Gold-Getters Garner Gains

share

share

share

share

share

share

share

share

share

share

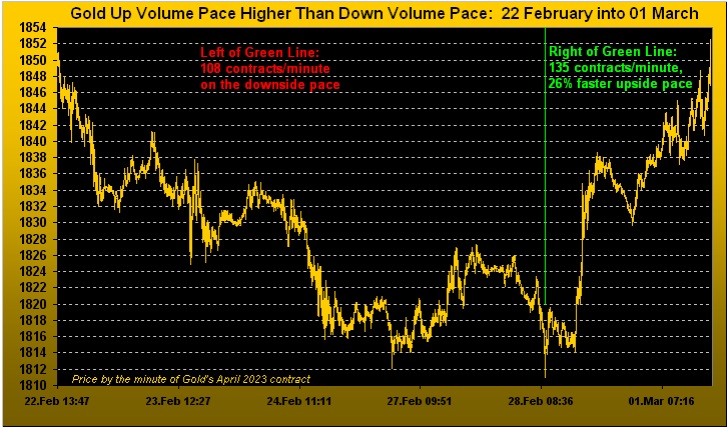

On the heels of last week's piece pointing to Gold (then 1818) as a "bargain", Gold-Getters have since come to the fore in pushing price to as high as 1864 towards settling yesterday (Friday) at 1863. That doesn't mean Gold has concluded testing our arbitrary 1851-1798 support zone that we've oft mentioned in recent missives. But 'tis Gold's upside volume pace which we now embrace. Here's the precise case:

After flirting with the 1851 level beginning on 15 February, come 22 February at precisely 13:47 CET, Gold slipped sub-1851 without looking back toward bottoming at 1811 this past Tuesday, 28 February at 09:17 CET. Across those 5,242 trading minutes, Gold's downside pace averaged 108 contracts/minute. However: in the swift race back up through just 1,779 minutes to regain the 1851 level the very next trading day on Wednesday, 01 March at 15:56 CET, Gold's upside pace averaged 135 contracts/minute.

Thus Gold's upside volume pace bettered that of the downside pace by +26%. How many times over these many years have we stated that -- unlike for other markets -- Gold tends to rise faster than it falls. And the Gold-Getters "get it". Encore, voilà:

"That's going deep into the data, mmb..."

But pretty cool, eh Squire? Because it reveals at least at present there is more interest in buying Gold than in selling it, even as the Federal Reserve looks to further the ascent of its interest rates. Even so, the Dollar is showing the earliest technical signs of at least some mild retrenchment which "ought" further buoy Gold.

'Course with so much market uncertainty, misvaluation and dislocation run amok these days, it can all turn on a dime. (Indeed for a dime back in the day you'd get 10 pieces of Bazooka bubble gum, i.e. at 1¢/piece; today, 1 piece costs 18¢, an increase of 1,700%, excluding the eventual cost of the dentist ... but we digress).

Instead let's digest Gold's weekly bars from one year ago-to-date. Does this recent dip into support and subsequent recovery suggest the current parabolic Short trend is short-lived? After all, 'tis but three red-dotted weeks thus far in duration, whereas the average length of the past 10 Short trends is 13 weeks. Yet that doesn't preclude there not having been a few brief Short-siders: four of the past 14 Short trends lasted five weeks or less. With price today (1863) some 96 points below the "flip to Long" price (1959) and Gold's "expected weekly trading range" now 52 points, two robust up weeks from here could end the Short trend with the 2000s then in the offing. Yes visually, 'tis a bit of a stretch, especially should any COMEX crushers be lurking about. But the green support zone in the graphic thus far is doing its job, as Gold from intraweek-low-to-settle sported its eighth-best gain in a year:

Moreover with respect to the Fed, Governor Christopher "Up the Wall" Waller this past week suggested that the Bank's rate hikes are not keeping pace with inflation, and that the StateSide job market is "unsustainably hot". One might opine the whole darn economy of late looks "hot":

And the standout star for the Economic Barometer this past week was January's Pending Home Sales rocketing up +8.1%, a 17-month best. Is America thus "on the move"? OR: is it cashing in so as not to lose? Mind that bubble gum price.

In less of a starring role however is the S&P 500, for which Q4 Earnings Season just concluded. Of the Index's 503 constituents, 471 reported within the seasonal timeframe, 60% of which improved their bottom lines over Q4 of a year ago ... thus not so did the other 40%. But let's drill a bit deeper: 451 did have positive earnings (regardless of whether or not they improved) which combined on a cap-weighted basis resulted in an overall Earnings Season gain of +2.7%. The Consumer Price Index year-over-year? +6.0%. The yield on the S&P itself? 1.698%. That annualized for the U.S. 3-month T-Bill? 4.718%. Think the stock market's way too high? The "live" price/earnings ratio for the S&P settled yesterday at 42.5x, nearly double the historical average to which the P/E always reverts. And Gold today (1863) is but half its Dollar debasement valuation. To reprise from above: "...so much market uncertainty, misvaluation and dislocation..."

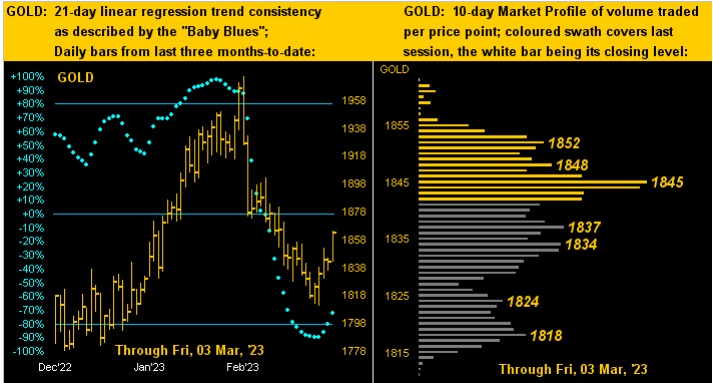

Meanwhile, from the "What a Difference a Week Makes Dept." we turn to Gold's two-panel graphic of the daily bars from three months ago-to-date on the left and 10-day Market Profile on the right. The baby blue dots of trend consistency are turning the corner, suggestive that the downtrend has reached its bend, whilst in the Profile, price has gone from worst to first, (the wee white nub at the top of the stack):

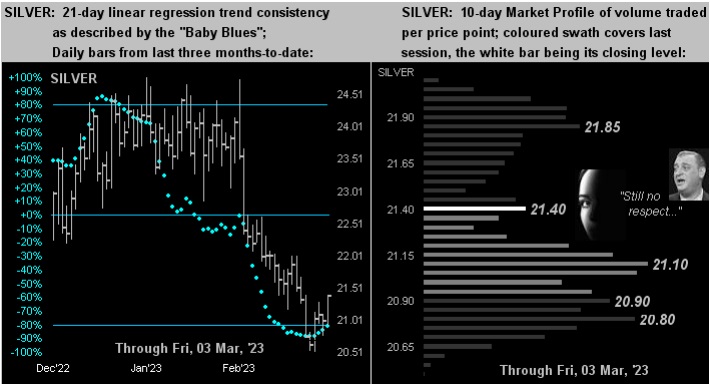

Having too improved, albeit struggling to so do, is Silver. At left her "Baby Blues" lack the more robust up-curl of those for Gold; and at right her price has ascended only halfway up through her Profile, the Gold/Silver ratio remaining excessively high at 87.1x. Poor ol' Sister Silver believes she's a distant relative of Rodney Dangerfield:

Regardless, 'twas a fairly robust week for Gold, with Silver somewhat in tow. 'Tis an added plus that this past week's up volume pace exceeded that of the down volume through Gold's testing of the support zone. And should Gold eclipse the mid-1870s in the new week, 1900 also is in range.

We'll wrap it here with this bemusement from our ever-popular "Others Parrot; We Do The Math Dept." This past Thursday, Dow Jones Newswires headlined with "Stocks and bonds are moving in tandem, something many investors have never seen", as sourced from an investment advisory firm.

REALLY? No surprise to our regular readers, since 2001 we've maintained rigorous correlation data amongst our five primary BEGOS Markets (Bond / Euro / Gold / Oil / S&P): we thus pulled up that for the Bond and the S&P. The truth across the 5,577 trading days century-to-date? Yes, the Bond and S&P are in negative correlation 61% of the time ... however that means they're in positive correlation 39% of the time. But the latter apparently is a phenomenon "many investors have never seen". Thus on rolls the Investing Age of Stoopid.

Cheers.

...m...

*********

share

share

share

share

share

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.