Polish Central Bank Buys Gold According to Secret EU Plan

share

share

share

share

share

share

share

share

share

share

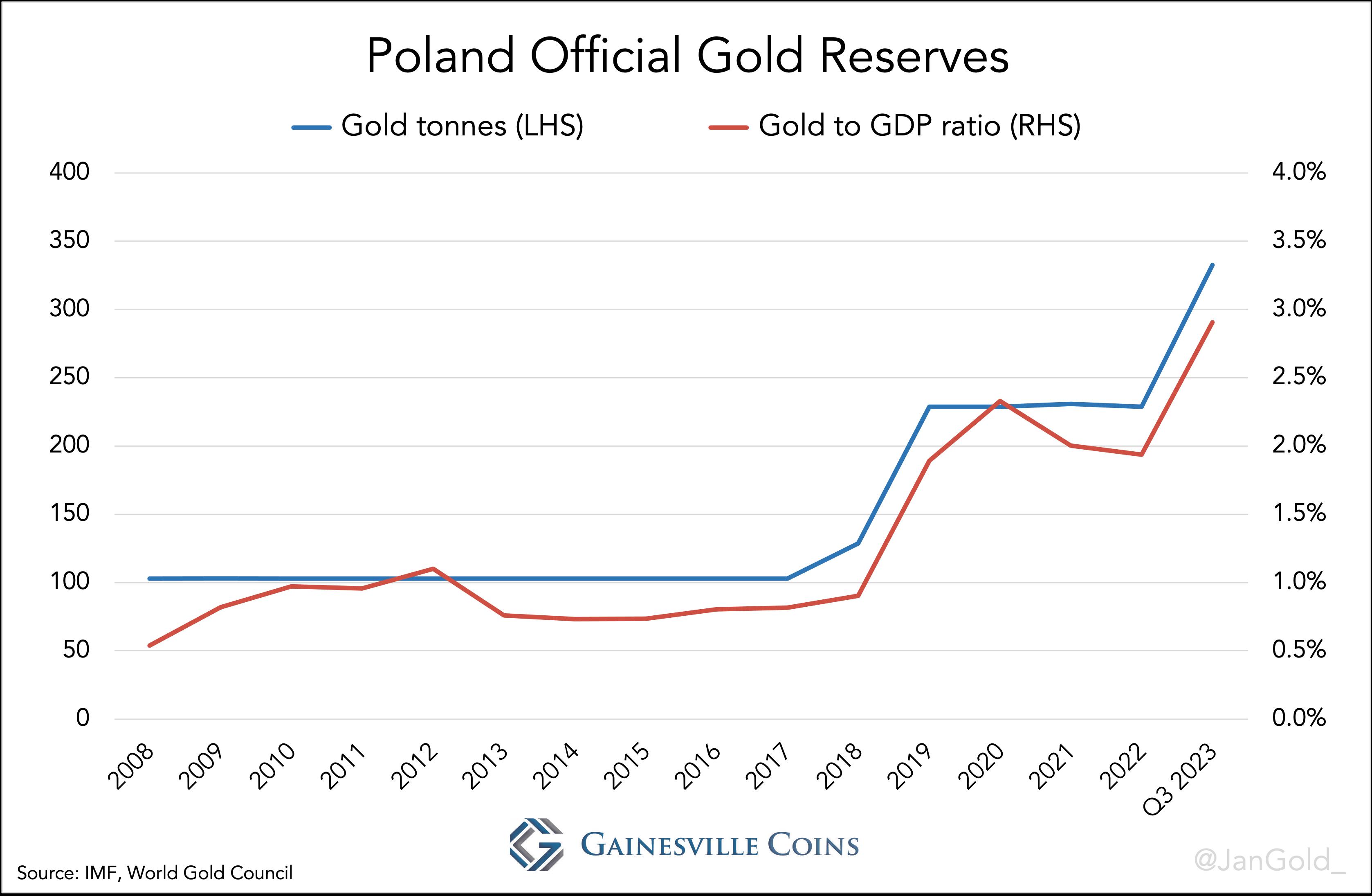

The Polish central bank has bought roughly 300 tons of gold in recent years to bring its gold to GDP ratio in line with the average in the eurozone. For medium and large economies in the eurozone, to which Poland might be included in the future, an equal monetary gold to GDP ratio is a covert requirement for nations to be prepared for a shift to a new gold standard. Based on these requirements I expect Poland to buy an additional 130 tons of gold.

View inside the gold vault of Narodowy Bank Polski (NBP).

Introduction

For those that don’t know, the idea in the European Union (EU) is that eventually all countries adopt the euro and become part of the eurozone. At the time of writing the EU counts 27 countries, of which 20 form the eurozone. When the remaining 7 countries will introduce the euro is unknown.

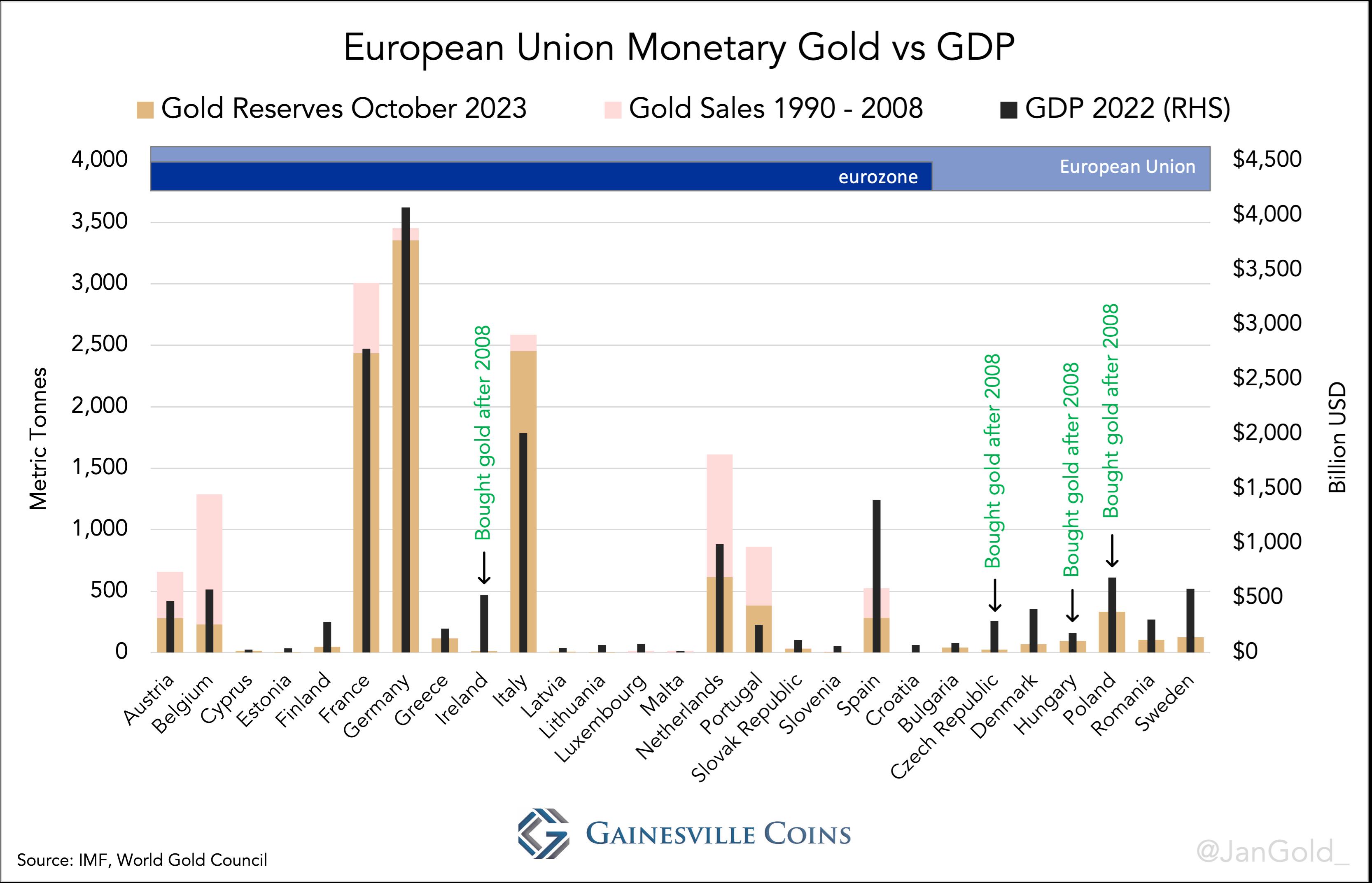

Within the EU most notably Poland—but also Hungary—has been a large buyer of gold in the past years. Poland and Hungary are not yet included in the eurozone. After my publications “Europe Has Been Preparing a Global Gold Standard Since the 1970s. Part 2” and “Dutch Central Bank Admits It Has Prepared for a New Gold Standard” it’s irrefutable that there are secret agreements between nations in the eurozone to align gold reserves relative to GDP to be prepared for a new gold standard (or gold price targeting system). For Poland to be included in the euro area it has to match its gold to GDP ratio with the eurozone average.

On one hand, the agreements I’m referring to are secretive because some central banks in the eurozone refuse to be transparent regarding gold reserve alignment on grounds of “professional secrecy” laws (Belgium). On the other hand, some of these central banks have spontaneously stated they determine the size of their bullion holdings based on the gold to GDP ratios of large economies in close proximity (the Netherlands).

Of concern to our present study is Poland, eligible for eurozone inclusion, that is buying large volumes of gold which reaffirms the existence of the agreements. Not only are European central banks slowly revealing their gold strategy informally, all actions taken substantiate this policy.

Data Shows EU Central Bank Balance Gold to GDP Ratios

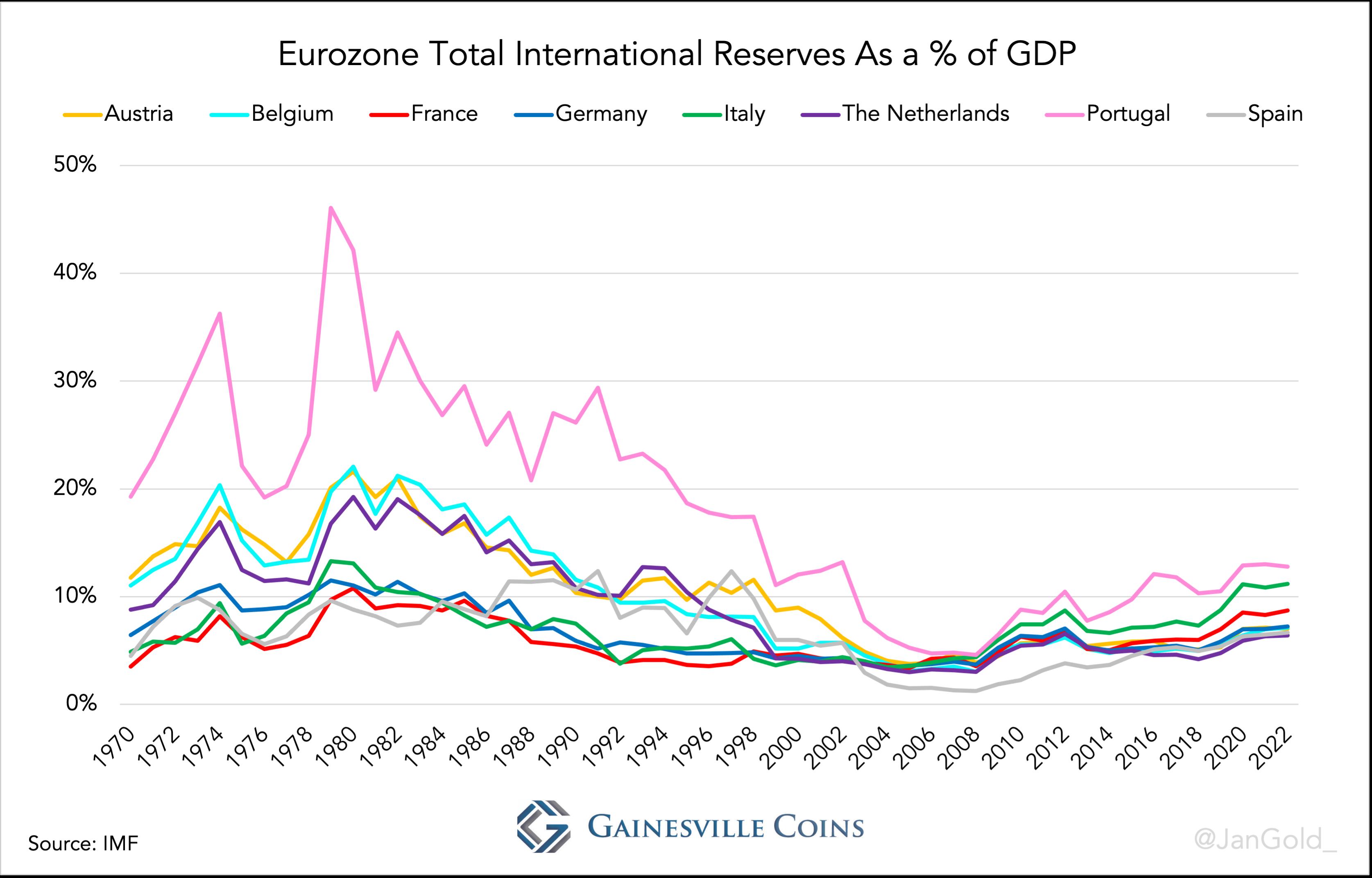

Last month a representative of the Dutch central bank (DNB) confessed in an interview that DNB holds gold worth about 4 percent of its GDP, which it has brought in line to the positions of France, Italy, and Germany. Bear in mind, the eurozone does not control the price of gold and thus their gold to GDP ratios, but there is a desire to harmonize these ratios throughout the eurozone, as illustrated in the chart below.

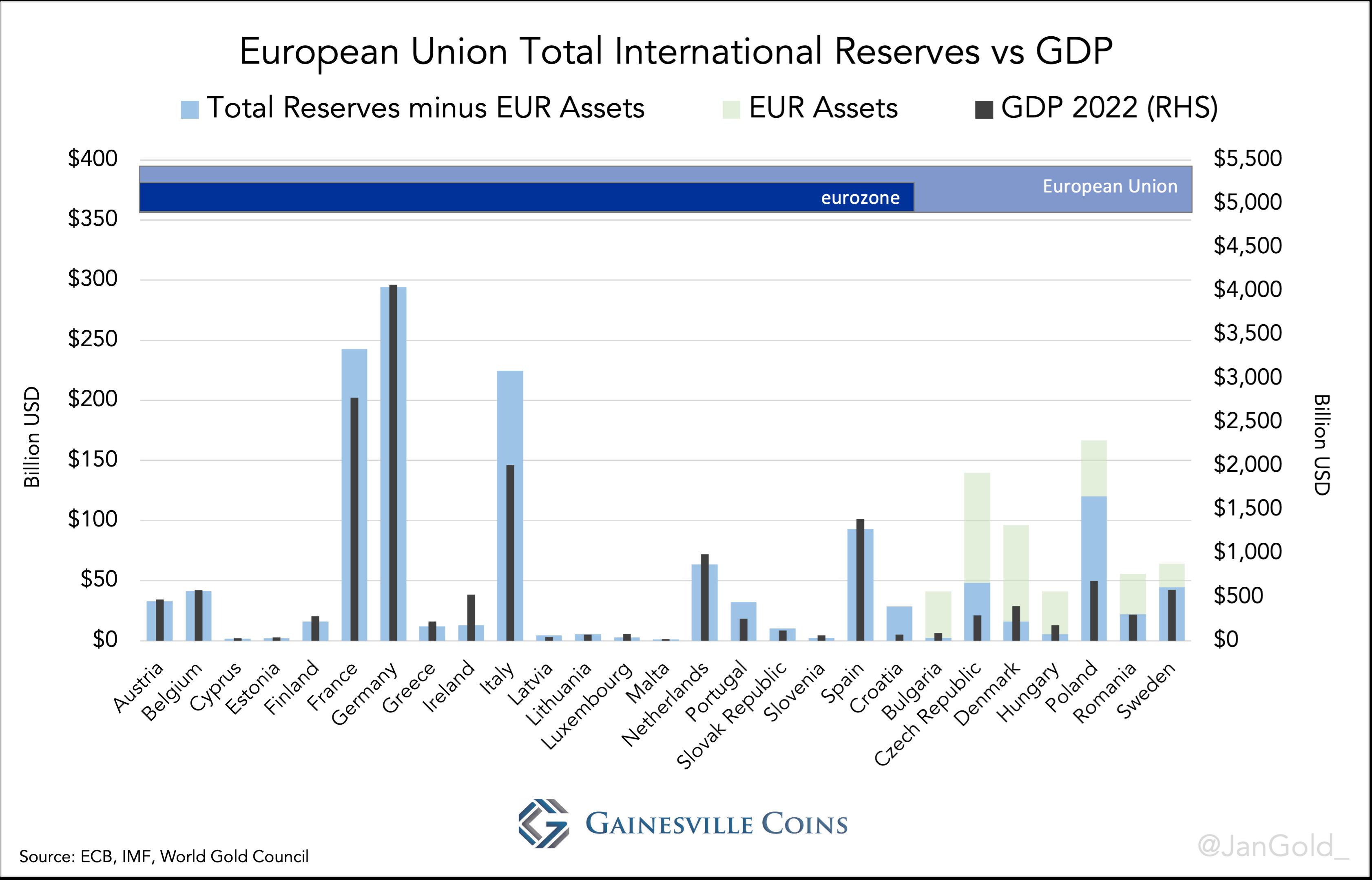

Supervision of total international reserves (gold and foreign exchange) versus GDP throughout the eurozone is even tighter. While European central banks have communicated that there are no legal obligations to coordinate reserves, they have likely agreed to recurrently use foreign exchange to equalize total reserves, and be able to exactly balance gold reserves among each other the very day they shift to a new gold standard. Periodically adjusting gold reserves is politically too sensitive.

It seems that countries within the EU but outside the eurozone (especially Romania and Sweden) are also coordinating their total reserves to GDP to ratios.

The precision with which total reserves to GDP ratios were equalized by eurozone central banks in 2008 is truly astonishing. Obviously, this has been meticulously planned.

Prior to 2017, Poland held 103 tonnes of monetary gold, which was just 1% of its GDP. To come on par with its European associates Poland needed to raise its metal reserves significantly and so it did: in 2018 the Polish central bank (NBP) started buying gold aggressively. By now it holds 334 tonnes, which is nearly 3% of Poland’s GDP.

As can be seen in the charts, Poland would need 450 tonnes to reach 4% of GDP, like its partners in the euro area. Additionally, NBP needs to transfer gold to the European Central Bank the moment it joins using the euro. According to my calculations that would be about 16 tonnes at the prevailing gold price. In total I expect NBP to buy another 130 tonnes.

Why Central Banks Harmonize Gold Reserves

In the late nineteenth century, as more countries joined the classical gold standard, demand for gold went up. On a gold standard, upward pressure on a country’s currency—as a result from increased demand for gold—created downward pressure on prices of goods and services denominated in that currency. Adoption of the gold standard involved deflationary forces.

The more skewed the current global distribution of official gold reserves, the less smooth a transition towards an international monetary system based on gold. Consequently, for every central bank that holds gold as its “Plan B” (a gold standard) there is an incentive to convince other central banks to do the same and balance the size of their bullion hoards among each other proportionally. So, when there is a severe financial crisis, which will fan out like wildfire in today’s intertwined markets, countries can stabilize their economies by shifting to a stable global gold standard. In my view, the majority of central banks are aware of this dynamic.

Click to watch the video.

Conclusion

Next to Poland, Hungary has increased its gold reserves substantially from 3 tonnes in 2017 (0.1% of GDP) to 94 tonnes in 2021 (3% of GDP). Tellingly, the Hungarian central bank commented that gold “may play a stabilising role and act as a major line of defense under extreme market conditions or in times of structural changes in the international financial system.” The Czech Republic is also buying of late, though its gold to GDP ratio is still far below the regional average. I wouldn’t be surprised if the Czechs buy an additional 150 tonnes in the years ahead.

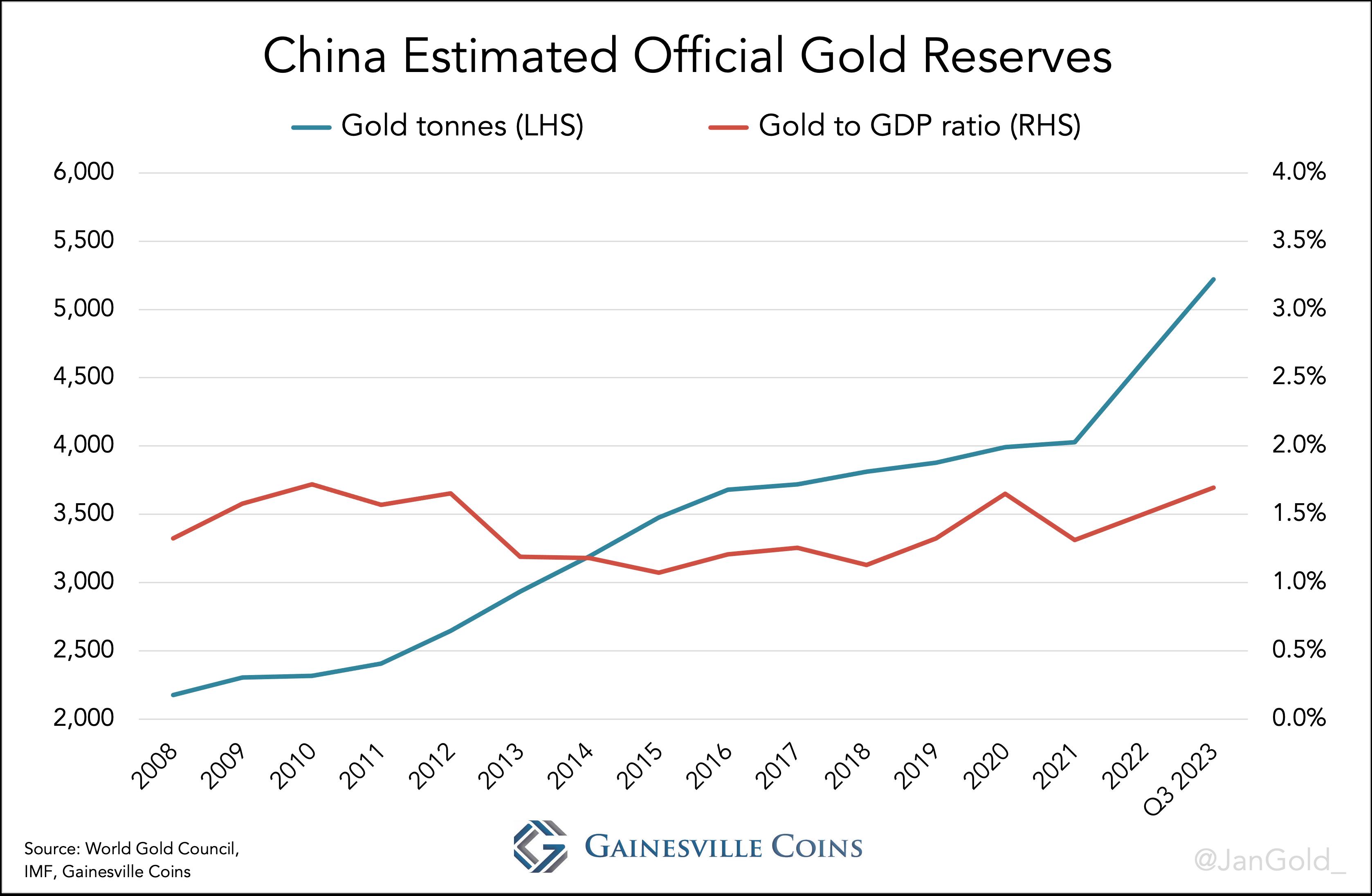

These developments are not likely to be limited to Europe. As I have demonstrated in previous analyses (here, here) China too is mindful of matching its official gold reserves to the size of its economy. According to my research, the Chinese central bank currently owns 5,220 tonnes of gold, which is worth almost 2% of its GDP. Perhaps this explains why the People’s Bank of China is buying gold hand over fist (approximately 700 tonnes annually) since the West froze Russia’s dollar assets. It needs to double its gold reserves and can't afford to wait.

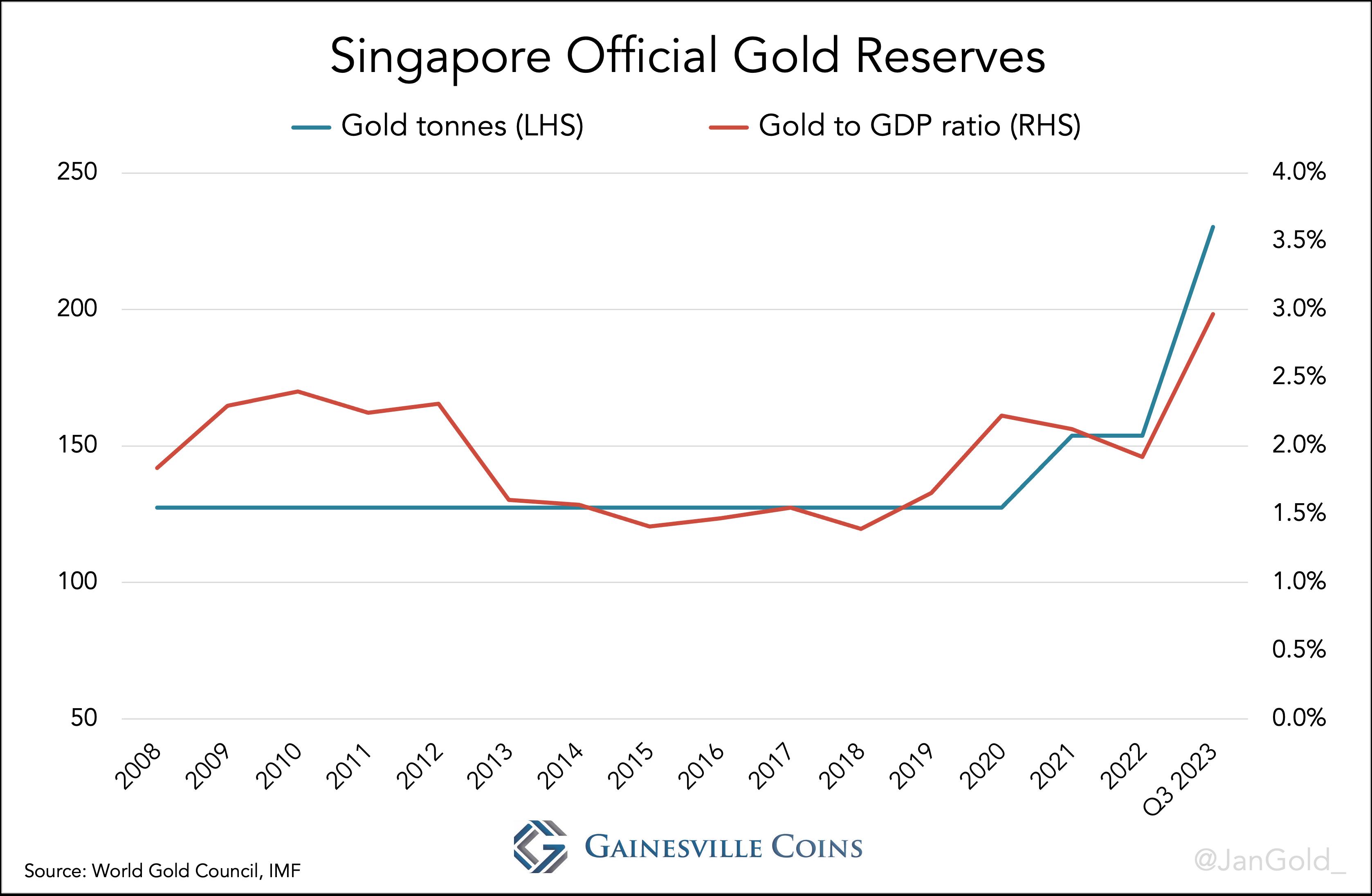

A test case is Singapore; another large buyer of gold since 2021 and seemingly trying to catch up as well. In 2018 Singapore’s monetary gold to GDP ratio was 1%, now it’s at 3%. It will be interesting to see if Singapore stops buying gold when it has reached 4% (or whatever the average ratio in the eurozone at any point in the future). I will keep you posted.

Courtesy of GainesvilleCoins.com. Article originally published here.

*********

share

share

share

share

share