Wall Street And A Strange Dollar

share

share

share

share

share

share

share

share

share

share

So far, at least, increasing inflation does not in the least seem to be of a ‘transitory’ nature. In fact, it could be speeding up. Also so far, there is no noticeable decrease in the printing of dollars. The number of Covid-19 cases is declining, even more so in the south, but the threat of the virus still has Americans nervous and subject to many regulations from state to state, which means the economic recovery is sluggish. So why has the dollar been so strong since the double bottom at the end of May?

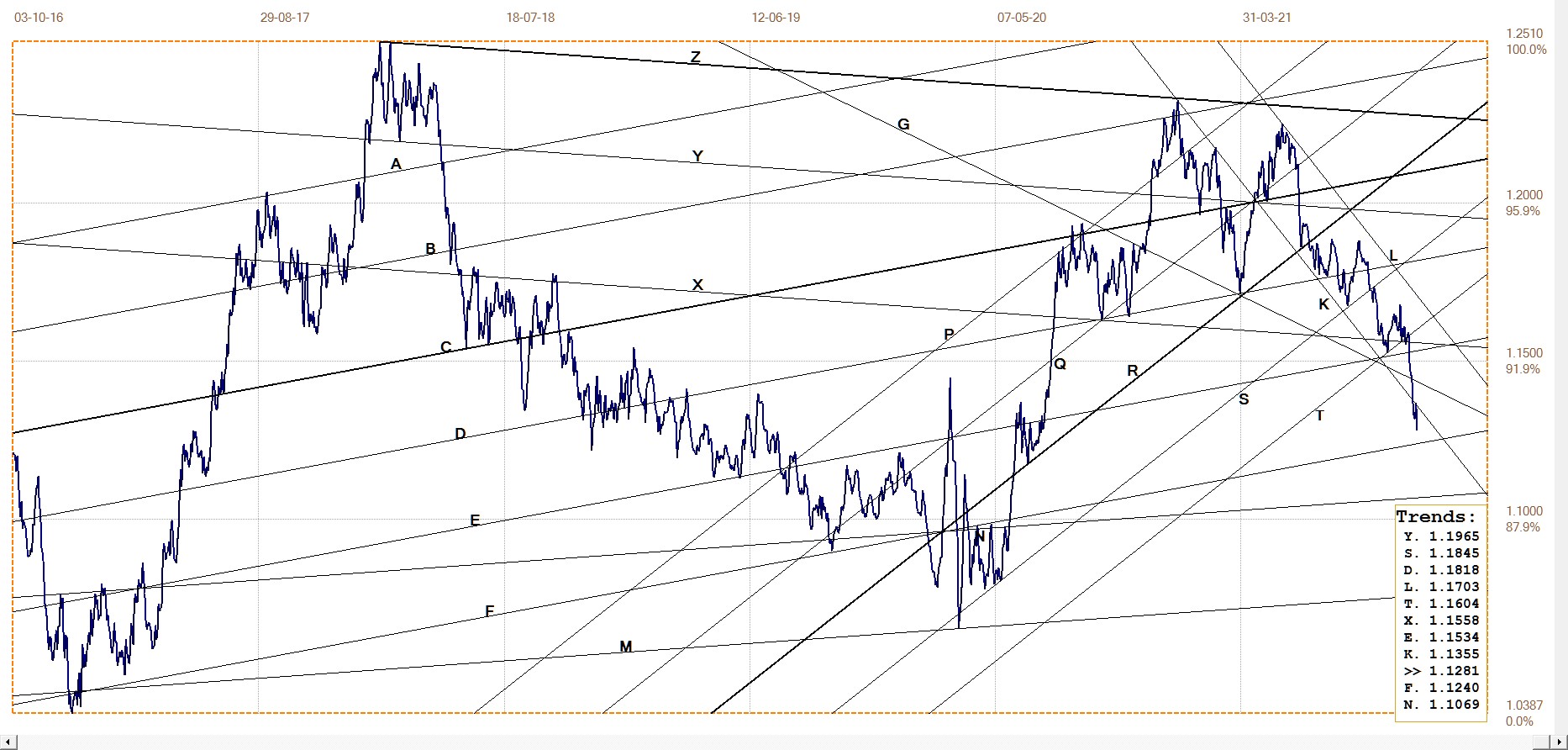

Despite the negative fundamentals during 2021, the dollar ended its post March 2020 bear trend as the new year took off and rallied into March, until the pandemic hit and it retreated into a double bottom at the end of May. Since then it has rallied from 89.5 to reach 96.03 on Friday – a 7.3% increase, which is large in forex terms and it was still accelerating into last week. This performance of the dollar is as if all the normal guidelines that describe how currencies typically react to changing economic and financial conditions in countries have been turned upside down.

The normal guidelines of course apply to ‘normal’ economic conditions, all things being equal, when markets react in a ‘normal’ way to the fundamentals of the situation. However, markets do not only react to economic fundamentals - such as a currency that reacts as anticipated to high inflation or to massive money printing – they can also react to other factors; political ones, for example. For example, if the ruling powers that be believe a market or a currency must carry a message to the investor public and other markets, local and foreign, then it is proper and sanctioned to nudge the market and currency in the right direction. Self-preservation is an amazingly strong emotive force which justifies much that normally would not be condoned by all of society.

It became evident during the Trump years that Wall Street was acting as a barometer to measure the success of the administration – the strong equity market often was used in that respect by mr. Trump in speeches and interviews. As time passed, it was ever more clear that quite a lot of nudging was happening to keep Wall Street strong and any sudden weakness was halted and steeply reversed using much more force than mere nudges. The new Biden administration simply had to continue that practice – having a crash on Wall Street would have been very visible evidence of the failures of the new economic and other policies.

However, as Wall Street kept on creeping higher and investors were becoming nervous, there were rather frequent and sudden corrections. These were soon halted and reversed, which then required serial new all time highs to convince investors that these sudden steep dips were not the beginning of a bear trend. Serial new highs soon had the PE on the Dow30 and the S&P500 rising to 40 and then to 42 – red flag danger levels in an economy suffering from all manner of shortages and pandemic related restrictions.

When nudging and even force are no longer fully effective, allies have to be mustered to offer assistance. The first one to be called into action clearly had to be the dollar. It had been in a bear trend since the Covid scare in March 2020, but the bullish reversal late in May was just in time to come to the assistance of Wall Street in early June. The DJIA lost 4.2% in two weeks; the steepest decline since October 2020, at which time the dollar rally surely assisted the recovery on Wall Street through June and into July and August.

Wall Street does not receive only semi-official support. The long pre-Covid bull market had proven beyond any doubt that investors do better when placing their money in passive investment funds rather than in funds that are actively managed. The returns mostly outperformed the active funds, in part because passive funds charged a lower cost. Passive funds deliver a lower return for the fund managers, but that is balanced by larger portfolios – as long as the money remained in the fund. This meant for as long as equity prices maintained their uptrend – which in turn meant that these funds also stepped up with their spare cash when Wall Street dips and help to restore the bullish momentum.

Dollar Index. Last = 96.03

Technically the break above channel CD implies that the dollar could reach as high as line M, at 96.8, which is the bottom of the main bull channels that followed after the financial crisis had settled down, at least as far as the currencies are concerned. This could imply that an equity bear market is not likely to start off on Monday, but that we could see some more sideways drift, perhaps without any new all time highs.

On the other hand, there is a belief among some old timers that a weak Wall Street on a Thursday, followed by a larger decline on Friday, results in a Black Monday. If that holds true, this could lead into an interesting week ot two.

Some new information about the vaccines is here and here for interested readers.

Euro–Dollar

The stronger dollar last week also claimed the euro as a victim; it broke clear below the support of the already steep bear channel KL. The initial break was followed by a ‘goodbye kiss’ on line K – the brief retracement to touch the line, before sinking to a new low.

Technically, this is not a positive sign, UNLESS the euro can quickly reverse to break into the channel again, thereby leaving a very skewed bifurcated low below line K. The odds of this happening decrease quite rapidly the more the euro continues to lose ground against the dollar. While good for the euro price of gold, this is otherwise bad news for the PM metals, yet adds a boost to Wall Street for foreign investors.

Euro–dollar, last = $1.1281 (www.investing.com)

DJIA daily close

DJIA. last = 35601.98 (money.cnn.com)

Wall Street as per the DJIA has been predominantly bearish since it reached another all time high two weeks ago. No wonder the dollar index closed back above the 96.0 level on Friday with the daily volume on the 30 Dow stocks more than a third higher than the three-month average. It required digging into deep pockets, probably from various sources, semi-official and the passive funds, to halt the slide at only a loss of 289 points.

A sequence of negative closes from Wednesday to Friday for a combined loss of 540 points sets Wall Street up for a decisive trading day on Monday. It will not surprise to find the Dow futures up by more than 150-200 points early on Monday as the market is being pre-empted to show a broad smile for investors when the new week begins.

Whether increasingly scared investors will fall for the swindle is not definite; the smile is bound to require more deep pockets for Wall Street to end in the green on Monday – probably with dollar support and various official announcements of how great the economy is doing. Further supported by news flashes, of dubious quality and veracity. Apologies for the mistakes appear in fine print on page 3 or 7, days later after the desired effect had been achieved and investors had been hoodwinked. Again.

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1861.10 (www.kitco.com)

As the chart shows, the improvement in the price of gold managed to break clear of the resistance of line Y, but then ran out of steam last week to make minor gains only. The combination of a stronger dollar late last week and the increased pressure on the Comex as the price approached $1800, caused it to retreat and hold.

As discussed previously, the ideal message would be if the price could break above line C at $1910 on the London PM fix. If that were to happen – and then hold through to the month end and beyond – December could be a good month for the yellow metal.

Euro–gold PM fix

Much the same behaviour of dollar gold, but assisted by the weaker euro to increase even further last week. The euro price is well cushioned above the resistance and also within bull channel RS. This implies that the price of gold in euros, while it is never invulnerable, is technically robust and retains a bullish bias for the near to medium term, despite possible setbacks and ravages of the approaching Comex month end.

Euro gold price – PM fix in Euro. Last = €1646.14 (www.kitco.com)

Silver Daily London Fix

Silver daily London fix, last = $24.785 (www.kitco.com)

The recent break by the price of silver, as per the London fix to above the $24 level as well as clear above persistent and narrow bear channel XY that had contained the price for too long was a welcome bullish signal. The rally carried the price to the cross-over of lines Y and C where it was compelled to reverse back below $25. This week the Comex month end looms on the horizon and it would require a tremendous effort to get back above $25 and also break above lines C and Y.

As many believe, time is on our side and if that could not be achieved this week, or even achieved only after the week thereafter, with NFP history, the future would look much brighter and make December a pretty good month to end off a dismal 2021.

U.S. 10–year Treasury Note

10–year Treasury note, last = 1.548% (Investing.com )

Early in November, the yield on the 10-year Treasury note spiked lower from 1.603% to reach 1.439% five days later. A drop of more than 10% in the yield of the largest market in the world in such a brief time comes as a shock that triggers a sudden need for significant adjustments in large portfolios; a process that makes lots of ripples.

I do not know what caused the large move, yet it came at a time when Wall Street was stagnant and not making any progress. Whether this is pure coincidence is quite possible – but it came at the right time to suggest that inflation is not such a serious problem, which would have been good news for Wall Street.

Coincidentally, as soon as the yield had completed the spike, Wall Street rallied again. Two days later the yield was back up where the spike had started from and the fund administrators had to reverse all the adjustments they had made the previous week.

It might be too easy to read too much into this, but 10% moves in the yield of the US 10-year note do not happen often. When this does happen, it typically signals some significant change in the market fundamentals. It is a surprise when the fundamentals spontaneously correct within two days for the spike to reverse all the way. Strange.

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $76.10 (www.investing.com)

Between 2 and 4 November the price of crude had its own bear spike that reversed fully within three days, only to spike lower again to end on Friday at the low price for the week. The many pleas for lower energy costs to reduce the inflationary effect of high energy costs have been answered, perhaps only in part so far, with more good news to come.

It is of course not widely known whether the sudden decline in the price of crude is due to less demand in a stagnant economy or as a market response to the threat of higher inflation. There is no doubt that it came at the right time to help boost Wall Street after it had slipped steeply lower shortly after the most recent all-time high.

Whatever the reason for the decline, it does make for interesting speculations, given the coincidences that have been proliferating for a long time and more so recently.

©2021 daan joubert.

********

share

share

share

share

share

More from Gold-Eagle