustaining costs at $855, their per-ounce profits are going to slide 14.4% QoQ to $411 per ounce. But odds are the gold price won’t linger near lows for long.

Last week I wrote an essay on how gold and its miners are likely to fare under a Trump Administration. Since gold moves counter to stock markets, it has always been something of an anti-stock trade. The post-election fantasy that this overvalued, long-in-the-tooth, Fed-levitated stock-market bull will manage to magically continue higher for the next four years is ludicrous. Stock markets are trading near bubble valuations.

Trump himself warned about this many times, declaring in the first presidential debate which was his largest audience ever that stock markets “are in a big, fat, ugly bubble.” As the surprising post-Trump-win stock-market euphoria inevitably fades and leaves the ugly reality of dangerously-overvalued stock prices, stock markets will start rolling over again. And then investors will resume diversifying into gold.

Gold investment demand has been the entire story of 2016’s young new gold bull, and American stock investors remain radically underinvested in gold. One proxy of this is the value of that leading GLD gold ETF’s holdings compared to the collective market cap of the dominant S&P 500 stock index. That ratio is currently running just 0.182%, not far off late-2015 lows. Between 2009 to 2012, it averaged 2.6x higher at 0.475%!

So investors need to greatly add to their gold portfolio exposure. And sometime in the coming months as the stock markets roll over, gold investment demand is going to come roaring back. So the likely-worse gold-miner operating results coming in Q4 are almost certain to prove short-lived. Once gold starts to power higher again, gold miners’ great profits leverage to gold will kick in and this sector will resume soaring.

The gold miners’ strong Q3 results are a microcosm of what’s to come as this young gold bull continues to climb on balance in the coming years and mature. It’s sad that most investors and speculators don’t realize this. They forget that major selloffs are soon followed by major uplegs, and succumb to the trap of assuming recent market trends and levels will persist indefinitely. Nothing could be farther from the truth.

Even though gold’s young bull market in 2016 has been minor so far, up just 29.9% at best by its latest early-July interim high, the gold miners’ operating profitability has exploded higher. There’s nowhere else in all the stock markets where a sector has seen greater fundamental progress. And the anomalous post-election gold-stock plunge on stop losses being run has granted an incredible buy-low opportunity.

At Zeal we’ve spent decades researching and trading gold stocks, with excellent results. As of the end of Q3, all 851 stock trades recommended to our newsletter subscribers in real-time since 2001 averaged stellar annualized realized gains of +24.1% including all losers! That’s an order of magnitude greater than the general stock markets’ performance over that span. Achieving it required staying focused no matter what.

Sadly most investors and speculators lose interest in gold stocks the moment they correct hard. So they foolishly bury their heads in the sand. Big gains are only possible by staying informed all the time. Only that will ensure you are aware when gold stocks are screaming buys fundamentally, like today. We can help you stay informed and fight your own greed and fear with our acclaimed weekly and monthly newsletters. They draw on our vast experience, knowledge, wisdom, and ongoing research to explain what’s going on in the markets, why, and how to trade them with specific stocks. Subscribe today! For just $10 per issue, you can keep abreast and thrive.

The bottom line is the major gold miners’ fundamentals in just-reported Q3’16 were incredibly strong and bullish. Due to lower all-in sustaining costs and higher prevailing gold prices, this sector’s cash flows generated from operations and actual accounting profitability exploded higher quarter-on-quarter. The fundamental transformation gold stocks have undergone in 2016 has been amazing, and it is only starting.

But unfortunately most investors and speculators today aren’t paying attention to the gold miners’ strong fundamentals. Instead they are all wrapped up in the fearful prevailing sentiment. That’s a big mistake as always. While gold-mining operating profitability will decrease in Q4 if gold prices remain low, gold’s young bull is far from over. When it starts powering higher again on weaker stock markets, gold stocks will soar.

Adam Hamilton, CPA

So how can you profit from this information? We publish an acclaimed monthly newsletter, Zeal Intelligence, that details exactly what we are doing in terms of actual stock and options trading based on all the lessons we have learned in our market research. Please consider joining us each month for tactical trading details and more in our premium Zeal Intelligence service at … www.zealllc.com/subscribe.htm

Questions for Adam? I would be more than happy to address them through my private consulting business. Please visit www.zealllc.com/adam.htm for more information.

Thoughts, comments, or flames? Fire away at zelotes@zealllc.com. Due to my staggering and perpetually increasing e-mail load, I regret that I am not able to respond to comments personally. I will read all messages though and really appreciate your feedback!

Copyright 2000 - 2016 Zeal LLC (www.ZealLLC.com)

share

share

share

share

share