Inflation: Expected and Unexpected

share

share

share

share

share

share

share

share

share

share

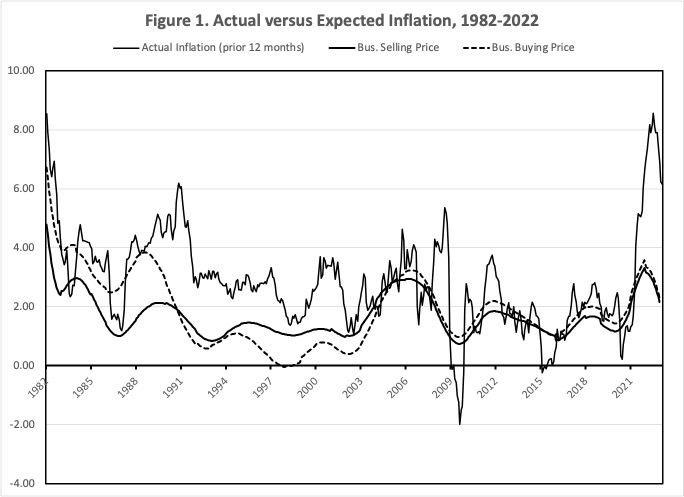

I've just completed my periodic update of business price expectations, including selling prices (the wavy solid line in the following chart) and buying prices (dashed line). I’ve juxtaposed these against actual inflation (the jagged solid line).

You will notice a big spurt of actual inflation, capping off at 8 percent. In contrast, the movement of business expected inflation has been muted, not even reaching 4 percent.

Supposing that it is business expected inflation that drives interest rates and wages, this means real prices have been affected by the spurt of actual inflation. Interest rates have been too low, and wage increases have not been enough to compensate workers for their loss of purchasing power. We can also suppose that there is a lot of catch-up inflation out there for the economy to work through.

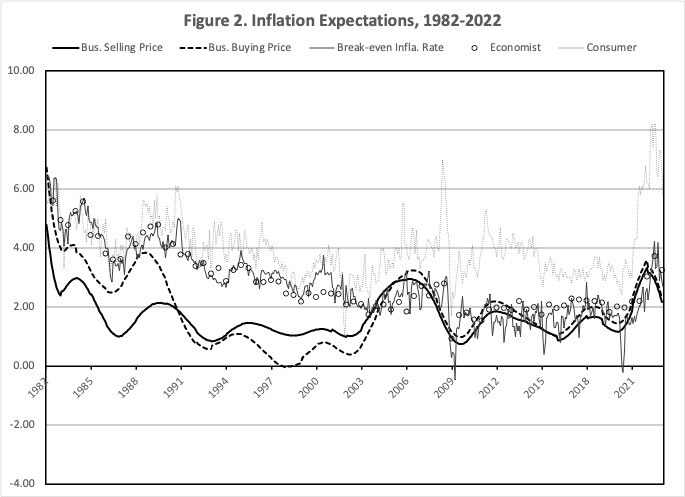

The next chart contrasts business inflation expectations to other expected inflation series. My series of business inflation expectations is based on an evolving set of surveys of business executives asking them – usually among a variety of things – about the near-term prospects for the prices of the goods and services they sell, and/or the prices of the goods and services they buy.

The “break-even inflation rate” is calculated by the Cleveland Federal Reserve Bank. It is the inflation rate that sets the yield on 1-year nominal US Treasury securities equal to the expected yield net of inflation on 1-year CPI-adjusted US Treasury securities.

Consumer expected inflation is the mean average expected inflation rate from the monthly survey of households conducted by the University of Michigan Survey Research Center.

Economist expected inflation is from the semi-annual survey of professional economists initiated by a financial journalist a long time ago, and continued by the Philadelphia Federal Reserve Bank.

A number of deviations are evident in these several inflation expectations series. Of immediate interest is that consumers were quite aware of the recent spurt of inflation, while business executives, professional economists and the financial markets were out to lunch.

Expectations may be rational, but this doesn’t mean they’re right. And, this doesn’t mean there won’t be hell to pay when they’re wrong.

Courtesy of AIER.org

Article originally published here.

*********

share

share

share

share

share