Perhaps This Is Why Gold and Silver Have Begun to Outperform the Stock Market

The following analysis was featured in the September 25th issue of the Short Seller’s Journal. You can learn more about this newsletter here: Short Sellers Journal information.

A survey was done by CreditCards.com in which 60% of the respondents said that they have been in credit card debt for at least a year. That’s up from 50% a year ago. Forty percent said they’ve been in credit card debt for over two years. A quarter of those surveyed said that the reason they carry outstanding credit card debt is to cover daily expenses. The Fed’s July consumer credit report (it has a two-month lag) showed that credit card debt hit a record $4.64 trillion. It’s likely that credit card defaults are going to start shooting higher, causing increased stress on bank balance sheets and credit markets.

A couple weeks ago Goldman Sachs reported that the losses (bad debt write-offs) on its credit card business hit 2.93% in Q2. That’s the largest loss-rate among big credit card issuers (Goldman in recent years has made a big push into retail banking services). As it turns out, more that 25% of Goldman’s credit card loans have gone to people with sub-660 FICO scores.

See a trend here?:

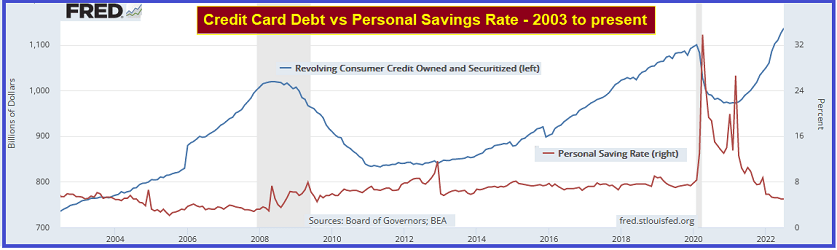

The chart above plots consumer credit card debt balances (blue line, left y-axis) vs the personal savings rate (red line, right y-axis). Credit card debt outstanding is at an all-time high, while the personal savings rate is at its lowest level since the great financial crisis. Keep in mind, though, that a significantly higher percentage of personal savings is with the upper 5% wealth/income demographic relative to the 2008/9 period. Also, the savings rate just after the virus lockdown was a product of the Government handouts in the form stimulus checks and PPP loans. The PPP loans were forgiven. The funds from those programs are now spent. Keep in mind that the savings rate metric is deceptive. The majority of the savings in the U.S. is attributable to the upper 5% income/wealth demographic – and really the upper 1%. How do we know? Because a Lending Club survey a few months ago showed that 23% of those making $250k or more were living paycheck to paycheck; no savings but they live in a fancy house and sport $100k SUVs and sedans in the driveway.

What stands out most to me in the chart above is that credit card debt levels explode relative to the savings rate when the financial markets and economy are entering a period of turmoil. I took the chart back to 2003. The same pattern occurred in 1998/1999 right before the tech bubble collapsed, but it’s not as pronounced because the money supply and outstanding household debt was diminutive relative to the post-tech stock crash period, when Greenspan juiced the money supply and encouraged all flavors of consumer borrowing.

Of course, over the next several months, escalating consumer debt losses will not be unique to Goldman. For point of reference, the overall credit card delinquency rate hit 2.7% in Q1 2020. At the peak in the financial crisis years, the delinquency/charge-off rate, according to Fed statistics, hit a peak of 6.77% outstanding balances in Q2 2009. I believe there’s a good chance it will be much worse this time around.

Moreover, the delinquency and default problem will not be confined to credit cards. Over the last few years, particularly since April 2020, households have stretched beyond rational limits and to assume auto loans and mortgages that many can barely afford and soon will no longer be able to afford. While Carmax’s big earnings miss and subsequent 25% drop in its stock grabbed the headlines on Friday, buried in its Q3 report was an increase in bad debt charge offs and an increase in the provision for credit losses. Carmax is not unique in this regard.

Brace yourself for the impact of a credit crisis that will be be far worse than the one that hit in 2008 – perhaps this is why gold and silver have begun to outperform the stock market.

********