Bad Ideas About Money, Bitcoin And Gold

share

share

share

share

share

share

share

share

share

share

Most false or irrational ideas about money are not new. For example, take the idea that government can just fix the price of one monetary asset against another. Some people think that we can have a gold standard by such a decree today. This idea goes back at least as far as the Coinage Act of 1792, when the government fixed 371.25 grains of silver to the same value as 24.75 grains of gold, or a ratio of 15 to 1. This caused problems because the market valued silver a bit lower than that.

So people were happy to bring their silver to the U.S. Mint to be coined. Silver had a higher value as a coin than it did in the market, and it was the opposite for gold. Gresham’s Law teaches us that if two monies must be treated by law as the same value, then the one of lower value will circulate and the one of higher value will be hoarded. This put the fledging America on a de facto silver standard.

Or, bad ideas have their roots in historical precedent but something is lost (or sabotaged) along the way. Back in 1792, there was no question that money meant gold and silver. There was no question that, when you deposited money at a bank, you had a right to get the same amount of money back. However, if each bank had a different unit of deposit, it would be hard to understand if someone said “I will pay you ten dollars”. Is that ten Road Runner Bank Dollars or ten Bank of Wile Coyote dollars?

The Coinage Act standardized the unit, but it did not change the rights of depositors or the obligations of banks. However, today, many people think that the government can, post hoc, change the definition of a unit and thereby change the value of everyone’s debt obligations and bank balances (and presumably cause a repricing of every extant asset).

We see this in many discussions of China’s future monetary policy. Many gold bugs have said that China will announce a gold-backed yuan. No one can know what a government may do in the future, but we can say in principle that it is impossible to fix the price of gold in yuan (or dollars or anything else). We can say that it won’t work if they try to change the value of the yuan by simple changes of law.

Another bad idea today traces itself back centuries. People use the paper bank note (and now electronic credit) as the equivalent of money for most situations, such as making a payment. Back in 1792, everyone understood that the paper note was redeemable for money. If you went to a bank, and pushed a twenty dollar bill over the counter, you would get just over 1 ounce in gold coins.

So long as the banks are trustworthy, few people have a reason to redeem their paper and withdraw their coins. So most become comfortable with the idea of paper bills. They may even begin to think of it as money. However, the concept of money cannot be entirely forgotten, so long as redemption occurs every day. If you redeem paper to get gold, can you call the paper “money”? If the paper is money, and you’re turning it in to get gold, then what is the word for the gold? In a system where redemption is possible, people are clear that the paper is currency and the gold is the money. No one would imagine redeeming money for … __________? (We literally cannot think of what word would go in the blank.)

Going further, another idea is that it’s OK if a bank note is not redeemable, so long as the backing is there. This idea became policy in 1933. The government redefined the dollar, from 1/20 ounce of gold to 1/35. Just like that, the people were left with bank notes but not money. Per the Stockholm Syndrome, they came to at last think of the paper as money. If paper bank notes worked as money previously, then no reason to worry if they will stop working.

At the same time, every creditor was made poorer and every debtor was made richer. That is what, in fact, decreeing a change in value does. As economist John Maynard Keynes wrote (citing Vladimir Lenin):

…the real value of the currency fluctuates wildly from month to month, all permanent relations between debtors and creditors, which form the ultimate foundation of capitalism, become so utterly disordered as to be almost meaningless; and the process of wealth-getting degenerates into a gamble and a lottery.

The bad guys 100 years ago understood something that most good guys today do not. Distort, pervert, undermine, and destroy the relationship between creditor and debtor at your peril. Whether you realize it, or not, the stakes are nothing less than capitalism. Lenin knew it, and hoped to use it to usher in his utopia where he could get away with mass murder on an unprecedented scale.

This point relates to our ongoing theme of bitcoin. Bitcoin’s value is, to say the least, fluctuating. Lenin aptly described it: “the process of wealth-getting degenerates into a gamble and a lottery.” With such value fluctuation, bitcoin is manifestly unsuitable for lending and borrowing. When instability comes to the legal tender paper currency, people are surprised and may not have an alternative. But with bitcoin, they can see it in advance. Checking back at Bitbond, we now see two bitcoin loan requests. Both are bitcoin miners, and the total between both loans is ฿9.3.

And note the final and most important connection between the bad idea that bitcoin is money and ideas that recur in history. In 1933, the US government forced all citizens to treat irredeemable paper as if it were money. There was still some gold in the monetary system, though no longer moving, no longer deposited and redeemed. But in 1971, the government finished off gold. The dollar was declared to be purely irredeemable, and this rippled through to all other paper currencies.

We have now had about two generations for this to seep into our culture, our souls, our sense of How Things Are. Money means irredeemable paper, and irredeemable paper is money. All Right-Thinking people know this. Try a Google Images search on the term money, to see what we mean.

With the idea of redemption of paper for money taken off the table, where next will people go? What new distortion can be manufactured for fun and profit?

The dollar is borrowed into existence. It is backed, but only by debt and that debt is payable only in dollars. There is something there, but it’s circular. The next logical progression is to remove the backing, which is what bitcoin is. To pugnaciously put a chip on one’s shoulder, daring anyone to knock it off—to say that a currency printed into existence, printed ex nihilo out of thin air (albeit at a metered rate and with a maximum limit) is money.

Bitcoin is a liability of its issuer, without any asset to balance it. It is a currency believed to be money because there is no asset. Many who rightly attack the dollar as debt-based money, seem happy with bitcoin because the debt backing it is removed.

The central banks have taught us well. They have trained us to think of money as the piece of paper which once redeemed for it, the electronic balance which once represented it. So why not experiment with removing all that?

If by now, you are picturing a cargo cult, that’s precisely right. The cargo cults that sprang up on Pacific islands after WWII would go through elaborate motions that they thought would bring the cargo just as they observed the US military do. Of course, they substituted coconut shells tied with vine for headsets, and tiki torches for flashlights. And they had no radios, and no airplanes to call on those radios they didn’t have. They simply had faith that appearances could cause the magic effect they wanted.

Bitcoin is carefully designed to appear just like an irredeemable government-issued currency. Which is carefully designed to appear just like a gold-redeemable government-issued currency. Which was carefully designed to appear just like a bank-issued gold-redeemable bank note. Each is a deliberate adulteration, to the final one with bitcoin today.

Having indoctrinated people to accept irredeemable currency, the Fed has opened the door for bitcoin. In a way, bitcoin is a perfect denizen in the Fed’s worldwide regime of irredeemable currency. That is, a regime where each printed promise to pay has fine print saying “this promise will not be honored”. So why not substitute it with “this is not even a dishonored promise” and see how it flies.

The philosophy of postmodernism seeks to “deconstruct” truth. A fitting money of postmodernisn, would be “deconstructed” too. Like bitcoin.

P.S. We have chosen to focus our case on the monetary theory of bitcoin. We do not want to rest our argument on the risks that its price will crash, its encryption algorithm will be cracked, or its user accounts will be embezzled. If we address price, it is not to equate “bitcoin is bad” with “price will fall”, but to observe that unstable value makes it unsuitable for saving and borrowing.

P.P.S. However, it is worth saying something we have not seen elsewhere. Everyone knows that bitcoin has a strict limit of 21 million. However, this limit can of course be changed by a majority of the bitcoin miners. Miners, of course, profit by mining, so they may have an incentive to increase this limit. The way Congress has an incentive to increase the debt limit.

The price of gold was up nine bucks, and that of silver 6 cents. These small changes mask the relatively big drop on Tuesday—$13 in gold and $0.48 in silver—and recovery the rest of the week. The gains above last week’s occurred on Tuesday.

The question is which move is driven by fundamentals, and which is by speculation against the trend? We will show graphs of the basis, the true measure of the fundamentals.

But first, here are the charts of the prices of gold and silver, and the gold-silver ratio.

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio. The ratio moved up slightly this week.

In this graph, we show both bid and offer prices for the gold-silver ratio. If you were to sell gold on the bid and buy silver at the ask, that is the lower bid price. Conversely, if you sold silver on the bid and bought gold at the offer, that is the higher offer price.

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

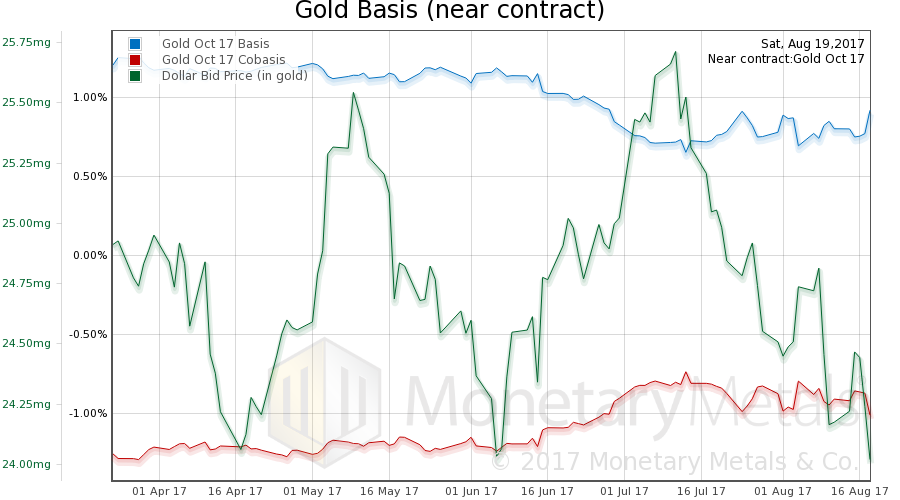

Here is the gold graph.

The dollar fell this week (the mirror image of the rising price of gold), now down to 24mg gold. And the basis rose a bit, another 12bps on top of the 11bps move last week.

Our calculated gold fundamental price dropped about $17 (chart here). So the market price is rising, and the fundamental price is still above the market price by about $31. A big change from last week when the fundamental was $57 over market.

Now let’s look at silver.

In silver, the price did not move much. However, the basis jumped up 22bps (against the pressures of the contract roll which is ongoing). The continuous silver basis, which is not subject to contract roll pressures, also jumped 21bps.

So it should be no surprise that our calculated silver fundamental fell $0.50 (chart here). The fundamental is now below the market price (though not a lot).

Two weeks ago, we asked:

So is the silver selloff over?

Now it is time to ask if the silver buy-up is over.

Last week, we noted:

One thing is for sure. If the fundamentals don’t continue to firm up further, or at least hold at the present level, then this rally is doomed like all of the others in the last 6 years.

© 2017 Monetary Metals

share

share

share

share

share

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.

Dr. Keith Weiner is the CEO of Monetary Metals and the president of the Gold Standard Institute USA. Keith is a leading authority in the areas of gold, money, and credit and has made important contributions to the development of trading techniques founded upon the analysis of bid-ask spreads. Keith is a sought after speaker and regularly writes on economics. He is an Objectivist, and has his PhD from the New Austrian School of Economics. His website is www.monetary-metals.com.