Interest Rates, Money Supply And GDP

That the world is on the edge of a monetary and economic cliff is becoming increasingly obvious. And becoming more obviously permanent than transient, price inflation will almost certainly lead to rising interest rates. Rising bond yields, falling equity markets and debt-triggered insolvencies will naturally follow.

According to the economists prevalent in official circles, a prospective mix of so-called deflation and rising prices are contradictory, should not happen at the same time, and therefore cannot be explained. Yet that is the prospect they now face. The errors in their lack of economic judgement have evolved from the time when central banks began to manipulate their currencies to achieve economic objectives and then to subsequently dismiss the evidence of policy failure. It has been a cumulative process for the Federal Reserve and the Bank of England since the 1920s, which can only now end in a final catastrophic failure.

The denial of reasoned economic theory, embodied in a preference by state actors for state-driven outcomes over free markets, has led to this cliff-edge. This article explains some of the key errors in economic and monetary theory that have taken the world to this point — principally the relationships between interest rates, money supply, and GDP.

Introduction

Following the First World War, central banks have not only acted as lender of last resort, which was the role the Bank of England and its imitators took on for themselves in the preceding decades, but they have increasingly tried to manage economic outcomes. The trail-blazer was pre-war Germany which grasped Georg Knapp’s state theory of money as justification for Prussia’s socialism by currency, eventually ending with the collapse of the paper mark in the post-war years. But the genesis of today’s monetary policies has its foundation in the then newly constituted Federal Reserve Bank, chaired by Benjamin Strong, who in the 1920s collaborated with Norman Montague at the Bank of England who was struggling to contain Britain’s post-WW1 decline.

Domestically, Strong was an advocate of monetary expansion, a policy that fuelled the Roaring Twenties, the excessive speculation that culminated in the Wall Street Crash, and the severe depression that followed. You would think that the experience of those times would have caused central bankers to reflect and consider the causes of failure, perhaps realising that it was Strong’s earlier inflationary policies that were responsible for the depression. They did reflect, but concluded that it was markets, not their policies that were at fault. If anything, they concluded that their remedies for the depression had not been imposed vigorously enough.

Having more sympathy with Knapp and the Prussian historicists than for free markets, the Fed and the Bank of England continued to seek inspiration from interventionist policies between the two world wars. A body of intellectual work grew up to support their suppositions, downgrading and eventually dismissing policies based on sound money. At the London School of Economics, Keynes triumphed over Hayek, who gave up criticising Keynes as a thankless task, doubly made a waste of his time when Keynes responded to Hayek ‘s criticism that he no longer believed in the theories he had previously promoted.[i]

In the 1970s, when price inflation threatened to get out of control, mainstream economics had devolved into Keynesianism, which was then becoming discredited, and the monetarism of Milton Friedman gained attention. The monetarists resuscitated David Ricardo’s equation of exchange explaining why the expansion of currency and credit led to rising consumer prices. But the monetarists were too mechanistic in their approach, failing to appreciate the importance of subjectivity of a currency’s purchasing power in the hands of the public. Furthermore, Friedman believed in managing inflation rather than stopping it. Both sides of the economic debate were therefore exposed by unsound or incomplete theoretical arguments from which the party expressing beliefs most suited to statist objectives would inevitably triumph.

From the 1980s the drift back into Keynesianism led to increasing suppression of free markets by governments and their central banks. From the original belief that the private sector would need a helping hand from time to time through deficit spending, policies have evolved towards full time intervention and regulation. Today, the state believes that private sector actors cannot be trusted to do anything without firm state control. That is how far removed from market reality the state has become.

The irony in all this is that the state depends on private sector actors for its revenues. And as a source of revenue, they now have their limitations. After increasing taxes to the point of diminishing returns, burdened everyone with the expense and irrelevance of regulation, and having plucked the goose of all its feathers there must be no doubt that debasement of the currency is now a permanent and growing source of funding for modern governments.

That is the background that consciously or unconsciously drives both monetary objectives and the economic beliefs to justify them. Policy makers have dug deep holes for themselves, and they only know to keep digging.

This article explains the fallacies central to a looming monetary and economic disaster — the use of interest rates as a means of controlling inflation, official blindness to the cause of a currency’s failure, and the reliance on a statistic which in economic terms is meaningless: interest rates, money supply and GDP.

Erroneous beliefs over the role of interest rates

Central bankers and the entire investment community believe the relationship between prices and money is governed by interest rates. In other words, to contain inflation, by which the establishment means increases in the consumer price index, interest rate management is the key. For empirical evidence, it is often referred to Paul Volcker, when as Fed Chairman he raised interest rates to unprecedented levels to kill inflation and to stop it accelerating even more.

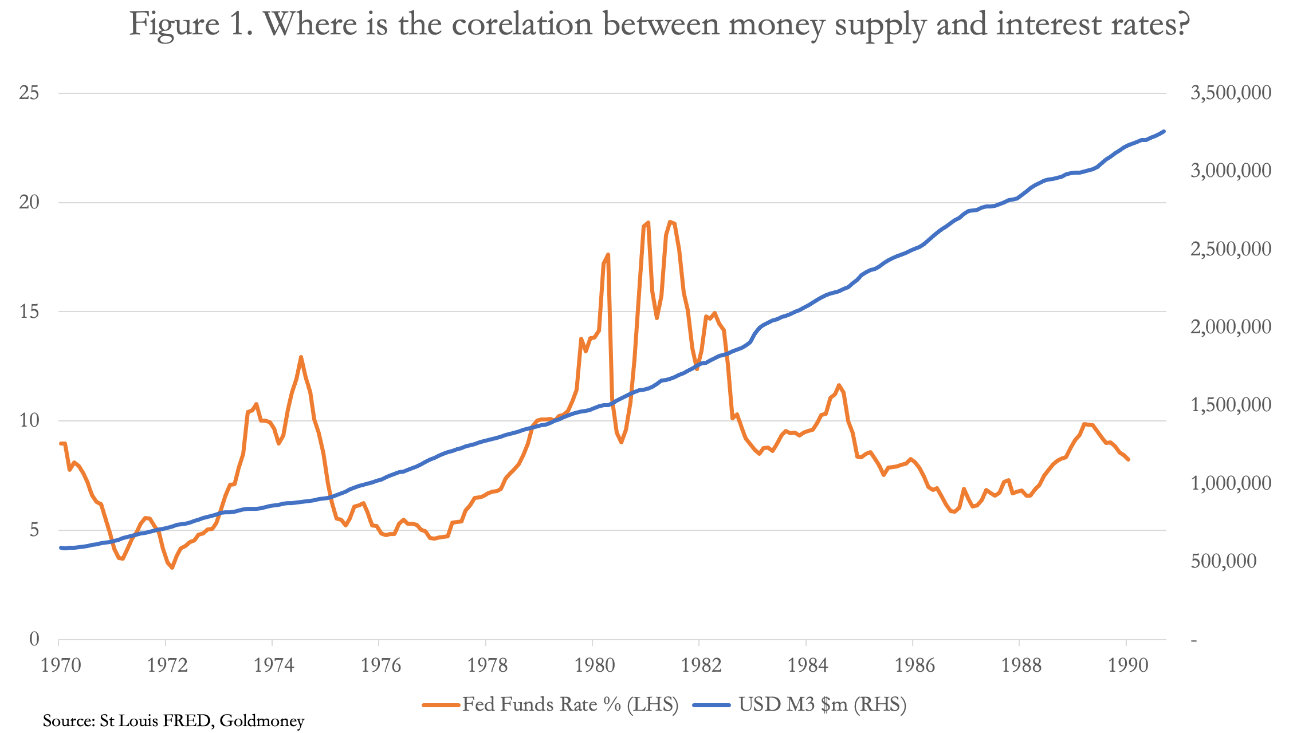

But empirical evidence on its own is insufficient — a proper analysis is required. The Volcker story ignores the actual relationship between interest rates and the quantity of money, which is shown in Figure 1.

Expectations of continually rising prices were suppressed in the early 1980s by near 20% Fed Funds Rates. But money supply continued to expand unabated —even increasing its rate of expansion to accommodate higher interest payments.

To the extent that increases in the quantities of money and credit continued, interest rate policy was an abject failure. This failure was not widely appreciated at the time, when the focus, as it is today, was on the consequence for prices. But measurement of prices as an indication of inflation is subjective to the statistician compiling the statistics, with method subject to change. And when the cost of indexation threatened to destabilise government finances, methods of statistical suppression of the consumer price index increases were applied.

But the evidence from Figure 1 raises other important questions. Should policy planners stick with managing interest rates as the primary method of inflation control? Why is it that interest rates do not correlate with the quantity of money and credit: does that mean that interest rates do not represent the price of credit? Does this lack of correlation portend a policy failure?

Resolving these questions is now an urgent priority. Price inflation everywhere is increasing at a time when economies in all the major jurisdictions are stalling. Undoubtedly, the policy response will be to raise interest rates, however reluctantly, while remaining free to expand the quantities of currency and credit to support economic activity, government spending and to resolve systemic failures.

But as I postulated in an article on the condition of the Eurozone, even a modest rise in euro interest rates will almost certainly lead to a substantial contraction of its bloated repo market, which would be reflected in a collapse of outstanding bank credit in a banking system riddled with concealed bad debts, and where banks from large to small have total asset to equity ratios of over twenty times. The ECB is effectively trapped. The US will have a different crisis on its hands, whereby rising interest rates will undermine financial asset values, upon which the Fed has relied to keep economic confidence intact. It will destabilise heavily indebted government finances. And zombie corporations, overloaded with unproductive debt, will likely fail, all potentially leading to depression-levels of unemployment.

Put succinctly, we have moved on from the Volcker years and today the overall debt situation, which has become hyper-sensitive to interest rate rises, is more serious than it has ever been. The solution whereby central banks print their way out of interest rate increases without collapsing their currencies is an illusion when the role of interest rates is properly understood. To understand why, we must answer the question posed in Figure 1 above about the non-correlation between interest rates and the quantities of currency and credit. Only then can we truly see the extent of the fallacies driving contemporary monetary policies.

Interest rates reflect time, not cost

If there is one reason why the state will always fail in its monetary policies, it is the inability of the bureaucratic mind to incorporate time into its decision-making. In the productive market economy, which is little more than a name for the collective actions of transacting individuals and their businesses, time is central. A producer incorporates time in his profit calculations, and a consumer in his needs and desires, whether wanting something immediately or being prepared to defer his purchase. And because money is the link between both earnings and spending and savings and investment, time is of the essence for money as well. It is this irrefutable fact that leads to a preference for money to be possessed sooner rather than later. And if a human is to part with it temporarily to be returned later, naturally he or she will expect compensation for the loss of its utility.

Fundamentally, this is what interest rates in the market economy represent. It is the time preference factor, set between transacting humans, which values possession in the future less than possession today. To pure time preference, we can add an element for counterparty risk. And when transacting humans anticipate a fall in purchasing power before money owed is returned, that is yet another factor.

The common central bank target for price inflation of 2% implies that interest compensation to include an element of time preference and monetary depreciation suggests a base case without counterparty risk for a minimum of a 3% interest rate. But already, dollar prices are rising at 6.2%, so we should be seeing annualised interest rates of perhaps over 7%. Even that 6.2% rate is heavily doctored, so perhaps it should be a minimum of 10% or even more. See Figure 2 and think about the time preference implications if John Williams at Shadowstats.com is only half right in his analysis of consumer price inflation, which he calculates is approaching 15%.

And then there is counterparty risk — the possibility that interest won’t be paid. Without placing any reliance on government statistics, or anyone else’s for that matter, it is obvious that the gap between officially imposed interest rates and market reality is probably greater than it has ever been.

We cannot know what the interest compensation for temporarily parting with money should be; that is a matter for transacting individuals. But clearly, keeping interest rates supressed at the zero bound is inhibiting the deployment of capital for productive purposes funded by genuine savings. We should not be surprised at this development, because replacing savers with the state as the source of investment capital was Keynes’s ultimate objective expressed in his General Theory.[ii] But it means that the state must be able to evaluate the terms of providing capital, to judge to whom it is to be provided, and then to provide it. It requires a judgement in the absence of economic calculation incorporating time, the latter which, as pointed out above, is wholly beyond bureaucratic contemplation.

Now let’s look at the situation without the state’s monetary planning. In free markets with sound money, having identified a possible venture, a business can calculate its anticipated costs, and from its knowledge of market prices can estimate the interest cost that it is prepared pay to permit the project to be profitable. If a proposed investment is deemed profitable, the business must then be prepared to bid up the interest rate sufficiently to entice consumers to defer some of the fruits of their labour from immediate spending. It is this demand for capital which effectively sets the interest rate in the context of the time preference demanded by prospective savers to attract the necessary capital. And market factors also ensure it is generally allocated for its most productive use.

Critics of time preference theory might say that businesses regard interest only as a cost, and that as a cost it makes sense to give the state an intervening role to keep the rate as low as possible, to stimulate business activity. But this ignores the fact that businessmen also regard interest as a reference against which profitability must be judged. Even if he doesn’t borrow to fund a production project, an entrepreneur will still measure the anticipated return on his capital against the time preference he can achieve by parting with his funds to other borrowers.

It is therefore a relatively simple matter to understand the role of savings for the provision of capital in a free market. The mistake that Keynes made was to regard interest as usuary charged by savers so they could enjoy a life of ease living off their savings. He ignored the inconvenient truth that not possessing it makes money less valuable. Keynes’s was a belief that favoured his theories of state intervention.

But when one considers the state’s attempts to manage interest rates and ensure capital is made available to the profitable enterprises which will not waste it, we run into insuperable problems. State agencies are not equipped to do the necessary economic calculations, which as we have seen is central to rate-setting. Compared with economies run on free market lines without monetary intervention, the policies of governments using monetary inflation and interest rate management have proved to consistently fail.

With the purchasing power of unbacked currencies now declining at an accelerating pace, the reluctance of the states’ monetary policymakers to permit rates to rise has sprung upon them a debt trap. Central banks have now gone too far down this rabbit hole to backtrack. Their dilemma is beginning to be noticed by homo economicus, who collectively decides the relative values between currencies and consumer goods. As a currency’s purchasing power is undermined by being increasingly discarded relative to possession of goods, markets will eventually force the central bankers’ hands. Until then, the suppression of interest rates will ensure the purchasing power of unbacked state currencies will continue to decline at an increasing pace, measured against commodities, producer input prices, labour and logistics costs, producer output prices, and finally consumer prices.

Putting aside the unrelated problem of logistics disruptions, output will be restricted because of price pressures on production, ensuring there will shortages of essential goods, even relative to falling consumer demand. As an economy enters this slump in business conditions, attempts by the state to stimulate flagging demand by further monetary inflation will only make the situation deteriorate further, with markets demanding yet higher discounts for the future value of money — being time preference reflected in yet higher interest rate compensation.

Ahead of these developments, we should expect financial asset prices to start anticipating the prospect of continuingly rising interest rates and bond yields. Falling financial asset values will undermine the collateral which is central to banking systems. In the Eurozone there is the additional fear that collateralised repo markets, believed to be more than €10 trillion — larger than the combined balance sheets of the ECB and satellite national central banks — will contract severely in the face of positive interest rates. This repo market has become bloated by zero repo rates, meaning that a bank can pass doubtful debts into the euro system as collateral for credit balances at no cost.

While the tendency of bank credit to contract due to falling collateral values will be common to all banking systems it could lead to an initial banking crisis developing in the Eurozone where banks are also frighteningly over-leveraged.

A systemic crisis, combining with a debt trap being sprung on both governments and over-indebted businesses, has now become the certain outcome of interest rate suppression when it fails. The mistake has been to confuse time preference with a price for credit. It is an error as old as the religions that banned usuary, which were also based on this misunderstanding. Having made the error and believing that interest is the wage of usurious sin and therefore can and should be suppressed or banned, there is now no escape from the consequences. When market actors increasingly respond to interest rate suppression by disposing of state currencies, central banks seem bound to drag their heels, initially refusing to accept this reality. For them to do so would make indebted governments, businesses, and consumers insolvent as a matter of official policy. And as economic actors begin to learn the difference between money, which is physical gold and silver, and unbacked currencies, the flight out of currencies will surely gather pace. Arguably, this is already beginning to be reflected in speculative cryptocurrency valuations.

With respect to interest rates central banks have boxed themselves in. But it is important to understand that permitting interest rates to rise to reflect time preference is not the same thing as stopping inflation. There is no guarantee that on its own sufficiently high interest rates will do more than temporarily stabilise the purchasing power of currencies. But even that course of action would appear to be ruled out today.

The inflation problem

Now that we have put interest rates into context, we can tackle the inflation issue. In the 1920s mainstream economics began to drift away from classical quantity theories of money and free markets under the growing influence of Marxist doctrines. The communist socialism of the Soviets was gaining traction, seen simplistically as the only alternative to European fascist socialism, with the established free market approach dismissed as an option. Socialism of the left reinforced arguments in favour of state intervention in the economy and the use of the currency to further socialist objectives. Subsequent evolution of monetary policies has been to remove all constraints on how it is deployed by the state. And today, policy makers have now disassociated inflation of prices entirely from increased quantities of currency and credit.

Recent FOMC statements from the Fed do not mention the quantity of money in circulation at all, sticking to commentary about targets for prices and interest rate policy. Nor are changes in the dollar’s purchasing power ever mentioned. The drip-feed of wealth transfer to the state from the productive economy through currency debasement is never mentioned: instead, monetary policy is claimed to be a necessary stimulant. It is as if illness has become no more than a rash, and not due to an underlying condition. But even empirical evidence clearly shows the link between increasing quantities of currency in circulation and a fall in its purchasing power.

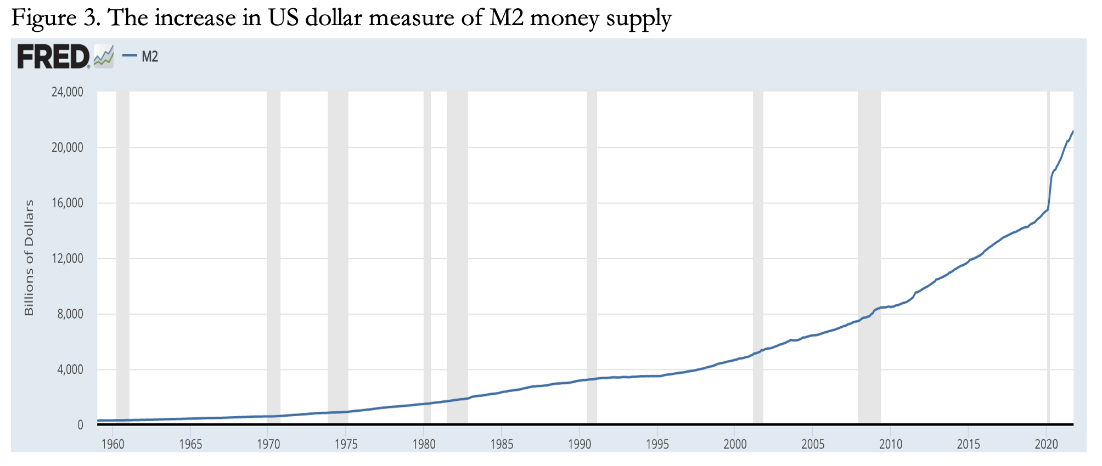

Knowledge of elementary mathematics points in the same direction. Other things being equal, if you increase the quantity of something, the utility of each unit diminishes in proportion to the increase. Thus, if as the monetary policy supremo, you chose to pursue the course illustrated in Figure 3 below, you can expect the purchasing power of your currency to fall significantly — which is why prices measured in a declining currency rise.

From the state’s point of view issuing currency is like shaking olives off an olive tree, and it is not about to admit to any consequences. The public is being kept in a state of ignorance. Further obfuscation comes from new currency and credit being indistinguishable from existing currency. Describing unbacked fiat currency as money is a further smokescreen.

It takes time for new currency and credit to enter the economy as it is spent into circulation. And if the public was aware of the wealth transfer affect, whereby the state, licenced banks, big business, the rich, and the indebted benefit having got initial possession of new currency and credit, while savers, pensioners, the poor and those on low fixed incomes lose out, this dishonest system would collapse in a people’s revolution. But as it is and if the history of monetary inflations is our guide, these losers will only find out too late to save themselves.

The loss of public credibility for a currency as a circulating medium is its death knell. At that point, the mathematics of quantity no longer matter. If the public collectively decides to get rid of all its currency liquidity while it has any purchasing power left, preferring to own goods instead, the currency will be rendered completely valueless. It is also a vote on the credibility of the issuer — usually a central bank or government treasury department. And with the demise of the currency, tax revenues become worthless as well.

The situation is easy to resolve. The first step is to stop issuing currency and credit. Interest rates do not come into it, as Figure 1 towards the beginning of this article demonstrates. But governments are always reluctant to adopt this solution. Promoting interest rates as the mechanism for controlling inflation is basically a smoke screen that has the effect of allowing inflationary funding to continue for the benefit of the state.

Statistical misinterpretation of GDP and currency inflation

Mathematical economists rely on statistics to guide monetary and economic policy without realising the confirmatory biases and tautologies involved. An example of the former is already remarked upon in this article in connection with the measurement of prices, which has been subject to alteration since 1980 to reduce the costs of indexation — that was even publicly admitted the first time the consumer price index was overhauled in the early 1980s. Today, deflated CPI figures are accepted as a true reflection of a currency’s purchasing power. The deception has permitted currency inflation to run at a higher level than otherwise would be tolerated.

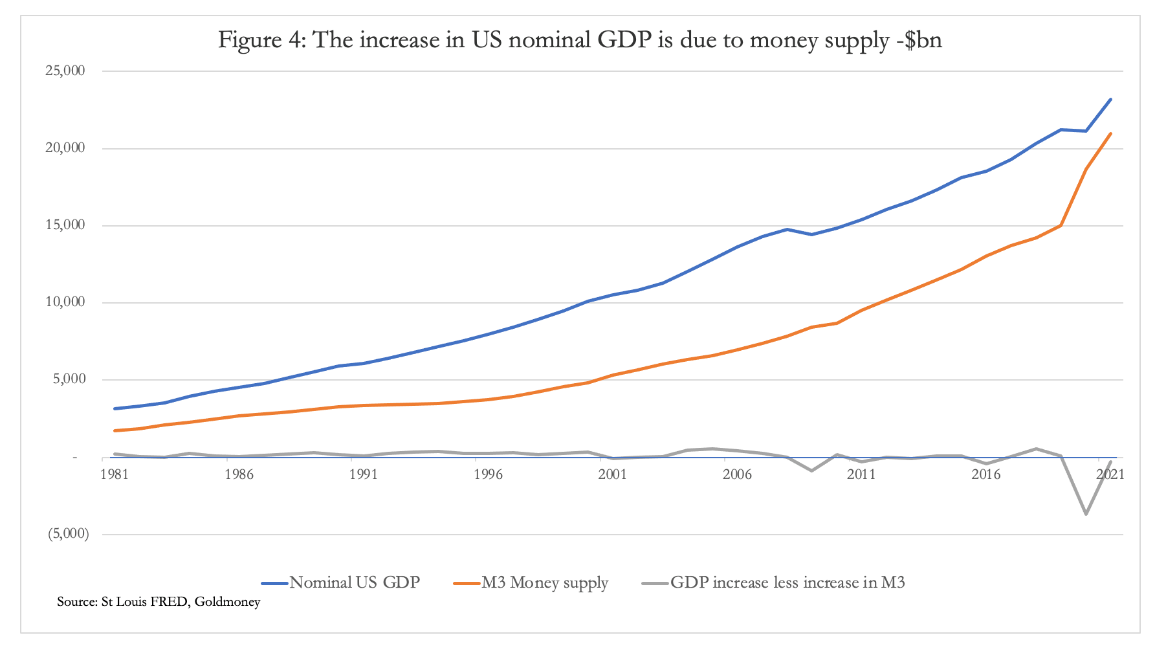

Probably the most dangerous tautology leading to a confirmation bias is denial of the true relationship between gross domestic product as a measure of the total economy and increases in the money quantity. Figure 4, of annual end of fiscal year statistics for the US illustrates an extremely close correlation between the two. The grey line, which shows the difference in their rates of increase, shows only a minor divergence most of the time.

There have only been two notable variations in this correlation. In the great financial crisis thirteen years ago, there was a mild slowing in the pace of M3’s growth rate —affected by falling bank credit during the banking crisis — while the economy entered a brief slump. It was rescued from that slump by currency expansion. More recently, the economy has emerged from covid lockdowns, reflected in a stalling of GDP for fiscal 2020 (to September). At the same time there was a substantial acceleration in M3 growth — reflecting deliberate official deficit spending and quantitative easing. And the correlation has now resumed.

The times of non-correlation can be explained by temporary variations in the savings rate, which when growing defers an increased proportion of total consumer spending, impacting GDP.

Theoretically, GDP is the total of final sales of all new consumer goods and services, which are distinctive in that unlike assets they are not subject to valuation. All consumer products have a limited utility, extinguishing their purchase value. For the purposes of GDP statistics second-hand goods have already been paid for and incorporated in GDP at an earlier date. If the product is a service, its value is fully extinguished once it has been provided.

GDP therefore records direct consumer spending. It also captures increases in savings, but with a variable time lag depending on how those savings are redeployed. When deposited in a bank, they support a bank’s lending, conventionally of working capital for businesses and for loans to other consumers.

Savings directed to bond and equity issues are spent by the issuer in the course of its business. The balance that remains while business expenses are discharged stays in the banking system as deposits, the counterpart through double-entry bookkeeping being assets in the banking system, which ends up being redeployed as unrelated credit or investments. Again, these funds are eventually spent.

Alternatively, if a saver chooses to buy a financial asset in the secondary markets, the seller pockets the proceeds, some of which may be spent, and some of which may be reinvested. Net savings flowing into secondary markets are delayed in their impact on GDP, which is particularly true during bull markets involving growing public participation.

The effect of covid lockdowns reduced direct consumer spending and increased cash and deposit balances, logged as deferred consumption (savings) at a time when substantial monetary stimulus accounted for much of the deviation in Figure 4 from the correlation between M3 and GDP.

Additionally, the US Treasury took the opportunity of increased public savings to overfund its deficit. This withdrew much of the increase in M3 temporarily from public circulation by growing the balance on its General Account at the Fed from under $400bn in March 2020 to $1,817bn only four months later. That increase of $1.4 trillion accounts for a significant portion of the $3.7 trillion dip in the grey line on the chart in Figure 4 for fiscal 2020. The subsequent unwinding of the General Account balance through government spending and disbursements into the economy reversed the initial effect, bolstering the GDP statistic, and effectively allowing it to reflect earlier monetary expansion.

To summarise, if you increase the quantity of currency and credit in circulation and allow for any changes in the circuitous routes between its issue and final deployment it approximates to the increase in nominal GDP.

A moment of further reflection confirms that this must be so, because in an economy where the quantity of currency and credit does not alter, irrespective of whether economic activity changes for the better or worse, being a currency total GDP cannot change. Whether existing currency and credit is deployed in changes in allocation between consumption or recycled as capital funded by savings and bank deposits is immaterial, as are changes in spending patterns on imports, so long as foreign payments balance — a condition of unchanged total money and credit. Therefore, increases in the GDP statistic can only reflect increases in the quantities of money and credit.

The only minor exceptions to this rule are changes in the level of hoarded currency, changes in the level of purchases of second-hand goods relative to the new, and changes in the levels of unrecorded and exempted activities, most of which are temporary factors.

These exceptions aside, we can expect changes in GDP, which starts from a previously existing higher level, to be closely tracked by changes in the broad money quantity. This is confirmed in Figure 4, even to the extent that the rapid expansion of M3 during the covid lockdowns have subsequently been fully reflected in the increase in GDP.[iii] This is illustrated by the grey line charting the difference. Admittedly, there was considerably greater variation in the quarterly statistics, but they have compensated each other on an annual basis.

The confirmation bias, whereby on the basis of a recovery in GDP monetary policy planners claim that economic activity has been rescued by their monetary stimulations, is clearly a statistical tautology. And through their ignorance the investment management industry, led by the mathematical economists, have also fallen for the delusion. They fail to question why, when the US economy effectively shut down for much of the US’s fiscal years straddling 2020/2021, GDP hardly reflected it on balance.

The consequences of monetary policy errors

This article has focused on two egregious errors behind monetary policy: the role of interest rates and the belief that increases in GDP mean anything other than monetary inflation. It is true that these are not the only errors driving monetary policy. Associated with the interest rate fallacy is the belief that price inflation can be managed by varying interest rates, a mistake concealed when the policy fails by merely suppressing the evidence, as Figure 2 above of official CPI shows, compared with Shadowstats.com’s version stripped of the statistical changes in calculation method.

The result is that almost everyone has been misled into believing that interest rate adjustments of a mere one or two percent will be sufficient to deal with “inflation”, incorrectly defined as rising prices.

Instead, the official definition of inflation is the consequence of unprecedented increases in quantities of currencies and credit. And it is not confined to just a few jurisdictions. Monetary expansion is common to the policies of all major central banks. Therefore, the purchasing powers of the dollar, euro, pound, yen, and yuan are coordinated, declining, and have further declines in prospect. Furthermore, with the dollar acting as all the other central banks’ currency standard, deviations into less inflationary monetary policies than those of the Fed are discouraged.

Measuring the consequences of policy errors through foreign exchange rate changes is therefore akin to betting which stone will sink fastest when thrown into the currency pool. Declines in purchasing power will become the dominant component of time preference for all these currencies. Any dispassionate analysis points to rises in the future discount rate for currencies being not reflected by interest rates of just a few percentage points, but by substantially more.

However, there is a growing but so far generally incoherent understanding that all is not right in the fiat currency world, epitomised by excessive speculation in cryptocurrencies. Fans of bitcoin and other cryptocurrencies are searching for protection from a currency condition they only partly understand. But they are ahead in the game of understanding what is happening to fiat currencies compared with earlier generations.

The sheer weight of excess currency, led by raw injections of new deposit money into investing institutions by the Fed, the Bank of England, the ECB, and the Bank of Japan, has driven financial asset values globally to unheard-of levels. The risk exposure to these asset values from the inevitable failure of monetary policy is most acute in dollar-denominated assets, ensuring that when interest rate increases are more correctly anticipated, the subsequent bear market will almost certainly be ubiquitous and substantial. And it is in dealing with this that the Fed’s erroneous belief that they can continue to issue new currency to support financial asset values will come back to bite the Fed’s policymakers, even if they acknowledge significantly higher interest rates instead of stopping the expansion of currency and credit.

i] This happened after Hayek wrote an essay criticising Keynes’s A Treatise on Money. See https://mises.org/library/reflections-pure-theory-money-mr-jm-keynes

[ii] See Keynes’s chapter on Concluding Notes, Section II in his The General Theory of Employment, Interest and Money where he claims that with the euthanasia of the rentier will come available through taxation the services of the entrepreneur more cheaply “because they are fond of their craft”.

[iii] M3 is no longer reported by the US monetary authorities, M2 being the widest official measure of money. But the OECD still estimates US M3 for purposes of international comparison.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.

*********

More from Gold-Eagle