Is Dollarization a Mirage?

Argentine presidential candidate Javier Milei has made dollarization a central issue in the election. In response, 170 experts have signed an open letter claiming dollarization is not a real solution, but un espejismo—a mirage. These experts say dollarization will not remedy Argentina’s fiscal imbalances nor numerous other issues.

Critics who follow this line of argument make two fundamental errors. First, they argue against a strawman version of the dollarization plan. Second, they overlook some of its benefits. Economics is about weighing cost-benefit trade-offs, not just costs.

The Strawman

No serious economist claims that dollarization, on its own, will resolve all of Argentina’s macroeconomic problems. It is not a sufficient reform. Nonetheless, advocates of dollarization believe it is a necessary reform. Given Argentina’s history and institutional weaknesses, policymakers are unable—or, at the very least, unlikely— to implement other essential reforms unless they face the constraints imposed by dollarization. In other words, dollarization is a complementary reform, not a substitute for much-needed structural changes. Moreover, since other monetary reforms lack the credibility required to be sustainable, they would jeopardize the success of the much-needed structural changes.

Over the last decade, the Argentine economy has stagnated. The latest inflation rate exceeded 10 percent per month. Dollarization offers a swift and credible solution to the inflation problem. And the inflation problem must be solved swiftly and credibly so that the government can address other issues. Resolving fiscal imbalances and other structural problems will take time. Without a quick victory on the inflation front, the new government will become a lame duck, unable to make progress on the other issues.

The Overlooked Benefits

While dollarization isn’t a panacea, it does offer advantages to a country that has an unstable currency and a tendency to elect populist leaders. Dollarization didn’t prevent Ecuador from electing Rafael Correa (2007 – 2017). It didn’t prevent Correa from pursuing populist policies. It didn’t prevent those policies from causing economic stagnation. But it did limit the damage: Ecuador’s inflation rate has remained at levels comparable to that of the United States. Domingo Cavallo, who served as the Minister of Economy in Argentina from February 1991 to August 1996 and again from March 2001 to December 2001, says there is “no doubt” that dollarization saved Ecuador from becoming Venezuela.

Argentina needs saving, as well. The populist policies imposed during the Kirchner administration (2003 – 2015) have caused the Argentine economy to stagnate. But, unlike in Ecuador, the Argentine central bank has been permitted to accommodate those policies. As a consequence, Argentina has suffered from stagnation and high inflation. Indeed, Argentina has one of the highest inflation rates in the world today.

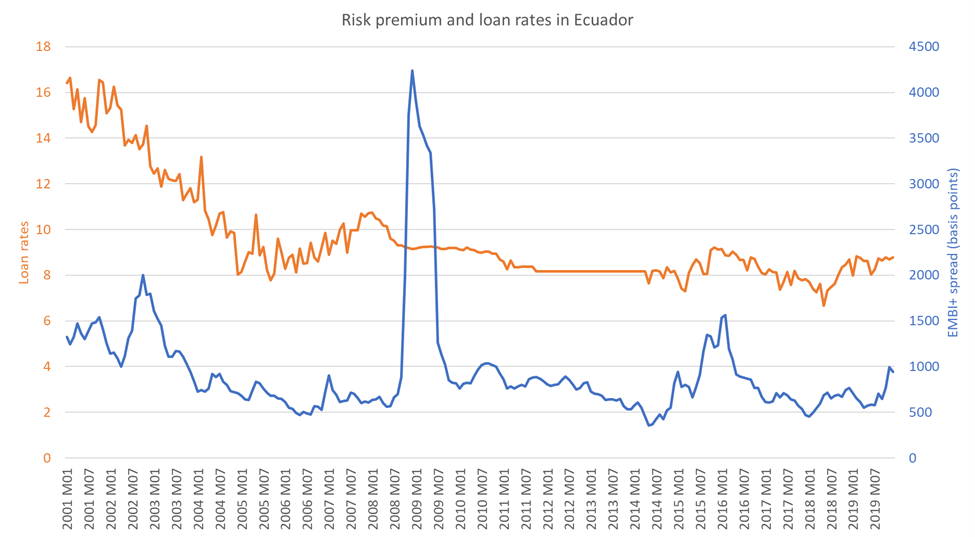

The difference in inflation is significant, but that’s not the only benefit. Dollarization also helps insulate private credit markets from sovereign default. Ecuador defaulted on its sovereign debt in 2008. Unsurprisingly, its country-risk premium increased considerably. In other countries, fears of debt monetization might have caused private sector credit to contract as well. But not in Ecuador. Since Ecuador was dollarized, private sector credit remained largely unaffected by the default. As the following figure shows, the spike in the country-risk premium (blue line) did not push up loan rates in Ecuador.

Argentina has not fared so well. Sovereign default crises in Argentina similarly raise the country-risk premium. However, since such crises might trigger another round of debt monetization, it also causes private credit to contract. Dollarization would serve as a firewall, protecting the private sector from the fiscal policy fallout.

Conclusion

Critics who defeat strawman dollarization proposals do a disservice to Argentine voters. Dollarization is neither magic nor a mirage. It will not solve all of Argentina’s problems. But it will solve the inflation problem. Furthermore, it will create better incentives for fiscal and structural reforms—and limit the damage from poor policies should the incentives not be strong enough.

Courtesy of AIER.org under https://creativecommons.org/licenses/by/4.0/ Article originally published here.

*********