Gold SWOT: Gold Climbed to the Highest Since May as the Dollar Weakened

Strengths

- The best performing precious metal for the week was silver, up 4.81%. Aris Mining is increasing capacity of the Maria Dama processing plant within the Segovia Operations from 2,000 to 3,000 tons per day (tpd). The costs for the plant expansion are estimated at $11.0 million and completion is expected by early 2025. Aris Mining also reported a significant update to its reserves.

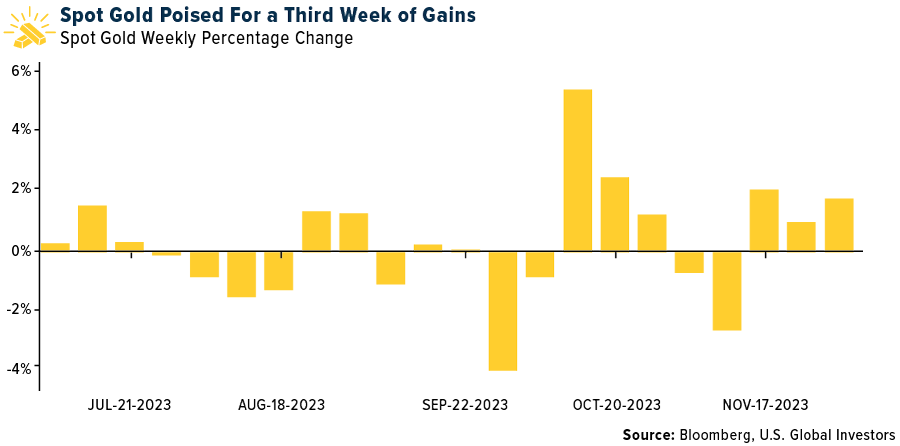

- Gold climbed to the highest since May as the dollar weakened ahead of Treasury auctions that are expected to indicate whether the U.S. bond market is set for a meaningful revival. Bond yields extended declines on Monday after weaker-than-expected U.S. new-home sales data, while gold held gains. Lower interest rates are typically good for non-yielding assets like precious metals.

- According to BMO, Dundee Precious Metals (DPM) reported an updated reserves and resources statement for its flagship Chelopech operation in Bulgaria, which resulted in mine life extension by another year to 2032. Furthermore, the reserve and resource update indicate a slight increase in gold and copper grades by 5% and 3%, respectively. The mine plan also includes gold recovery increase of 5%.

Weaknesses

- The worst performing precious metal for the week was palladium, down 6.60% on oversupply, and substitution from platinum, which has been cheaper to acquire. Palladium is down 40% this year while platinum had dropped about 13%. According to Bank of America, in its latest monthly, the World Gold Council (WGC) noted physically backed gold ETFs saw continued outflows in October. This trend was most pronounced in North America, where selling totaled $2 billion (28 tons). In Europe, selling totaled $622 million (11 tons). It seems the rise in interest rates has shifted investor preferences away from the yellow metal to higher yielding assets in the western nations while Asia and India have picked up their purchases of gold. Global ETF outflows have totaled 225 tons year-to-date, making 2023 the second largest year for ETF outflows.

- According to Canaccord, Westgold Resources lowered its FY25-31 production forecast at Murchison by 5% on average to account for the tie in of the long-hole open stoping (LHOS) operation with Big Bell's existing cave. The combined operations account for 45% of production at Murchison hub over this period.

- Following a winder rope incident at the start of last week, Impala Platinum announced 12 fatalities at Rustenburg's 11 Shaft. A further 74 employees were injured in the accident and 10 remain in critical condition. The accident is under investigation as regulations are clear concerning the regular safety checks and inspections.

Opportunities

- Goldman Sachs sees an environment developing for gold with a fattening in right-tail price risk into next year. The potential upside in gold prices will be closely tied to U.S. real rates and dollar moves, but they also expect persistent strong consumer demand from China and India alongside central bank buying to offset downward pressures from upside growth surprises and rate cut repricing. On net, they would expect any selloffs to be limited in scale due to a dovish Federal Reserve, slowing wage growth, and resilient central bank purchases and tactically would view a sell-off in gold as a buying opportunity. They maintain their 12-month gold target at $2,050/oz.

- Moneta Gold and Nighthawk Gold have announced an at-the-money merger whereby Moneta will acquire all the Nighthawk issued and outstanding shares. Each share of Nighthawk will receive 0.42 shares of Moneta in exchange and the overall ownership post the transaction is expected to 34% Nighthawk and 66% Moneta.

- According to Canaccord, gold is up 12% this year yet the S&P/TSX Global Gold Index is up only 4% and the VanEck Vectors Gold Miners ETF 9%. They also note that roughly 50% of their coverage universe is down 20% or more from their 52-week highs. The last four times the gap between gold and gold equities have been this wide (dating back eight years) has resulted in an average 25% subsequent rise in the gold price and 100% average increase in the S&P/TSX Gold Index.

Threats

- According to Bank of America, as the U.S. yield curve flattens, the gold price tends to rise; and as the U.S. yield curve steepens, the gold price tends to fall (or rise more slowly). The U.S. rates team is calling for the yield curve (i.e., 2s10s) to dis-invert in H2'24, reaching a positive slope by the end of 2024 (vs. sharply negatively sloped currently). They wonder if this might act as a damper on the gold price even if the Fed is cutting its rate.

- According to Bank of America, demand for palladium and the wider platinum group metals complex is under pressure as the world transitions from internal combustion engines (ICEs) to electric vehicles (EVs). They model a palladium surplus of 1.4 Moz in 2024. To balance the market, cuts will likely be required. Which mines are most "at risk"? In their view, the palladium rich mines of North America, Sibanye Stillwater (Sibanye, SSW) and Impala Canada (Impala, IMP). They also see potential to rationalize higher cost mines in South Africa; they believe that Impala will take further write-downs on Royal Bafokeng Platinum (RBP) carrying value.

- Bloomberg expects platinum to remain in deficit throughout the rest of this decade, while palladium and rhodium will shift to surplus and stay that way for the foreseeable future. As the EV transition continues, the 90% of demand for palladium and rhodium that comes from ICEs will weaken demand for both metals.

********

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com. You can contact Frank at: [email protected].

Frank Holmes is the CEO and Chief Investment Officer of U.S. Global Investors. Mr. Holmes purchased a controlling interest in U.S. Global Investors in 1989 and became the firm’s chief investment officer in 1999. Under his guidance, the company’s funds have received numerous awards and honors including more than two dozen Lipper Fund Awards and certificates. In 2006, Mr. Holmes was selected mining fund manager of the year by the Mining Journal. He is also the co-author of “The Goldwatcher: Demystifying Gold Investing.” Mr. Holmes is engaged in a number of international philanthropies. He is a member of the President’s Circle and on the investment committee of the International Crisis Group, which works to resolve conflict around the world. He is also an advisor to the William J. Clinton Foundation on sustainable development in countries with resource-based economies. Mr. Holmes is a native of Toronto and is a graduate of the University of Western Ontario with a bachelor’s degree in economics. He is a former president and chairman of the Toronto Society of the Investment Dealers Association. Mr. Holmes is a much-sought-after keynote speaker at national and international investment conferences. He is also a regular commentator on the financial television networks CNBC, Bloomberg and Fox Business, and has been profiled by Fortune, Barron’s, The Financial Times and other publications. Visit the U.S. Global Investors website at http://www.usfunds.com. You can contact Frank at: [email protected].