If The Markets Turn Quickly, How Bad Can Things Get?

share

share

share

share

share

share

share

share

share

share

HOW BAD CAN THINGS GET?

Pretty damn bad. Which means that it will likely be much worse than most of us can imagine. Other than Covid and its forced shutdown of economic activity by governments world-wide, the most recent learning experience for investors is the Great Recession of 2007-09. Beginning in October 2007 and ending in February 2009, the S&P 500 Index lost 53%…

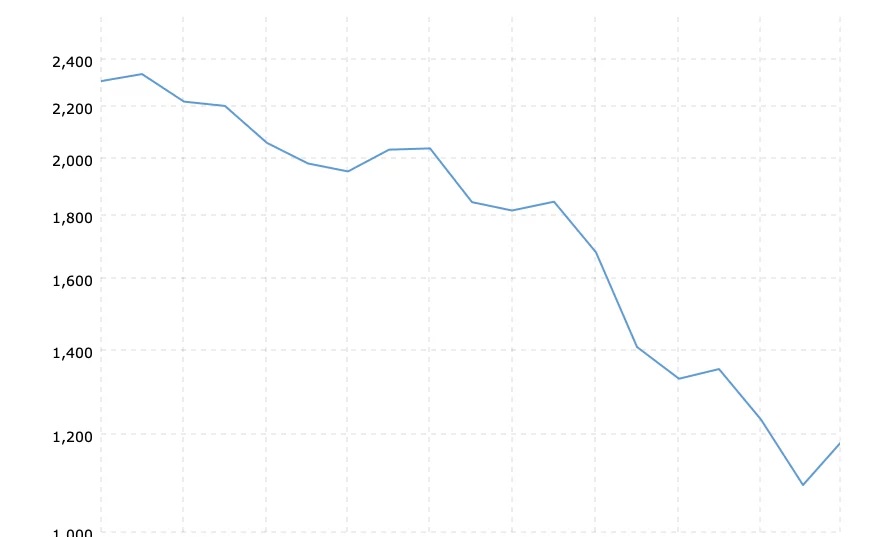

S&P 500 Index 2007-09

Most of that loss (38%) occurred during calendar year 2008. It was the largest single, calendar-year decline since a similar -38% in 1937. Both the NASDAQ (-53%) and DJIA (-50%) declined by similar amounts.

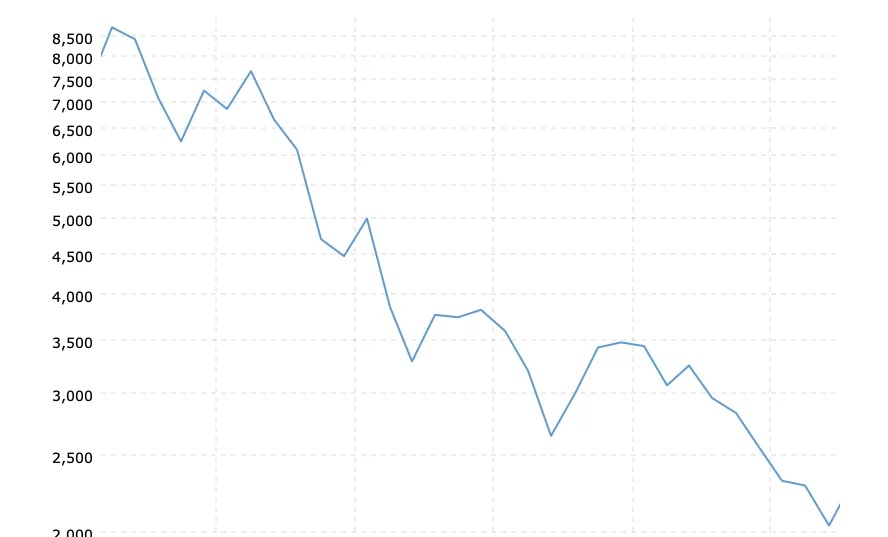

Prior to the Great Recession, post-Y2K markets collapsed in a heap on the heels of the most profitable decade in U.S. financial and economic history. For more than 2 1/2 years, between February 2000 and September 2002, stocks were in a tailspin led by the NASDAQ which declined by 80%. The carnage is pictured on the chart below…

NASDAQ Composite 2000-02

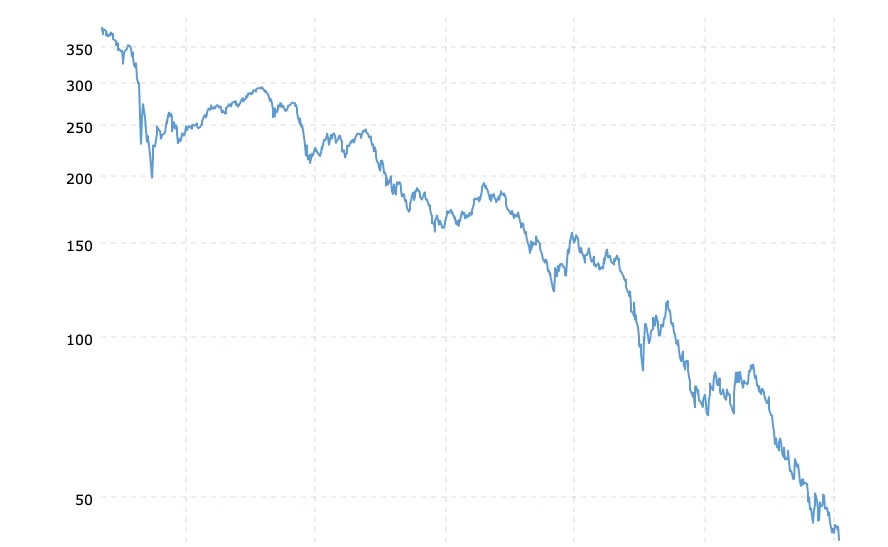

The extent and breadth of the declines and accompanying bankruptcies of hundreds of dot.com companies is rivaled only by the Stock Market Crash of 1929 which is shown on the chart (source) below…

Dow Jones – 1929 Crash and Bear Market

Over an excruciating three years (September 1929 – July 1932), stocks declined by 90%. Stocks did not recover their original pre-crash levels until 1954, twenty-five years after the September 1929 peak. The accompanying economic depression lasted until 1941, although a significant portion of what is termed a resumption of economic activity, was accounted for by war-related industrial activity. Economic conditions on the homefront were characterized by rationing, price controls, and shortages.

WHAT MIGHT CAUSE A MARKET CRASH?

Stock market crashes like those described above don’t happen spontaneously. There are a number of factors which lead to eventual corrections of significance. They include the evolution of normal business and economic cycles, duration and extent of previous stages of those cycles, intervention and manipulation by governments and central banks, the need for corrections and rebalancing due to poor judgement and market excesses, and political and economic factors.

U.S. economic activity has been declining broadly for more than a year or two. That is partially attributable to changes in interest rates which have caused a reassessment of cost factors and undermined the credibility of various investment strategies. The manipulative expansion of cheap and easy credit over the previous four decades resulted in excesses that weren’t fundamentally justified and which distorted the financial landscape. Highly disproportionate availability of cheap credit led to serious misallocation of resources and capital.

In addition, the use of leverage has exacerbated the problem. The unfathomable and unexplainable derivatives monster has the potential to wreak incalculable damage on the financial markets. The use of leverage throughout all markets – stocks, bonds, commodities – and including the use of options, futures, and other more precarious derivatives, currently rivals its pre-1929 use which approached 90%.

The currently added recent market excesses are based on expectations for a return to cheap credit. It is assumed that once the Fed announces a rate cut, that a return to the good old days is right around the corner. As much as a 50 basis point cut is already factored in to current stock and bond prices. What happens when that cut is announced? (see What Happens After A Rate Cut Is Announced?)

MORE ABOUT THE FED

The Fed will likely NOT pursue a series of significant rate cuts UNLESS there is an acceleration of the current decline in economic activity. It makes no sense to simply return to the hell that was brought about by its own intentions and actions previously, and which forced them to try to navigate a return to a more normal and reasonable, higher level for interest rates. On the other hand…

Since the Fed is occupied mostly with slaying dragons which it birthed by its own errant monetary policy, including more than a century of intentional inflation, they are doomed to a life of putting out fires and containing collateral damage. For investors, it is time to wake up to the fact that the Fed is not your financial savior and its purpose and goals, irrespective of any so-called mandates, are not aligned with yours.

CONCLUSION

It is possible that a deepening recession (official or not) could morph into something worse – an economic depression. Even if the Fed cuts rates aggressively, it might not be enough t0 stop the cascading waterfall of lower prices for all assets priced in dollars; including stocks, bonds, commodities, real estate, etc. A collapse in the credit markets such as that which occurred in 2007-08 would likely overwhelm any efforts by the Fed to stop the hemorrhaging.

It would not be unreasonable to see prices decline by 50% or more initially. Further declines would be likely as it is unlikely that an event of this nature at this particular time could be reversed in timely fashion. The prevailing conditions of unemployment and shuttered doors spawned by wholesale financial destruction would be too much for a beleaguered Fed.

It may or may not happen, but investors who ignore the possibility could be in for a shock. I do not consider the likelihood of such an event, or the reaction of the Fed or the government, to be altered in any significant way regardless of November election results. (also see: Default – Deflation – Depression)

Kelsey Williams is the author of two books: INFLATION, WHAT IT IS, WHAT IT ISN’T, AND WHO’S RESPONSIBLE FOR IT and ALL HAIL THE FED

*********

share

share

share

share

share

More from Gold-Eagle