All Signs Point to the Early Stages of a New “Commodity Supercycle”

share

share

share

share

share

share

share

share

share

share

The idea that commodity markets can only yield short-term gains isn’t entirely accurate. During a commodities supercycle, investors can still expect long-term gains of a similar nature, and volatility, to equities.

What Are Commodity Supercycles?

A “commodity supercycle” is commonly described as a period of consistent and sustained price increases lasting more than five years, and in some cases, decades. The Bank of Canada defines it as an “extended period during which commodity prices are well above or below their long-run trend.”

Supercycles occur because of the long lag between commodity price signals and changes in supply. While each commodity is different, the following is a rundown of a typical boom-bust cycle:

As economies grow, so does the demand for commodities, and eventually the demand would outstrip supply. That leads to rising commodity prices, but the commodity producers don’t initially respond to the higher prices because they’re unsure whether they will last. As a result, the gap between demand and supply continues to widen, keeping upward pressure on prices.

Eventually, prices get so attractive that producers respond by making additional investments to boost supply, narrowing the supply and demand gap. High prices continue to encourage investment until finally, supply overtakes demand, pushing prices down. But even as prices fall, supply continues to rise as investments made during the boom years bear fruit. Shortages turn to gluts and commodities enter the bearish part of the cycle.

In the investment world, when people point to a commodity supercycle, they’re usually referring to the bullish, or the upswing part of the cycle.

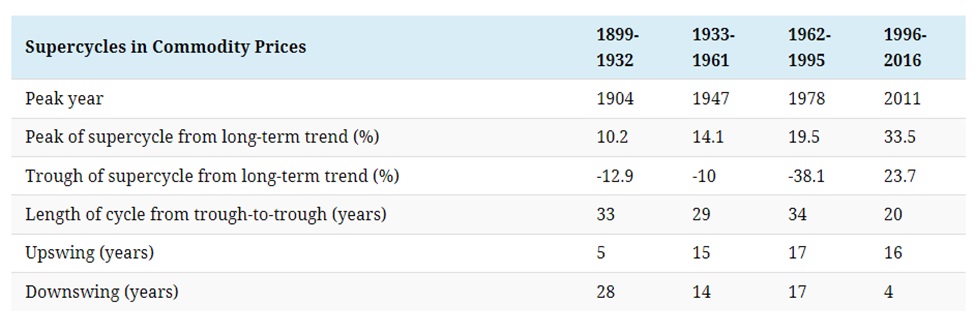

In the graphic provided by Visual Capitalist below, we can see that there have been multiple commodity supercycles throughout the course of history. Our most recent commodity supercycle started in 1996 and peaked in 2011, driven by raw material demand from rapid industrialization taking place in markets like Brazil, India, Russia and China.

The last cycle also ended with just four years of downswings, which meant prices would likely remain elevated relative to previous ones heading into the next one.

Data source: Bank of Canada, IHS. Image: Visual Capitalist

In fact, we may be right at the early stages of a new supercycle, as analysts have been predicting for years.

Dawn of a New Supercycle

A big proponent of the current “supercycle” talk other than AOTH is Goldman Sachs, which predicted back in October 2020 that commodities were beginning a supercycle that could last years, and possibly a decade.

Behind the bank’s supercycle call was the brutal decade for commodities in the aftermath of the 2008 financial crisis. By 2020, investors had all but abandoned the asset class in favor of equities.

“The lack of investment in commodities for tomorrow is startling,” Goldman said. “Without sufficient capex to create spare supply capacity, commodities will remain stuck in a state of long-run shortages, with higher and more volatile prices.”

In an interview with Bloomberg in January of 2022, Goldman’s global head of commodities research Jeff Currie stated that commodities are “the best place to be right now, particularly given the Fed pivot,” referring to the US Federal Reserve’s decision to begin hiking interest rates last year.

This year, the bank doubled down on its “commodity supercycle” take, citing growth in top consumer China and capital flight from energy markets and investment after concerns triggered by the US banking sector.

“As losses mounted, it spilled into commodities,” Currie told the Financial Times Commodities Global Summit in March 2023. “Historically, when you have this kind of scarring event, it takes months to get capital back,” he added.

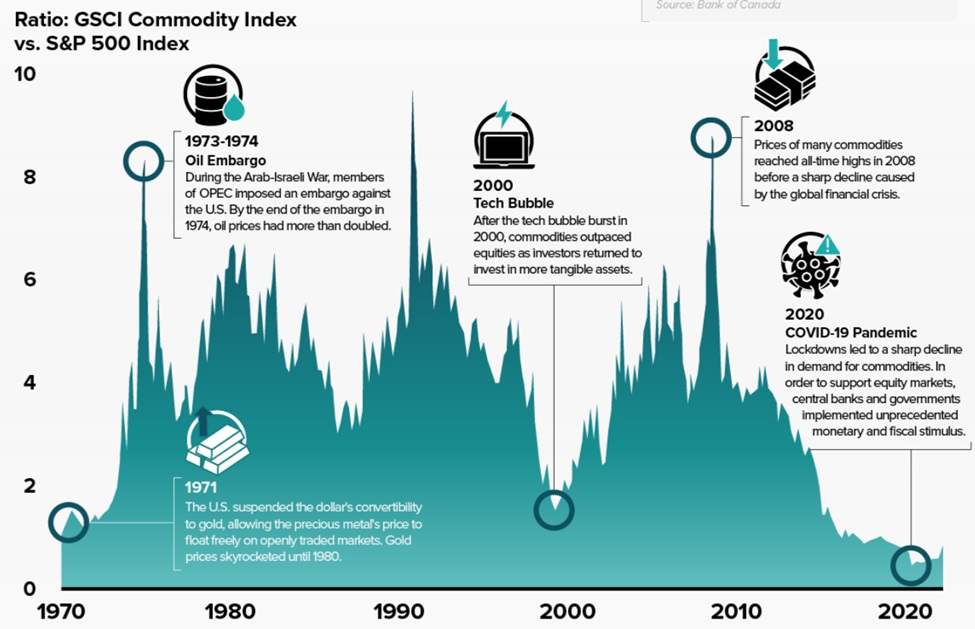

What’s interesting is that in past cycles, commodity prices and equity valuations have often been at odds with one another.

During the 1970s and early 1980s, for example, rising oil prices led to a significant decline in stock prices as higher energy costs hurt corporate profits. In contrast, during the first half of the 2000s, low oil prices were accompanied by a strong equity bull market that ended with the 2008 stock market crash.

The relationship, however, is not always straightforward and can be affected by various other factors, such as global economic growth, supply and demand, inflation and other market events.

Source: Visual Capitalist

As pointed out in Visual Capitalist’s infographic above, commodity prices have reached a 50-year low relative to overall equity markets over the Covid years. Perhaps the next supercycle is already up and running?

Historically, lows in the ratio of commodities to equities have corresponded with the beginning of new commodity supercycles.

This Time’s Different

While no two supercycles look the same, they all have three indicators in common: a surge in supply, a surge in demand and a surge in price.

The new commodity supercycle, however, could look a bit different from the previous ones for one simple reason — an increased focus on climate change.

According to S&P Global, a more aggressive commitment to the energy transition across G-20 nations could also create the conditions for a sustained surge in demand, supply and prices.

Like in the past, commodity supercycles are usually driven by strong demand for raw materials, manufactured materials and sources of energy. The energy transition serves as a major catalyst for all the key inputs to our renewable energy infrastructure, taking demand to levels never seen before.

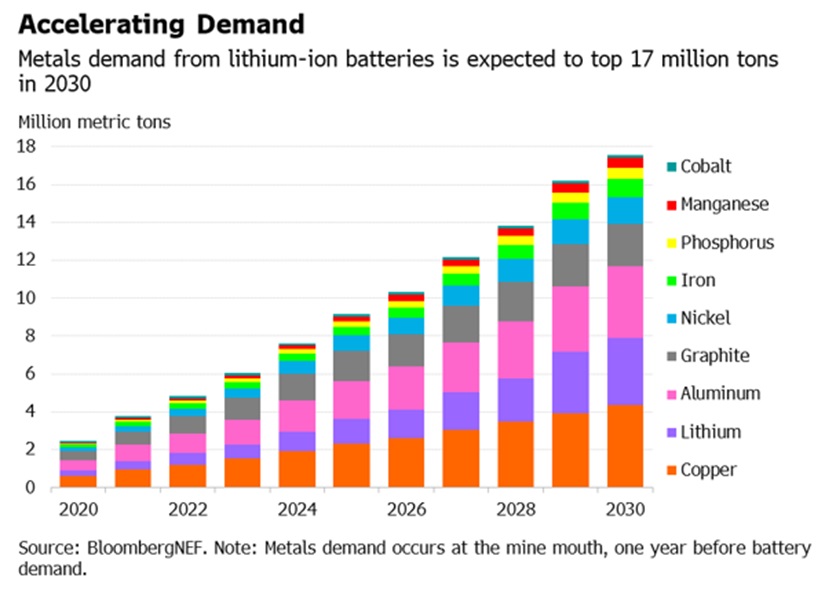

Demand for copper — the cornerstone for all electricity-related technologies — is set to grow by 53% to 39 million metric tons by 2040, according to BloombergNEF. Battery metals like lithium, cobalt and nickel will see even faster growth, reaching more than three times the current demand levels by 2030, says BNEF, with lithium rising the fastest with a seven-fold increase.

Source: BloombergNEF

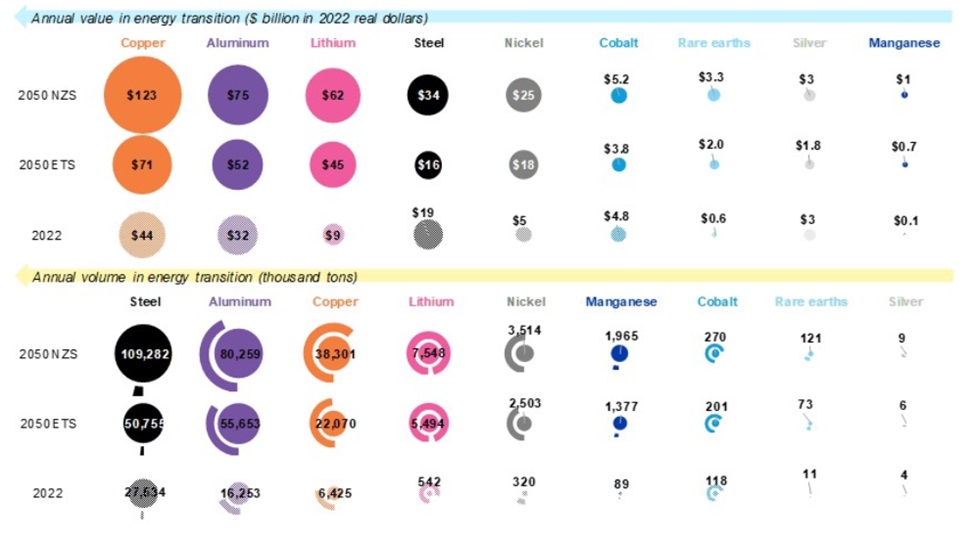

To reach net-zero, demand for these key metals needed for the deployment of energy transition technologies such as solar, wind, batteries and electric vehicles will grow fivefold by 2050, BNEF adds.

Source: BloombergNEF

The International Energy Agency forecasts mineral demand for use in EVs and battery storage will become a major force, growing at least thirty times by 2040. Lithium should see the fastest growth, with demand growing by over 40 times in its Sustainable Development Scenario by 2040, followed by graphite, cobalt and nickel (around 20-25 times).

Industrial metals like aluminum, which is essential to low-carbon technologies, are also expected to see healthy demand growth as the global economy recovers. Earlier this year, Goldman raised its price forecasts for aluminum, citing higher demand in China and the shaky political situation in Europe.

Rare earth elements, the key ingredients in permanent magnets used in electric vehicles and wind turbines, may see three to seven times higher demand in 2040 than today, according to the IEA.

According to the World Bank, graphite accounts for nearly 53.8% of the mineral demand in batteries, the most of any. Lithium, despite being a staple across all batteries, accounts for only 4% of demand.

An average plug-in EV has 70 kg of graphite, or 10 kg for a hybrid. Every 1 million EVs requires about 75,000 tonnes of natural graphite, equivalent to a 10% increase in flake graphite demand.

According to Benchmark Mineral Intelligence (BMI), the flake graphite feedstock required to supply the world’s lithium-ion anode market is projected to reach 1.25 million tonnes per annum by 2025. The amount of mined graphite for all uses in 2021, was just 1 million tonnes. (USGS)

Furthermore, the London-based price reporting agency forecasts demand for graphite from the battery anode segment could increase by seven times in the next decade as the growth in EV sales continues to drive construction of lithium-ion megafactories.

BloombergNEF expects demand for battery minerals to remain robust through 2030, with graphite demand increasing four-fold.

The International Energy Agency (IEA) goes 10 years further out, predicting that growth in demand for selected minerals from clean energy technologies by scenario, 2020 relative to 2040, will see: increases of lithium 13x to 42x, graphite 8x to 25x, cobalt 6x to 21x, nickel 7x to 19x, manganese 3x to 8x, rare earths 3x to 7x, and copper 2x to 3x.

Peaking Supply

As Goldman pointed out, the new commodity supercycle is quite unique in the sense that supplies for several commodities are set to peak or have already peaked, causing more market deficits and higher prices.

Previously, surging demand and falling supply are the hallmarks of a market in decline (i.e. coal). But now, it’s not so much about producers being reluctant to invest, but more of demand rising too fast for supply to catch up.

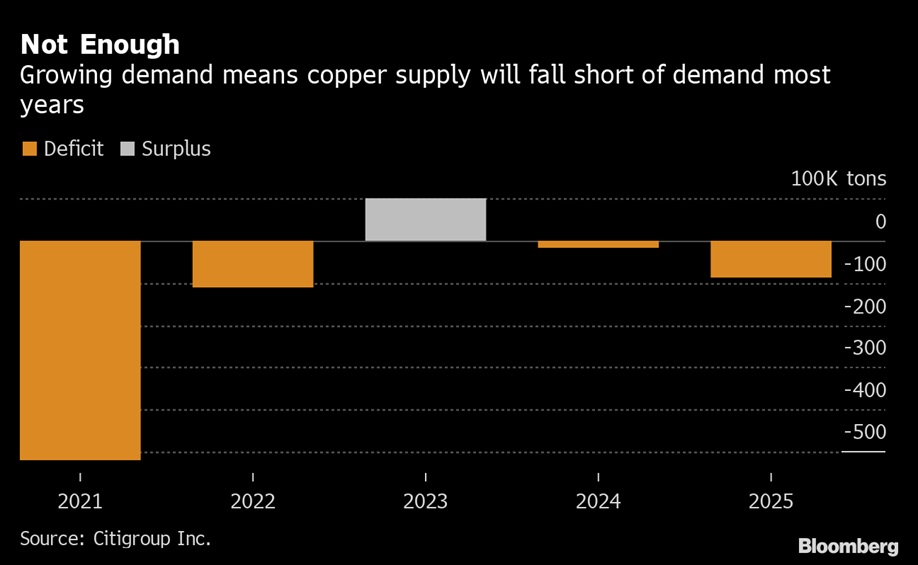

Take copper, for example, analysts at Goldman are extraordinarily bullish on the metal due to its high demand, predicting that “we’ll be at the lowest observable inventories that have ever been recorded at 125,000 tonnes” this year.

By year-end, the copper market is expected to be undersupplied, and some time in 2024, peak supply will arrive, generating deficits from that point, the bank said.

Back in 2021, Goldman’s Currie argued in a report titled “Copper is the new oil” that the global copper market is not prepared for the increased demand.

Source: Bloomberg

As the expansion of mines and creation of new copper production fields takes years, this is likely to lead to shortages of the metal. To prevent a depletion of copper supply within two years, prices must rise now to encourage investment and an expansion in output, Goldman said.

In its report, the bank estimated a long-term supply gap of 8.2 million tons by 2030, twice the size of the gap that triggered the bull market in copper in the early 2000s.

Economist and commodity market specialist Patricia Mohr told the audience at last year’s AME conference that copper could be “heading towards supercycle territory in the medium term,” referencing the newfound demand for copper as a critical metal.

One metal that has already plunged into deficit territory is silver, whose demand surged 18% last year. While often bought for investment purposes, silver is primarily used for industrial applications such as electronics and automotive. It’s also a key ingredient in solar panels, and as the world moves towards renewables, demand from that sector has grown exponentially.

The silver market has entered a “new paradigm” of ongoing deficits that’ll last for years, says Metals Focus consultants. In 2022, the market extended its shortfall from the previous year by nearly five-fold on the back of record-high demand from all major users.

Longer term, “there is not a great deal of movement (in silver supply), whereas on the demand side, we generally have that doing quite well … industrial demand in particular,” Philip Newman from Metals Focus told Reuters.

These examples demonstrate that insufficient capital spending from the last commodity cycle (i.e. from 2008 onwards) is now getting punished by the current demands of the clean energy era, leading us to years of market deficits. This is what makes a new supercycle potentially more exciting.

High Inflation

The final, and perhaps most definitive, indicator of a commodity supercycle is rising prices, and historically, supercycles tend to create inflation, which is what has occurred over recent years.

The head of real asset strategy at Wells Fargo recently told Kitco News that we’re already in the middle of a supercycle that kicked off in March 2020 and has at least six more years to go.

“Commodities are in a supercycle. We’re structurally undersupplied across the commodity complex,” John LaForge from Wells Fargo said. “The shortest supercycle on record is nine years. We are only in year three.”

“The commodity supercycle can be very destructive, and it’s probably going to force the hand of a lot of financial players,” LaForge said, while pointing that that world with inflation at 2% no longer exists, and “it will take time for governments and central banks to come to terms with that.”

And with that uncertainty, gold, acting as a safe trade for investors, should be able to perform as well as it has during previous cycles. The metal has been outperforming for nearly 3 years after hitting record highs in August 2020.

Based on historical analysis of commodity supercycles, Wells Fargo predicts that gold will at least double, and is looking at the $3,000/oz price target.

Conclusion

Here in the West, it isn’t only that we have failed to maintain mining and oil investments. We have also put roadblocks in the way of mining, such as the lengthy permitting process in North America. In Canada we’ve let interest groups hostile to corporations dictate resource policy.

We haven’t built the necessary infrastructure, either. We may have the metals but in Canada, the resources are quite often stranded, located far away from roads, railways and electricity. The Golden Triangle of northwestern BC and the Ring of Fire in Ontario are two examples. For many post-secondary school graduates, mining and oil and gas are part of the old-world economy. Unless more of an effort is made to entice them, retirements will continue to outpace new hires, leading to a severe skills shortage.

All of these factors are limits to growth.

In general there has just been a total lack of planning for what is to come; a failure to invest in, and support the natural resource sector.

In many metal markets, the West’s reluctance to mine has been China’s gain.

If there is a silver lining, it’s the fact that North Americans are finally starting to realize that to have security of supply, we need to develop our own mineral deposits.

The first step is recognizing that we have these metals, we do not need to purchase them from China, the DRC, Russia or any other foreign producer, we can mine and refine them right here.

Next is upping our exploration game — and nobody is better at it than Canadian junior resource companies — so that we can find and develop the deposits that will become the world’s next mines.

Richard (Rick) Mills

aheadoftheherd.com

*********

share

share

share

share

share