Exceptionally Strong PBoC and Chinese Private Sector Buying Continues to Boost Gold Price

share

share

share

share

share

share

share

share

share

share

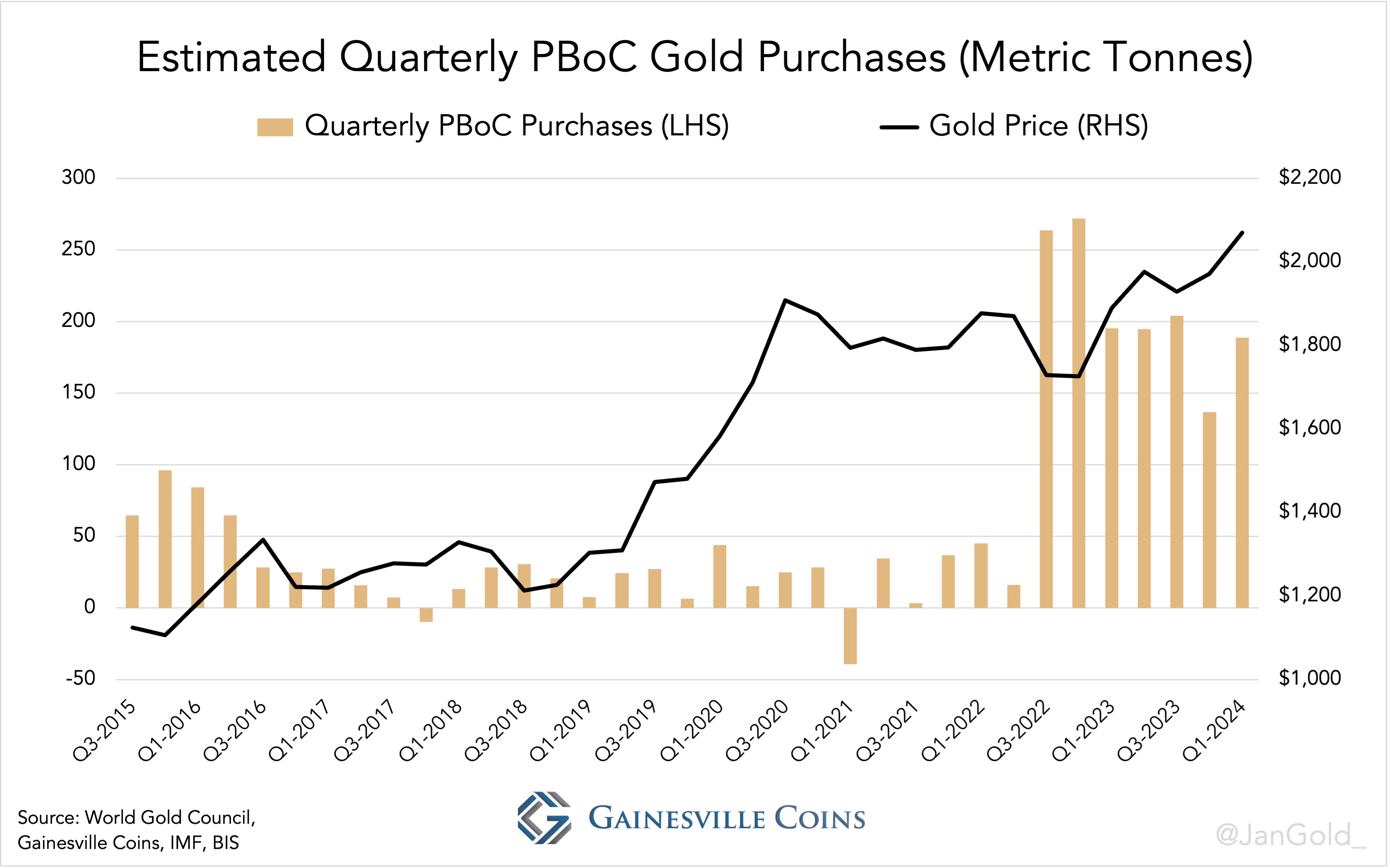

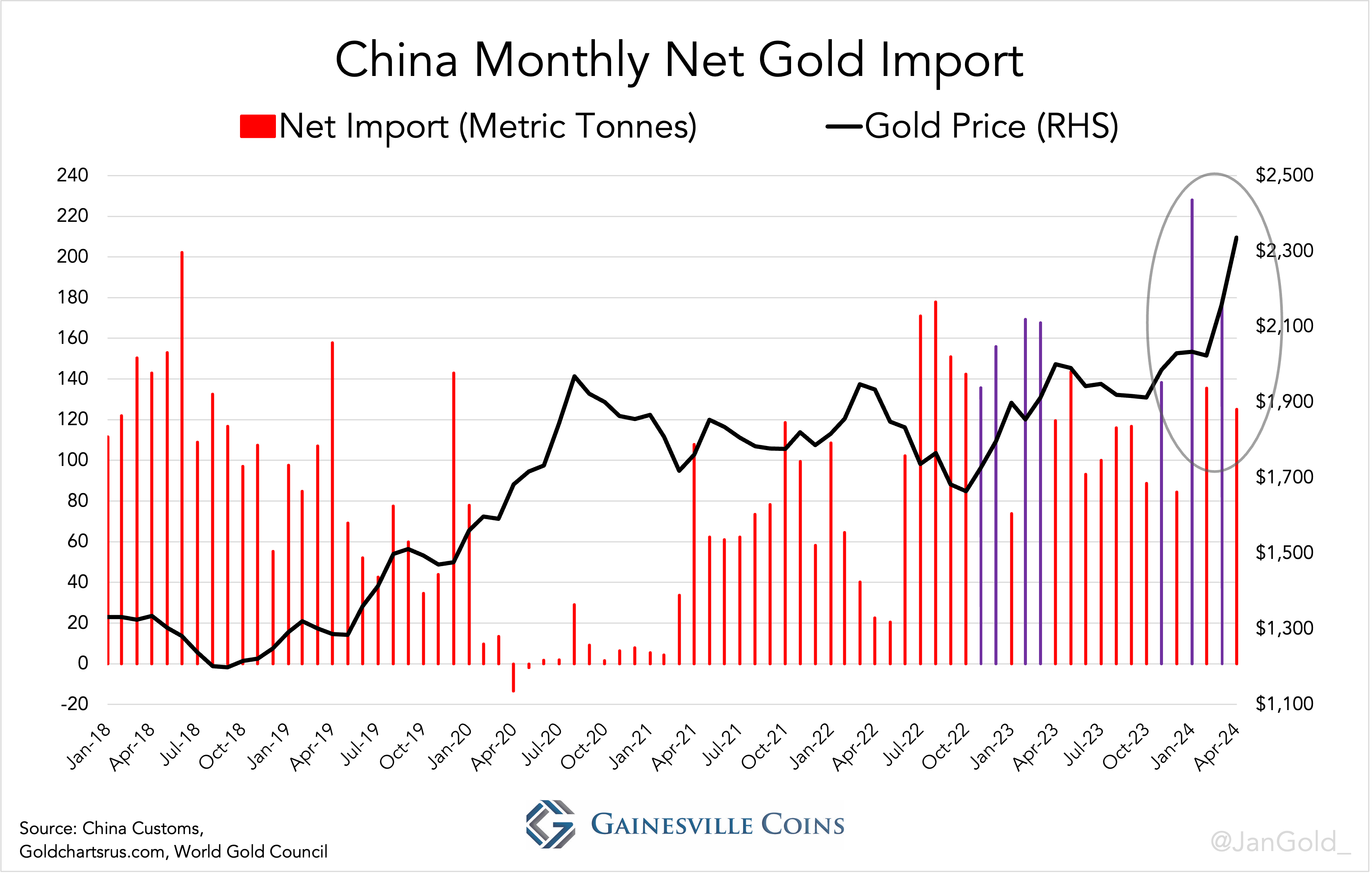

Chinese private sector gold imports accounted for 543 tonnes in the first quarter, while the People’s Bank of China (PBoC) added 189 tonnes to its reserves over this time horizon. Most of the PBoC’s purchases are “unreported.” China continues to be the marginal buyer in the gold market, driving up the price. I expect that China will remain a robust buyer of gold going forward in support of the price.

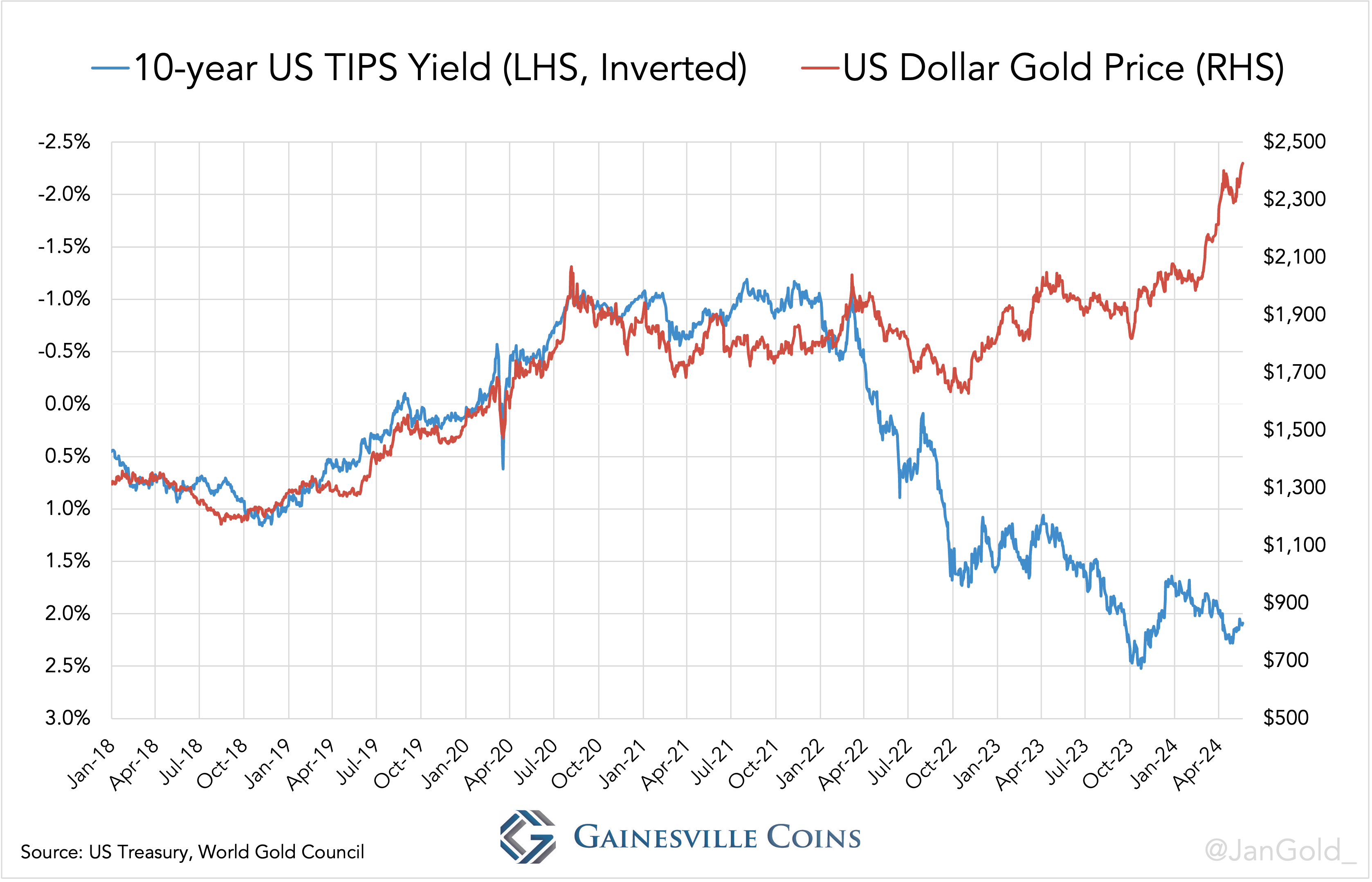

In my latest article on global gold flows from March 2024, “China Has Taken Over Gold Price Control from the West,” I showed that in 2022 China broke the peg between the US dollar gold price and “real yields.” Instead of being price sensitive China had become a driving force of the gold price. The data at my disposal ran until December 2023 which made me hesitant to conclude the sharp increase in the gold price since late February was also caused by the Chinese. However, as new data has been released, I can confidently say that China initiated the current bull market.

Chart 1. Dollar gold price versus real yields.

BoC Gold Buying Increased by 38% in Q1

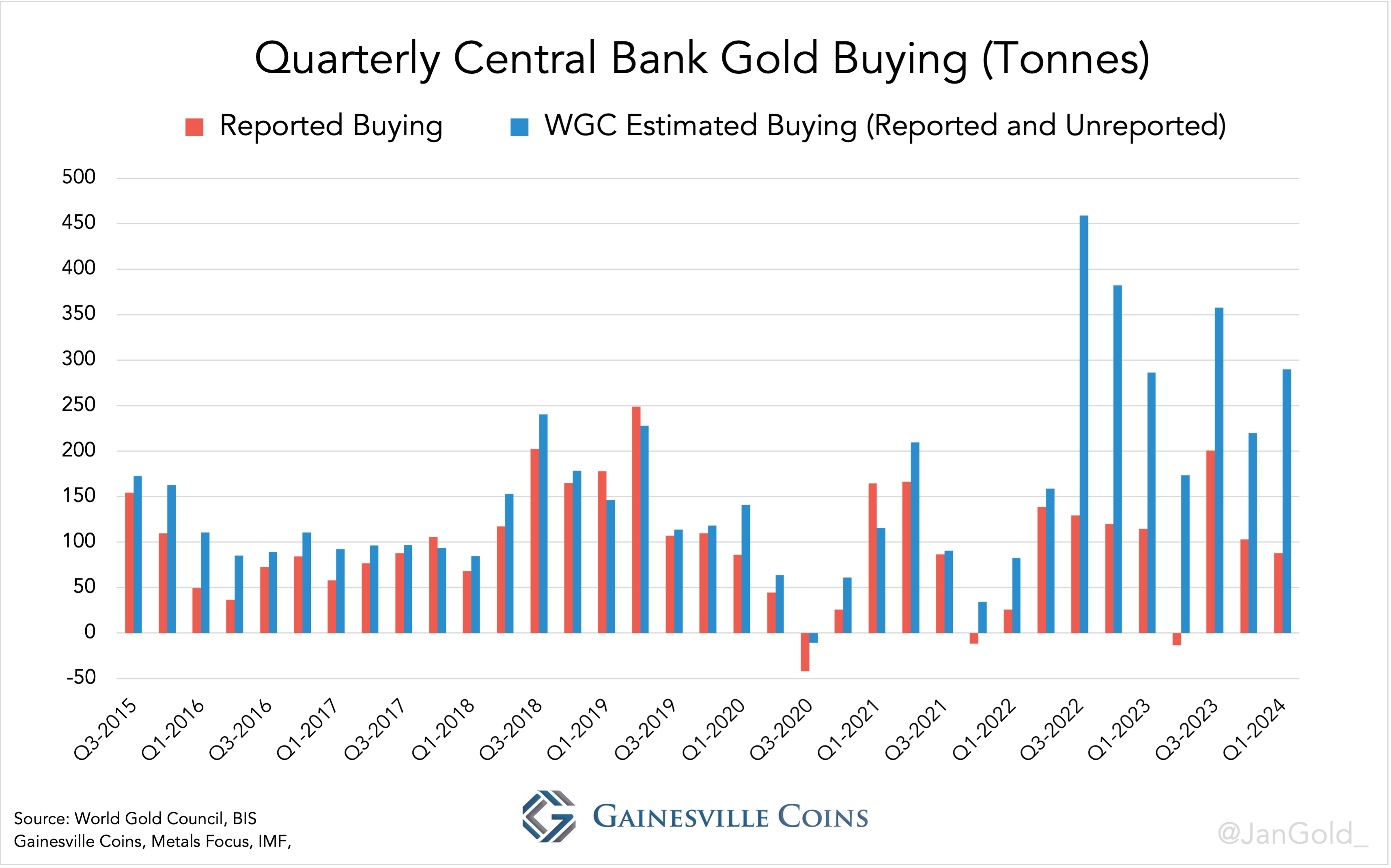

The media is aware that since 2022 central banks mostly buy gold covertly (often referred to as “unreported” purchases). By now it’s widely known that the World Gold Council (WGC) publishes a single statistic on aggregate central bank buying each quarter, which is markedly higher than what all monetary authorities combined report to have bought. Which central banks are causing the difference isn’t made clear though.

Chart 2. Quarterly central bank gold buying. Especially since the war in Ukraine (early 2022) the WGC’s estimates of central bank buying are much higher than what is reported by the IMF.

In February 2023 I broke the story on unreported buying being mostly acquisitions by the PBoC. Two people familiar with the matter shared with me the Chinese central bank is responsible for “the majority” of secretive additions by monetary authorities. Emerging markets such as Saudi Arabia take up the rest.

Based on field research, the WGC states central banks bought 290 tonnes of gold in the first quarter of 2024. Most of the difference—I use eighty percent—between the WGC’s estimate and total purchases as disclosed by the IMF is 162 tonnes. When we add what the PBoC has reported to have bought during this period, total purchases come in at 189 tonnes, 38% more than the previous quarter. Possibly, the PBoC had a stake in boosting the price since late February.

Chart 3. My estimated quarterly PBoC gold purchases (reported plus unreported).

Taking into account unreported purchases, the Chinese central bank now holds gold reserves weighing 5,542 tonnes, according to my research (my methodology is explained here).

Exceptionally Strong Chinese Private Gold Demand in Q1

Chinese net gold imports by the private sector have been extremely strong. From January through March imports accounted for a mammoth 543 tonnes, up 74% from Q4 2023. This is definitely what pushed up the gold price. Import in April decreased somewhat to 125 tonnes.

Chart 5. Chinese monthly net gold import. Purple bars show strong buying while the price goes up. Before 2022 the Chinese were price sensitive and only bought large tonnages when the West heavily sold and the price was weak.

India imported a healthful 95 tonnes in February, but less than 30 tonnes both in January and February. The Indians remain price sensitive and are not driving this rally.

Hong Kong saw notable net inflows in the past months, which mainly reflects strong demand in China in my view. Chinese housewives buy VAT free jewelry in Hong Kong and take it across the border to Shenzhen. In addition, bullion banks that export gold to China store gold in Hong Kong before re-exporting to the mainland.

In Q1 the UK and Switzerland both were net exporters, and Western ETF inventories declined. At the time of writing the West has not yet joined the bull market, which primarily has its roots in China.

Chinese Gold Demand Will Stay Powerful

Bloomberg recently reported that Beijing offloaded a record of $53 billion in US Treasuries and agency bonds combined in Q1, which illustrates the PBoC is selling dollars for gold. No wonder, as enthusiasm to seize Russia’s foreign exchange reserves—deposited at Belgium-based clearinghouse Euroclear—is rising among G-7 nations. In turn, Russia is freezing €700 million of assets from Western commercial banks such as UniCredit and Deutsche Bank, further strengthening gold’s global position as a safe haven. China’s foreign exchange reserves stand at $3.2 trillion so there is plenty of firepower left for gold.

Private gold demand in China is likely to uphold as well as the end of the property slump is not in sight. Home prices have declined in 30 out of the last 33 months. The State Council is floating a plan to buy unsold houses through local governments, but these are already drowning in debt. The Chinese public, which doesn’t have many investment options due to capital controls, will continue to invest in gold and support the price.

I’m expecting the West to join the bull market soon. ETF outflows appear to have stopped, and it would only be logical for Western investors to rotate into gold at some point because of high asset valuations and an overconfidence in credit instruments.

Courtesy of Gainesvillecoins.com and originally published here.

********

share

share

share

share

share

More from Gold-Eagle