The Inflation Train is Arriving on Schedule, and the Labor Train is Departing

The Fed’s financial plans are running off the rails already. With summer just gone by and the Fed’s first rate cut barely out of the station, already the bond vigilantes are pushing bond interest rates back up, and voting Fed members are already talking about stalling their future rate cuts—all due to inflation being back on the rise. The timing of inflation’s arrival is as I expected, but it is not at all what the Fed was hoping to see.

Bond investors are referred to as “vigilantes” when they bring true justice to interest rates by going in the opposite direct of what the Fed intends because keeping the market in sync with reality demands it. They do this when they smell inflation stinking up the air like a dead rat in the walls of the house because they don’t want to lose to inflation as they wait to maturity to get their money back out of bonds.

The Fed is looking to create a little slack in the economy to ease into a soft landing. The bond vigilantes have done the opposite and tightened it up the most in months, taking the 10YR Treasury bond back above 4% and holding it there, and the 10YR is a foundational basis for many market interest rates that are marked up off of that rate.

As economist Wolf Richter wrote yesterday, the “bond market smells a rat.” The 43 basis-point interest rise in bonds almost matches up to the 50 basis-point mega interest cut just initiated by the Fed. Of course, bonds are not rising just due to perceived inflation risks running up but also due to the obvious fact that the US government, no matter which party wins, plans to keep issuing massive numbers of new bonds as far as the eye can see to finance its out-of-control debt.

Both presidential candidates are pushing for policies that will keep the government’s annual deficits deep in the red for their entire terms (which is one of many reasons I don’t like either candidate, as both are irresponsibly harming the nation just to get elected by throwing out candy to their children).

We’ll go into the detailed facts regarding all of this in the upcoming Deeper Dive, but today’s reports have already pushed the 10YR yield past 4.1% today, which provided enough of a jolt in vigilante justice for Atlanta Federal Reserve President Raphael Bostic to announce he would be open to a pause in the Fed’s rate cuts.

The news followed a slightly hotter-than-expected inflation report. The consumer price index increased 0.2% in September and 2.4% year-over-year, above economists’ estimates of a 0.1% increase on a monthly basis, and a 2.3% advance over the prior 12 months

Labor is no longer riding the gravy train

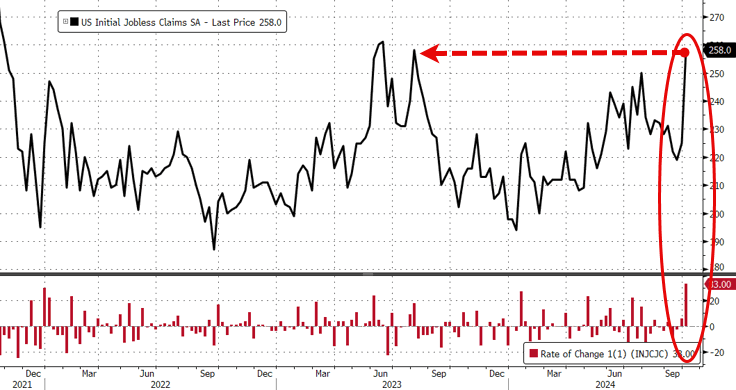

Jobless claims also made an unexpected advance as labor left the station. Was the last government report that pushed the unemployment rate down just another head fake due to broken metrics, or was it the result of corrupt electioneering, and we’re just getting to where it is hard to jury-rig the numbers enough to get them where Biden and Harris want them. I made a case for the latter in my last Deeper Dive. At any rate, labor continues to writhe up and down:

Initial filings for unemployment benefits rose to 258,000 for the week ending Oct. 5, the highest since August 2023.

This is lining up right along the pattern I proposed we could expect: Inflation would start to rise by the end of summer and would imperil the Fed’s rate cuts. Those cuts, which the Fed is reluctant to backtrack and lose face on on now that unemployment is rising, would imperil the Fed’s inflation fight. The Fed gets stuck in a bind.

In fairness, just as I refused to throw in the towel when the last job report looked to almost everyone like the Fed had scored its soft landing, making me wrong on a major claim, I also refuse to make any big claim on behalf of my predictions out of today’s turn away from a soft landing. It is merely proof that my predictions for this year are still very much in play. The reports are far from proof the Fed has failed or that I was right.

Zero Hedge has taken the same point of view as I have about the last optimistic job report prior to the present one (as being more of an election report than a true job report), and they do so again today:

Having exposed the total decoupling from reality in initial claims recently (near multi-decade lows despite surging job cuts, weak labor market survey indicators, and higher unemployment rates), last week saw the numbers provided by the government suddenly explode higher (by the most since July 2021) to the highest since August 2023 (258k)...

To represent that claim, they present the following graph:

It’s a little hard to believe the prior labor report that showed unemployment falling back below the critical recessionary level of the Sahm-Rule I’ve been talking about when initial jobless claims are soaring and when the Sahm Rule has never been wrong. That, too, smells like a dead rat in the wall somewhere, reinforcing what I wrote in my last Deeper Dive.

Continuing jobless claims also spiked from 1.816mm to 1.861mm Americans.…

Well then, so much for falling unemployment.

So—to summarize—inflation printed way hotter than expected this morning and the labor market indicators crashed—good luck with that stagflationary malarkey Mr. Powell.

Powell had said, just prior to delivering his big rate cut, that he could not see either the “stag” or the “flation” that people were fearing. I’ve said, to the contrary, stagflation is exactly where we’re going (actually, where we are), and it’s not that hard to see. Powell may have to rethink those words as much as he had to rethink his “inflation is transitory” narrative. The only thing transitory about this inflation has been Powell’s opinion about it. It looks like another solid face plant could be in store, but we’ll have to wait and see.

Of course, The Fed will likely shrug off the claims surge as 'localized' and 'transitory'...

They’re going to have to find a new word. The old one isn’t going to fly very well this time. It will work more like a triggering word if people hear Powell say it again; so one more thing I’ll predict is that you won’t hear him say it because he knows what ridicule will come. How he will rephrase what we are about to see, is a mystery; but he’ll have to find a way to couch it in other terms and try not to call on anyone who will bring the old “transitory” claim back up. Good luck with that. Even with the mainstream media being his friend, it has to look a little like it cares about and sees what is going on.

Neither the return of inflation nor the sudden return to rising unemployment, as the train jolted out of the station right after everyone was talking “soft landing scored,” are likely to be transitory. To his credit back then, Powell was reluctant to accept the claim that his soft landing had been achieved. I’m sure he’s well aware of how quickly that could flip on him.

I’ll likely dig more into the details in this inflation report and jobs report that strengthen my thesis on both subjects in this weekend’s Deeper Dive as I did last week, but the main point here is that the jury is clearly still out, and there is plenty of concern, even among Fed members, that their rate cut already isn’t going as they hoped. Obviously, a reversal of their interest cuts is a face plant they would be loathe to take, so they won’t go that far until it’s way too late.

“The Fed has shown that they’re willing to let inflation potentially run hotter than normal in favor of full employment,” said Skyler Weinand, chief investment officer at Regan Capital. ”Only a rise towards 4% inflation or a few hot inflation prints in a row would alter the Fed’s course of continued rate cuts over the next year.”

Which means the Fed response that is more likely to happen is that it will just pause rate cuts, which means it will hold too long on making that reversal, even if that drives inflation up more, repeating exactly the kind of mistake it made last time when it kept stimulus rates in place too long while inflation was rising.

If the Fed refuses to take the face plant, this inflation may bite its members’ faces off for them. We’ll look at the details in the report I’ll be putting tougher tomorrow for this weekend. For today, I’ll close by noting that clearly neither stock investors nor bond investors were happy with what they saw. That, too, is in the headlines that follow:

“Clearly today is being driven mostly by the CPI report,” said Luke O’Neill, portfolio manager at CooksonPeirce. “Not a huge surprise in most respects, but some of the underlying data is clearly a little bit hotter than anyone would prefer. On the margins, people are selling off small and mid cap stocks that are a little bit more rate sensitive….”

There are caveats, of course:

A separate report Thursday showed weekly jobless claims hitting a 14-month high, indicating potential softness in the labor market despite the big jump in nonfarm payrolls in September. However, most of the surge could be tied to the hurricane and strike.

Striking workers are not generally eligible for unemployment, so I’m not sure how the Boeing strike could cause an anomalous rise in approved unemployment claims; but that is the answer the mainstream financial press is desperately offering on the Fed’s behalf. After all, the liberal media wouldn’t want the Biden administration to lose face on the benefits of “Build Back Better” now that the costs of BBB are certainly apparent. (The hurricane, of course, could be to blame for the rise.)

“The market is bouncing around based on the fact that inflation seems to be reaccelerating, and you wonder if we will see the Fed pause,” said Chris Marinac, research director at Janney Montgomery Scott, in an interview. “That’s my struggle.”

So, the jury is clearly still out, and we’ll look into the details to see if rising unemployment is a one-off due to Hurricane Helene or if it is made up of elements there are likely to stick around or even grow worse. Likewise with rising inflation pressures.

********

David Haggith publishes The Daily Doom and writes satire. The Daily Doom contains economic, social, and political news about our troubled times--a non partisan weekday collection of the most consequential stories about our complex times with insightful editorials and weekly economic analysis. As an equal-opportunity critic of America's sharply divided, two-ring political circus, David divides his satire into sister publications so you can pick the one you find agreeable and ignore her sassy sister.

Support David Haggith by subscribing on Substack.